ASEAN Countries Need to Prioritise Renewable Energy Not Ammonia, Hydrogen and CCS

27 September 2023 – by Viktor Tachev

At COP26, Japan promised to “lead the way in the clean energy transition, with a particular focus on Asia” and “undertake efforts toward net-zero emissions in Asia”. Fast-forward two years, and instead of helping accelerate decarbonisation efforts and provide renewable energy financing, Japan is trying to burden ASEAN and African nations with questionable technologies under its GX strategy.

“Expensive and very dirty” is how BloombergNEF refers to Japan’s plans, while environmentalists labelled them as “toxic” and a “greenwashing exercise”.

In that sense, it would be surprising if ASEAN countries partnered with Japan – known as the world’s largest public fossil fuel finance provider – on decarbonisation projects. However, recent history proves energy policy decisions don’t always follow common sense.

Japan’s Plans For Exporting Its GX Technology to ASEAN Countries

Japan’s Green Transformation Strategy (GX) is an investment roadmap for mobilising USD 1.1 trillion in public and private financing over the next decade. It aims to transform the industry and speed up decarbonisation progress domestically and regionally.

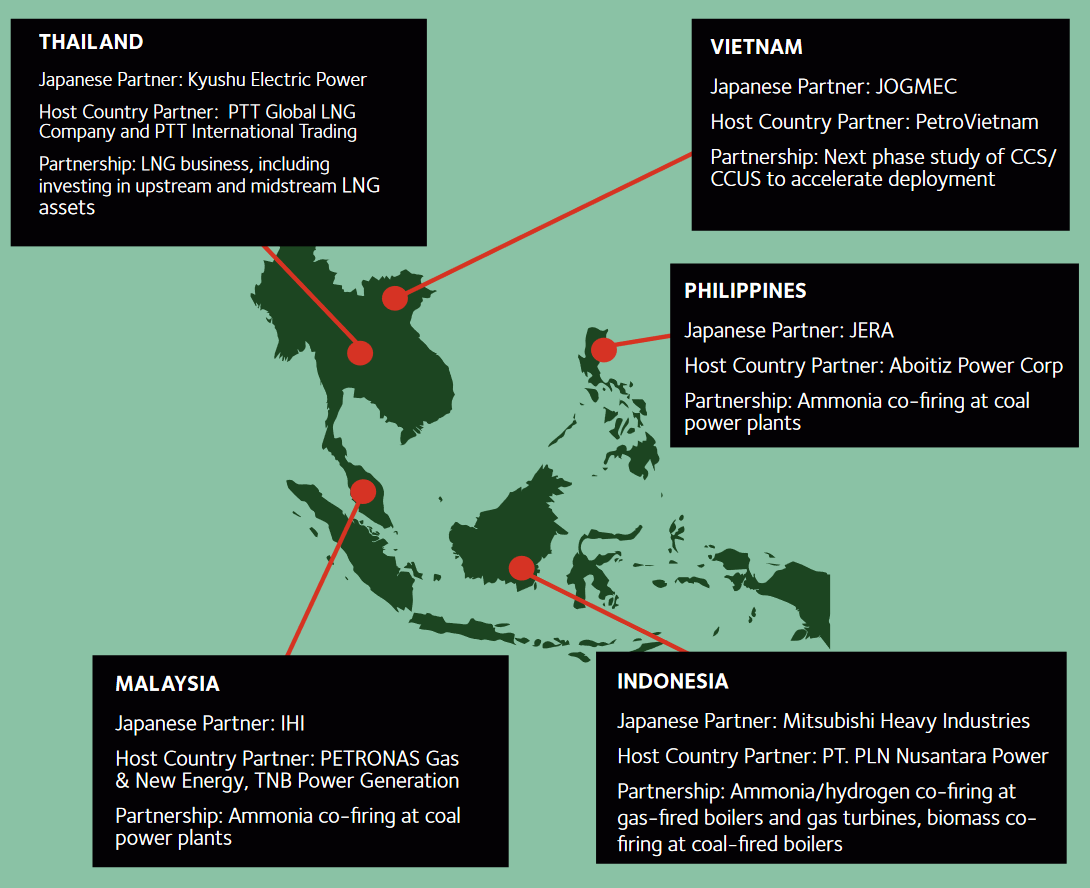

While the strategy’s name might suggest that it will spearhead the clean energy transition, it seems it will impede it. The proposed technologies include LNG, ammonia co-firing at coal-fired power plants, hydrogen and carbon capture and storage (CCS). Japan’s basic energy plan aims to export these solutions to developing countries in Southeast Asia.

Makiko Arima from Oil Change International states that the GX strategy risks delaying Asia’s energy transition.

“The Green Transformation policy is just a euphemism for technologies that prolong the use of fossil fuels, and Japan is pushing hard to promote it in South and Southeast Asia,” the expert warns.

The Risks For ASEAN Countries

In 2022, most of the ASEAN governments suffered some of the worst consequences of the energy crisis. Having to deal with high power costs and the inability to ensure a stable power supply forced them to search for a long-term solution.

Japan has always been perceived as Asia’s technology and innovation leader. As a reliable and friendly partner to ASEAN governments, it again emerged with potential solutions to the region’s problems.

