How Bangladesh and Pakistan Can Survive the Energy Crisis

13 August 2024 – by Viktor Tachev

Rising energy demand, strong fossil fuel import dependence and fiscal challenges due to price volatility – the energy crisis in Bangladesh and Pakistan reminds us of the striking similarities in both countries’ circumstances. The two nations are very much alike also in their weak clean energy targets and limited solar and wind deployment. Instead of following regional leaders’ pathways to energy security and affordable electricity, Pakistan and Bangladesh are increasingly looking to deepen their fossil fuel dependence, locking themselves into a future of high power costs, unstable supply and economic and climate hardships.

The Fossil Fuel Import Dependence of Bangladesh and Pakistan

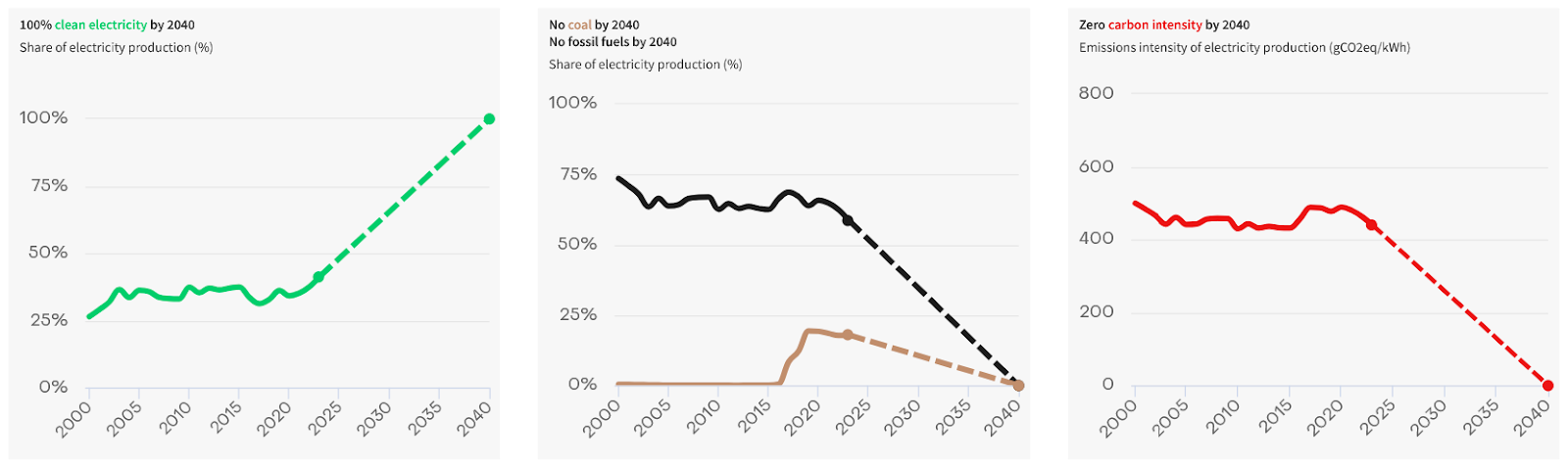

In 2023, the share of fossil fuels in Pakistan’s electricity generation mix was 59%. Solar and wind comprised just 2.7%, while low-carbon electricity sources’ share stood at 24%. Although the country has the ambitious target of having renewables account for 60% of its electricity generation mix by 2030, it will continue to rely significantly on fossil fuels.

As of 2023, coal met 18% of the electricity demand, up from just 1% in 2016. The government plans to quadruple its coal-fired capacity by 2030 and is considering retrofitting furnace oil-based power plants to accommodate for coal.