However, market experts warn that strong interests from the Japanese fossil fuel lobby drive the GX strategy. Analysts argue that Japan is pushing other countries to adopt the strategy because its energy businesses are searching for new export markets.

According to Kimiko Hirata, the founder of Kiko Network and Climate Integrate, the country has a strong interest in prolonging the life of fossil fuels, as many private Japanese companies have actively participated in such projects and don’t want to lose their investment.

At the same time, Hirata warns that Japan hasn’t even explained the specifics of the GX to other countries in detail, which is why they might struggle to recognise the false solutions within.

Failure to do so will expose ASEAN economies to various risks.

Locked in a Future of High Emissions

According to TransitionZero, Japan is misleading countries across Southeast Asia regarding its technologies’ carbon emissions-saving potential. Instead of helping ASEAN governments accelerate their decarbonisation efforts, they will prolong the life of fossil fuels and result in substantial emissions.

For example, TransitionZero finds that Japan’s goal of 20% ammonia co-firing at domestic coal power plants by 2030 would still generate nearly double the emissions compared to standard gas-fired power plants. Even 50% ammonia co-firing schemes would emit comparable emissions to gas power generation.

While these scenarios are theoretical, the practice shows that blue ammonia project sites can emit more emissions than projected.

BloombergNEF concludes that even green ammonia-based scenarios can’t align with a net-zero-aligned power sector.

The case is similar when it comes to blue hydrogen. The emissions of such plants can exceed those of conventional gas-fired power generation.

“What is inside of this strategy seems rather unaligned with both the 1.5°C target and the actual transformation needed, providing only unsustainable solutions against global trends,” notes Hirotaka Koike, senior political and external affairs officer at Greenpeace Japan.

Yet, Japan already has memorandums of understanding with various countries across Asia for cooperating on projects involving the GX technologies. As a result, their JETPs are now at risk of being undermined.

An Unnecessary and Expensive Technology

Ammonia and hydrogen as power sources remain largely untested solutions with no practical application and commercialisation. According to estimates, these technologies might not be ready for application by 2035.