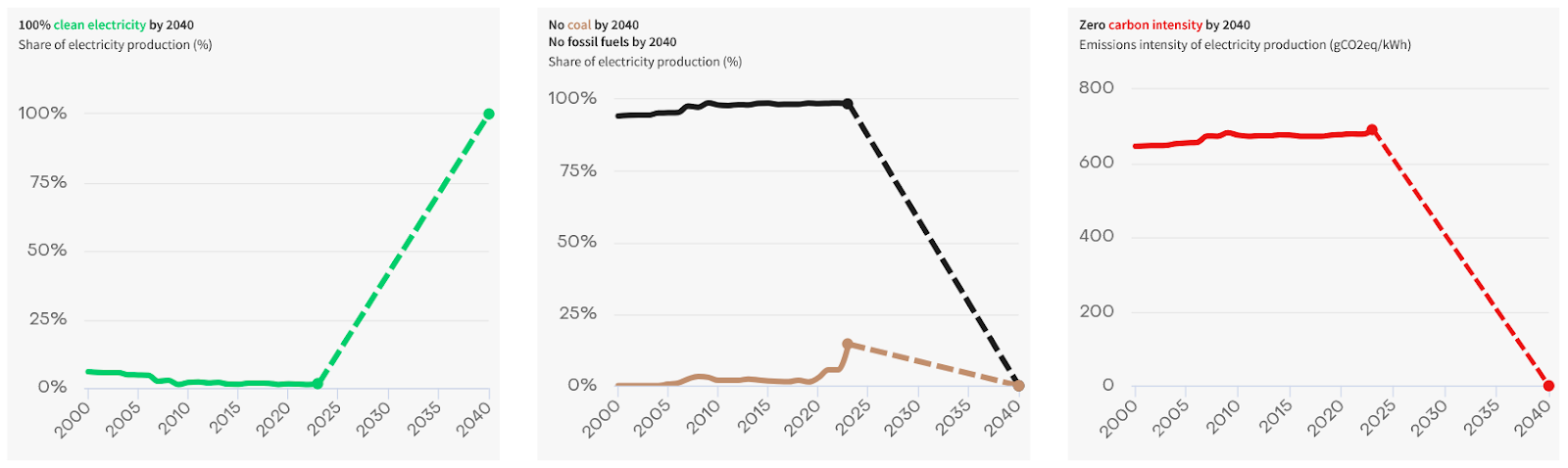

Bangladesh is among the top 10 economies most dependent on fossil fuels for power generation. Ember notes that the country relies on fossil fuels, mainly natural gas, for 98% of its electricity generation. The share of renewables is just 1%. While the IEA calls for a clean power target of 60% by 2030, the goal of Bangladesh is just 16%.

According to estimates, the domestic natural gas resources that have long fuelled the country’s power sector are now depleting. The expectations are that they will run out in the next nine to 11 years.

Both countries rely on imported coal and gas to meet a sufficient share of their energy demand.

The Result of Fossil Fuel Import Dependence: A Severe Energy Crisis in Bangladesh and Pakistan and Economic Hardship

The increased volatility of coal and gas prices on global markets has made Bangladesh and Pakistan unable to afford deliveries. As a result, they have suffered prolonged power cuts. In Bangladesh, they affected up to 80% of the country and are likely to last until at least 2026. Pakistan also felt firsthand the consequences of being at the mercy of suppliers when, in the midst of the energy crisis, its gas deliveries were cancelled and rerouted to wealthier buyers, leaving the country in the cold.

To tame the energy crisis and the high electricity prices, Bangladesh has tripled its coal-fired power output in 2023. While the government’s strategy salvaged the situation in the short term, Reuters reports that it was at the expense of cleaner fuels. Furthermore, the move was motivated by the struggle to pay for costly natural gas, furnace oil and diesel imports due to shrinking dollar reserves and a weakening currency. Government officials confirmed that the country will follow a similar strategy this year.

Without more sustainable long-term power system master plans that diversify the energy mixes by prioritising accelerated clean energy deployment, both countries risk taking up a strategy that has already backfired in the past.

Macroeconomic Woes

When the 2022 energy crisis struck Bangladesh, the country had to pay above-market prices to avoid suffering extended blackouts. For example, some gas delivery deals were struck at prices 10 times higher than in the previous years, while imported LNG cost 24 times more than domestic gas supplies. Paired with the depreciation of the local currency against the US dollar, the country had to drain its foreign currency reserves to ensure deliveries. The situation became so severe that Bangladesh had to turn to the IMF and creditors for financial assistance. Even despite paying over the odds, the country still had to endure prolonged blackouts. Today, Bangladesh’s annual fossil fuel import bill still remains high, sitting at USD 2 billion.

Aside from the immediate pricing risk, the import-oriented plans of both countries bear long-term risks in the form of stranded assets. According to the IEEFA, Pakistan faces a real risk of unutilised LNG terminal capacity and idle supply infrastructure due to a supply-demand mismatch. The agency doesn’t see gas becoming more affordable in Pakistan in the future, even if LNG prices come down or the country pushes through its virtual LNG projects for transporting gas off-grid by trucks or rail and bringing costs down. According to the analysts, Pakistan will continue paying higher prices due to oil-indexed contracts and high credit risk, while investments in additional supply risk locking consumers in unaffordable power.

The case is similar when it comes to coal. IEEFA researchers warn that Pakistan’s policymakers’ actions to revive coal power plants and import coal lack evidence-based research, considering that due to the foreign exchange crisis, the country is unable to procure supplies and is shutting down imported coal-based power plants.

Economic Hardship For Businesses and Households

The volatile prices of natural gas in global markets have also taken a toll at the microeconomic level. In the case of Bangladesh, one of the leading global textile and garments markets, the unpredictable power prices and supplies have affected the export-oriented industry’s competitiveness by increasing production costs and reducing output. After Bangladesh’s government again increased power tariffs for all consumer categories in 2024 due to high power generation costs, both industries and households started considering energy efficiency investments to ease the strain on their finances.

In 2023, Pakistanis took to the streets to express their disagreement with the electricity hikes. In some parts of the country, the protests turned violent. Human Rights Watch urged the IMF to intervene and help the struggling country deal with the situation.