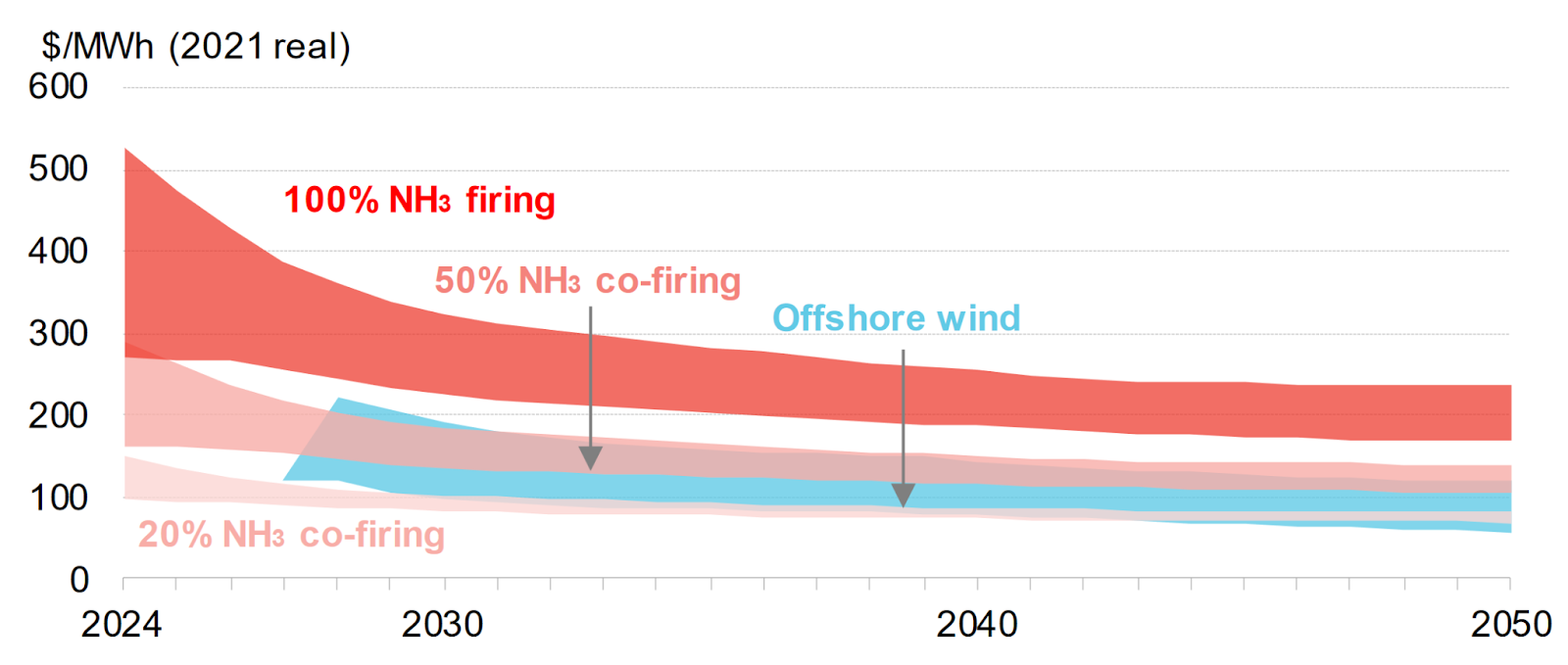

BloombergNEF notes that producing electricity at a coal plant that is burning 50% clean ammonia in Japan in 2030 would still be more expensive than offshore wind.

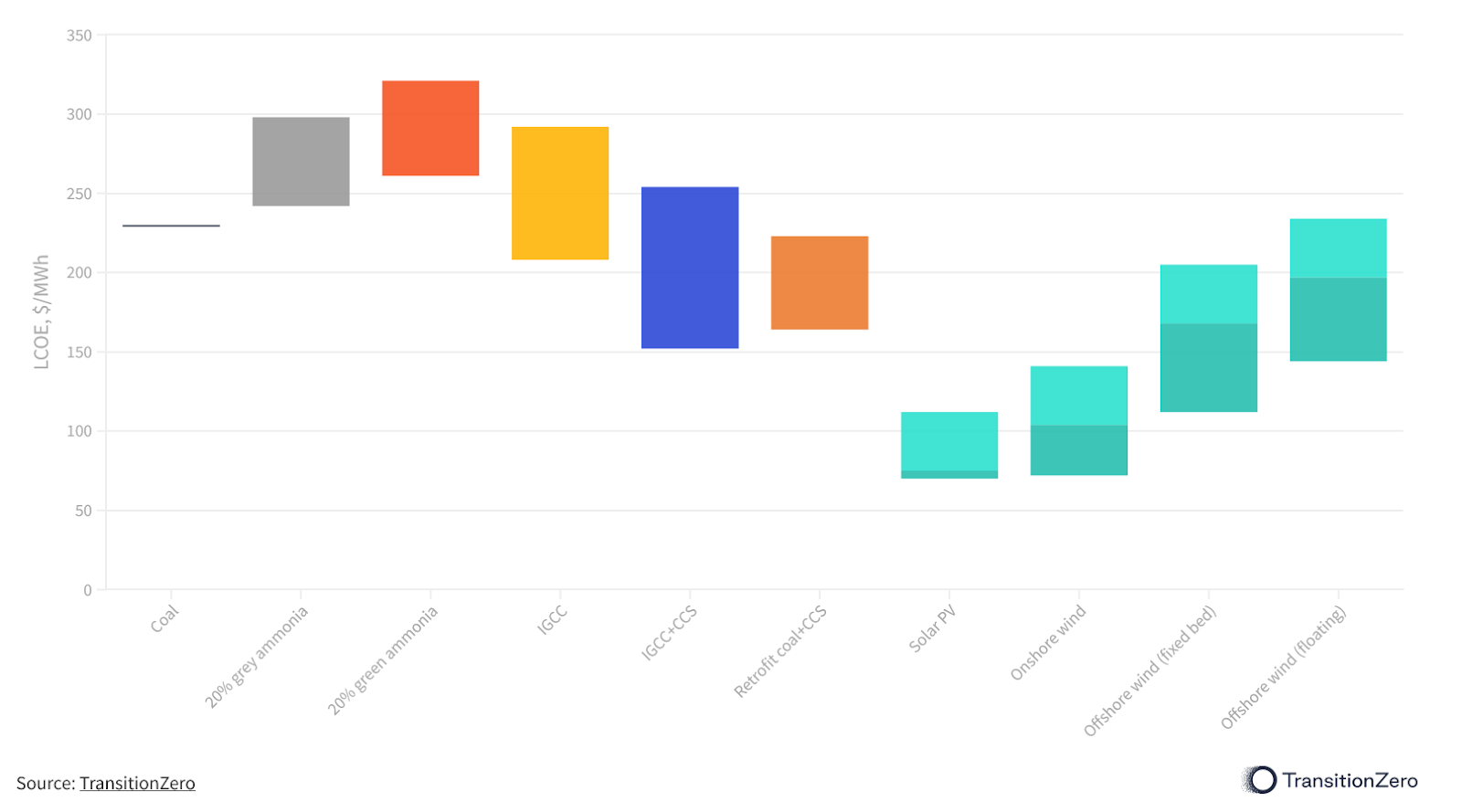

TransitionZero comes to similar conclusions. Coal co-firing schemes using the cheapest ammonia (grey) cost four times more than thermal coal. Using green ammonia is around 15 times more expensive than coal co-firing. CCS also remains a costly technology. It also hasn’t been proven on a large scale and has a “limited impact on global CO2 emissions”, the IEA notes.

So is the case with hydrogen, which remains a widely untested, expensive and inefficient technology.

On the other hand, clean power is already cheaper, with the gap expected to widen by 2030.

TransitionZero warns that the average abatement costs for a 20% ammonia co-firing scheme across the Philippines, Malaysia, Indonesia and Thailand are around four times higher than solar and wind.