Scaling Up Renewables Can Unlock Economic Gains

Bangladesh government officials admit that renewables won’t make up more than 5% of overall output by 2030, with fossil fuels dominating power generation in the coming years.

Such a decision means a failure to capitalise on the country’s massive untapped solar and wind energy potential of 341 GW. Even utilising just 4% of the territory would ensure enough capacity for a 100% renewable energy-powered system. On top of that, the country has vast hydropower potential, with over 50% of its capacity untapped.

Pakistan’s untapped clean energy potential is nearly 60 GW for hydropower, 40 GW for solar, and 346 GW for wind.

However, it is worth noting that capitilising on the vast clean energy potential in both countries won’t be a seamless journey. For example, governments can expect potential hurdles in raising the needed capital for the energy transition. Overcoming them would require exploring various financing options, such as multilateral development banks (MDBs), green bonds, private equity funds, investment promotion and financing facilities. It is worth noting also that aside from increasing their clean energy capacities, both countries should also concentrate on sufficient investments in battery storage, grid buildup and modernisation to overcome issues like transmission constraints and energy losses.

Furthermore, both countries need to address bureaucratic barriers to increase transparency and guarantee investment security for clean energy project developers. This is especially important for Pakistan, where the IEEFA notes that decision-making mostly happens in the highest echelons of power and without any public disclosure of the reasoning.

Still, addressing those barriers is crucial, since the reluctance to expand clean energy capacity can prove a costly move.

Shelter From Fossil Fuel Price Volatility Through the More Affordable Clean Power

In economic terms, as per Bangladesh’s Integrated Energy and Power Master Plan 2023, fulfilling the 37.8 GW renewable energy without energy storage systems laid in the framework will cost USD 37.4 billion. While this might seem a significant amount for a distressed economy, it pales in comparison to the fact that climate change adaptation is costing the economy 6-7% of its annual budget each year due to the reliance on fossil fuels, which increases costs and drives up inflation, and the health costs of having the worst air quality in the world. According to TransitionZero, when accounting for air, water and climate costs, the average operating cost of coal is 27% higher than that of clean energy.

At the same time, analysts reveal that Bangladesh could immediately deploy around 12.5 GW of solar power on rooftops and other available areas. Furthermore, installing just 2 GW of solar and replacing diesel-run irrigation systems with solar-powered ones will save around USD 1.1 billion from fuel import costs.

Pakistan can also unlock significant economic gains from scaling up renewables at the expense of fossil fuels. During the peak of the energy crisis in 2022, Pakistan’s coal import reliance resulted in delivery costs as high as USD 419 per tonne. This resulted in power generation costs of up to 19.3 US cents per KWh. For reference, the IEEFA notes that hybrid renewable energy systems consisting of solar, wind, and battery energy storage have a cost of power generation ranging between 5.3-7.7 US cents per KWh.

Reduced Burden of Fossil Fuel Subsidies

Aside from bringing electricity prices down, reduced fossil fuel reliance can also ease the burden of fossil fuel subsidies on the state budget. In the case of Bangladesh, for example, studies suggest that removing fossil fuel subsidies will increase the country’s GDP by up to 2.3%. It will also improve the welfare of Bangladeshis by 1.89%. However, such a move should be accompanied by comprehensive reforms that will protect households from price increases and facilitate the transition to sustainable energy through universal social protection systems.

Tame the Impact of Climate Change

Moving away from fossil fuels will mean that Bangladesh and Pakistan are actively contributing to solving a problem that they are highly vulnerable to. Between 2000 and 2019, they have been the seventh (Bangladesh) and eighth (Pakistan) most affected countries globally by climate disasters. Floods, droughts and heatwaves have been taking a massive toll on both nations’ ecosystems, livelihoods, infrastructure and food and water security.

According to the World Bank, in Bangladesh, the average tropical cyclone costs Bangladesh about USD 1 billion annually. By 2100, a third of the population could be at risk of displacement.

In Pakistan, climate change could potentially cost the country up to USD 3.8 billion in annual losses.

From a climate resilience and preparedness perspective, scaling up renewables will also contribute to implementing comprehensive national security strategies.

Moving From Quick-Fixes to Long-Term Solutions Critical

Although there are some differences, the situations in the energy sectors and the poor financial health of both Pakistan and Bangladesh that we see today are mostly a byproduct of prioritising quick-fix strategies centred around imports instead of long-term, sustainable plans. For example, due to its strategy, Pakistan is still paying high power costs today and continues to suffer energy cuts, but on top of them, it also has an energy deficit of 6 GW and an import bill of USD 7 billion.

These circumstances are a reminder that instead of making the same decisions and expecting a different result, both countries should chart new pathways with a focus on scaling up renewables instead of fossil fuels to minimise the economic, environmental and health costs.

by Viktor Tachev

Viktor has years of experience in financial markets and energy finance, working as a marketing consultant and content creator for leading institutions, NGOs, and tech startups. He is a regular contributor to knowledge hubs and magazines, tackling the latest trends in sustainability and green energy.

Read moreOur Publications