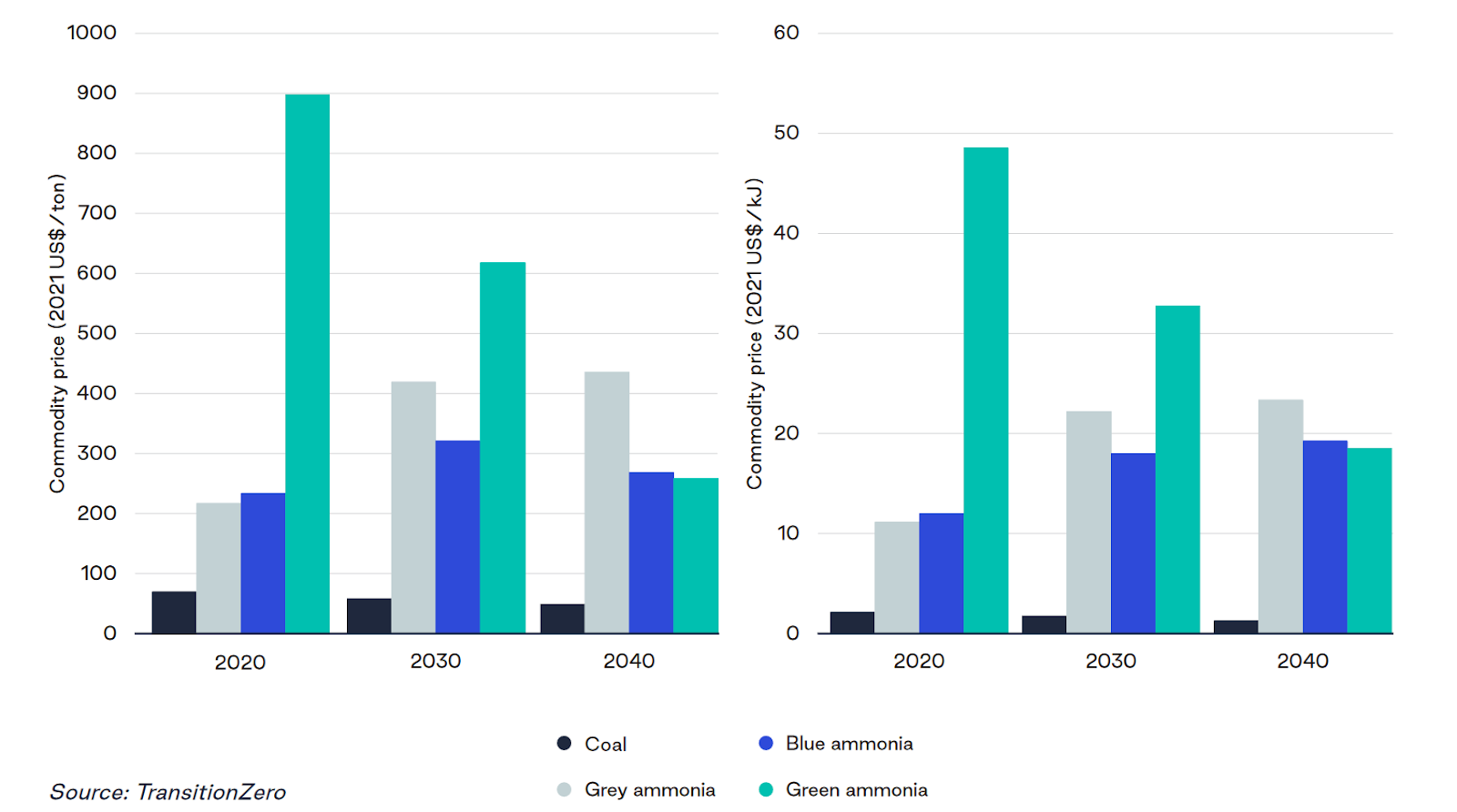

Furthermore, the IEA expects low-carbon ammonia for power generation to remain expensive up to 2030. In some cases, it will be up to 30% higher than regular energy market values.

Along with the significant upfront and ongoing costs, investing in such technologies will lock ASEAN governments into a future of stranded assets.

Increased Energy Dependence

Japan relies on imports to meet nearly 96% of its energy needs. The newly proposed ammonia co-firing plans will also require importing significant amounts of fuel.

The case will be the same for ASEAN countries as well. Aside from Indonesia, none of them have significant ammonia production capacity. Adding to the problems, the ammonia export market isn’t highly diversified. This could lead to ASEAN countries being priced out of the market or failing to ensure adequate supplies.

Furthermore, Japan has a lower energy independence score than many of the ASEAN countries it has promised to help regarding their energy insecurity problems, including Thailand (48.4%), the Philippines (52.3%), Vietnam (62%) and Indonesia (100%).

Health and Climate Change Consequences From Extended Fossil Fuel Use

ASEAN governments should consider that any strategy that plans to extend the lives of coal and gas plants will put wildlife, the environment and communities at risk.

Meanwhile, living near coal power plants can lead to adverse public health implications, including premature and increased child mortality, respiratory disease, lung cancer, cardiovascular issues, reproductive problems and adverse neurological effects. Harvard research has found that deaths caused by gas emissions can be comparable to those of coal.

Embracing Japan’s “clean coal” technology will mean that ASEAN nations will lock themselves into a future of pollution. This would come on top of many already being among the countries with the worst air quality globally.

Japan promotes fossil fuel expansion at home and across Asia even though it already suffers from severe climate change impacts. Yet, those pale compared to what ASEAN countries are facing.

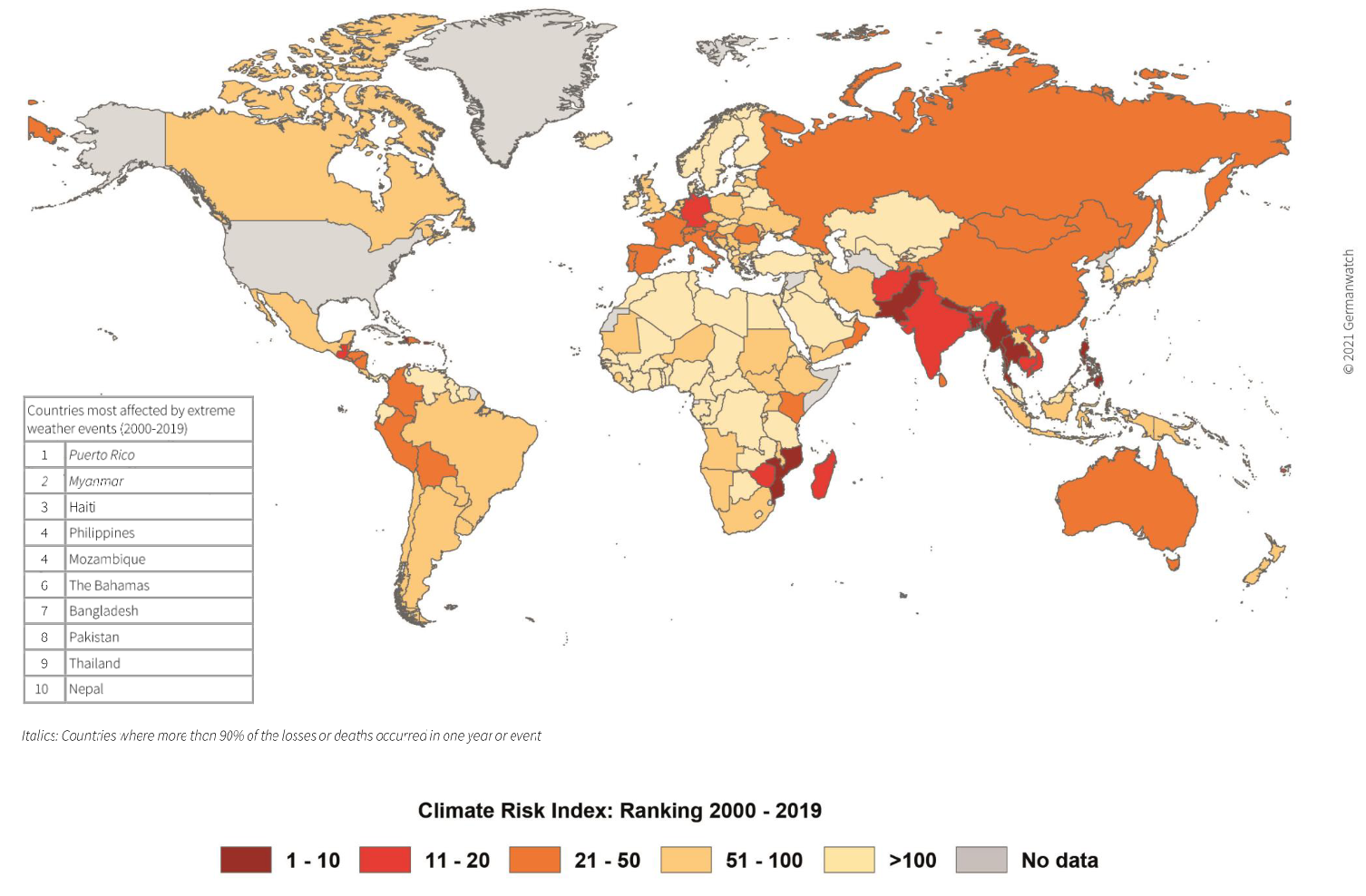

The region is most vulnerable to droughts, floods, typhoons, sea level rise, and heat waves. In the past two decades, Myanmar, the Philippines, Vietnam and Thailand have been some of the worst-affected countries globally in terms of deaths from climate disasters.

Due to climate change, ASEAN nations also risk losing 35% of GDP by 2050.

Vietnam, for example, is among the five countries most likely to be affected by climate change, according to the World Bank. Ho Chi Minh, responsible for 23% of the country’s GDP, is among the most vulnerable global cities to rising sea levels.

The Philippines is at risk of unprecedented compound extreme events. Sea level rise is higher than anywhere else, three times the global average since 1901.

Without urgent action to reduce emissions, heat waves in Indonesia will last almost 8,000% longer by 2050. Climate disasters threaten around 180 million Indonesians living in coastal areas.

ASEAN Governments Risk Facing Public Backlash

Civil society groups, climate activists and various NGOs are already voicing their opposition against Japan’s GX strategy plans.

Over 140 groups from 18 countries sent Prime Minister Fumio Kishida a letter asking to stop expanding the use of fossil fuels and derailing Asia’s clean energy transitions. Locals are also actively campaigning against the country’s extended fossil fuel support plans.

For organisations like CEED in the Philippines and Friends of Earth in Indonesia, Japan’s efforts to export its GX strategy resemble what the country did with coal in these respective countries. Describing it as a “greenwashing exercise,” the groups accuse Japan’s government of treating their countries as testing grounds for its fossil-based technologies.

Furthermore, some LNG projects financed by Japanese banks risk destroying ecosystems and livelihoods. This includes the Verde Island Passage project, taking place in the world’s richest marine biodiversity hotspot.

On a local level, ASEAN governments that decide to pursue Japan’s GX strategy are also likely to fall under public scrutiny and be held accountable for prioritising the interests of the fossil fuel lobby instead of their own.

ASEAN governments looking to embrace Japan’s energy policy should also consider the reaction of the G7 against it. Japan’s fixation on fossil fuels and its “clean coal” plans have been heavily criticised by the rest of the G7. G7 officials challenged its GX strategy, reportedly blaming it for prolonging the use of fossil fuels and referring to the country’s efforts as an “obstacle” in the group’s energy transition agenda.

Renewable Energy as a Way For ASEAN Countries to Ensure Cleaner, More Stable and Affordable Power

In 2022, solar power helped China, India, Japan, South Korea, Vietnam, the Philippines and Thailand save USD 34 billion in coal and gas imports.

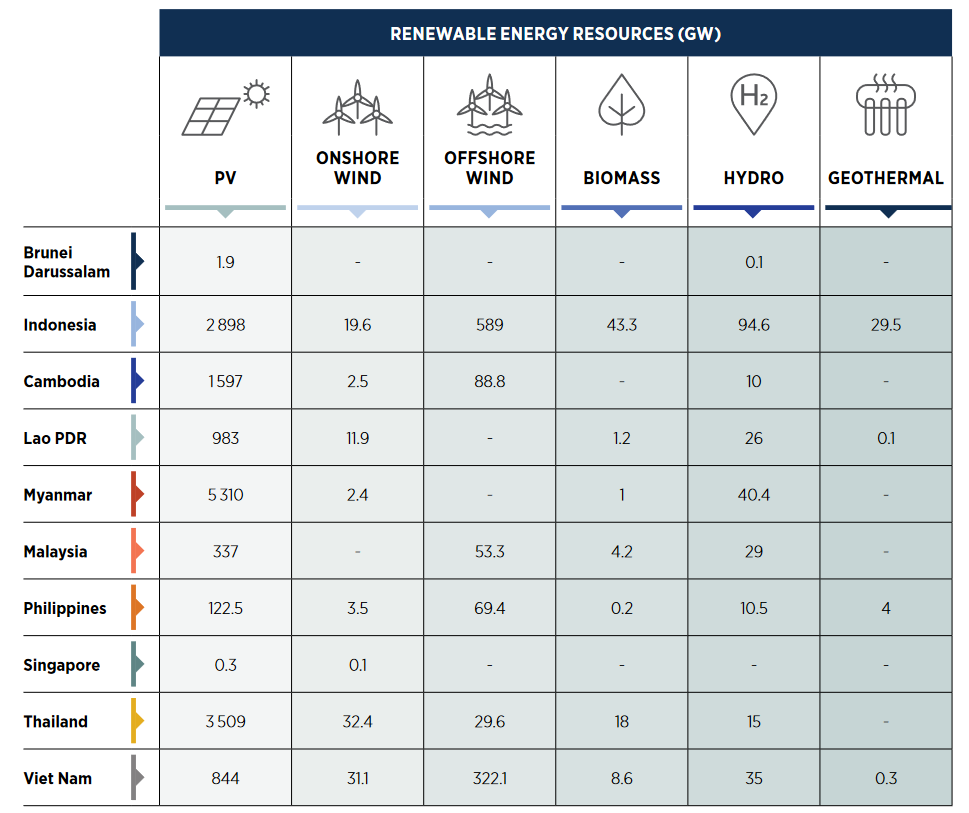

ASEAN countries share one key characteristic: the abundant, untapped technical potential for clean energy capacity.

IRENA finds that the region can transition from just 19% renewable energy share in final energy in 2018 to 65% by 2050. It can slash power sector emissions by 75% and reduce energy costs by USD 160 billion. Avoiding costs related to health and environmental damage caused by fossil fuels can accumulate savings of up to USD 1.5 trillion cumulatively by 2050.

Furthermore, renewables are the cheapest power option in much of Southeast Asia. Paired with the short time-to-market of such projects and the stable transmission networks already existing in many ASEAN countries, governments have a cheap and quick sustainable solution that will also cement their energy independence and empower their growing economies.

As Alden Meyer, senior associate at E3G, says: “You can’t embargo or shut off the sun or wind. The key to ensuring energy and climate security is switching to renewables.”

In that sense, ASEAN countries have no incentive to engage with Japan’s self-interested promotion of fossil fuel-based technologies.

While Japan can serve as a role model for ASEAN governments in many aspects, climate policy isn’t one. The country must set a better example if it wants to influence the region in a positive way.

by Viktor Tachev

Viktor has years of experience in financial markets and energy finance, working as a marketing consultant and content creator for leading institutions, NGOs, and tech startups. He is a regular contributor to knowledge hubs and magazines, tackling the latest trends in sustainability and green energy.

Read more