Indonesia Energy Transition Outlook 2024: In Light of the JETP

15 January 2024 – by Viktor Tachev

The very individual circumstances make Indonesia’s energy transition more challenging than the rest of its Southeast Asian peers. However, the country’s vast clean energy potential and strong economy ensure a stable position for accelerated decarbonisation. The key to unlocking the economic gains of Indonesian energy transition is prioritising the much-needed market reforms to ensure the right public and private financing mechanisms.

Indonesia’s Energy Transition Challenges

Once a rich oil and gas nation, today, Indonesia is the world’s largest global thermal coal exporter. Fossil fuels account for around 80% of the country’s electricity generation, with coal holding a 61.55% share.

It also has the largest fleet of coal-fired power plants in Southeast Asia. However, the bigger problem is that Indonesia’s coal-fired plants are relatively new. Their average age is less than 15 years compared to the 40-year typical lifespan of a coal power plant.

While Indonesia has already started decommissioning coal plants prematurely, there are worrying signs on the horizon. The country is considering making a U-turn from its 2022 national green taxonomy. Under the initial categorisation, only renewable energy projects were considered “green”. However, the IEEFA warns that Indonesian financial regulators could recategorise new coal-powered generation as protecting or improving the environment if the projects were “aimed at the energy transition”. As a result, this could open up opportunities for greenwashing, deter investors and impede the clean energy transition, the agency warns.

According to Climate Action Tracker, the huge fleet of newly operating coal plants has skyrocketed Indonesia’s emissions by 21% in 2022.

Another potential obstacle to the decarbonisation journey of Indonesia is the pursuit of expensive and questionable technologies, such as hydrogen, ammonia and CCUS, while also making them a part of the country’s long-term energy plan. Considering the massive fossil-fuel reliance of the country and the long road it has to go in its transition, Indonesia needs solutions with proven decarbonisation potential that can make an immediate impact, like solar and wind.

The Prerequisites For Indonesia’s Energy Transition To Succeed Are There

Indonesia’s starting position doesn’t mean it can’t unlock a just energy transition and benefit from reduced emissions, increased jobs and a healthier environment. In fact, the country has all the prerequisites to do so, with the gains significantly outweighing the costs.

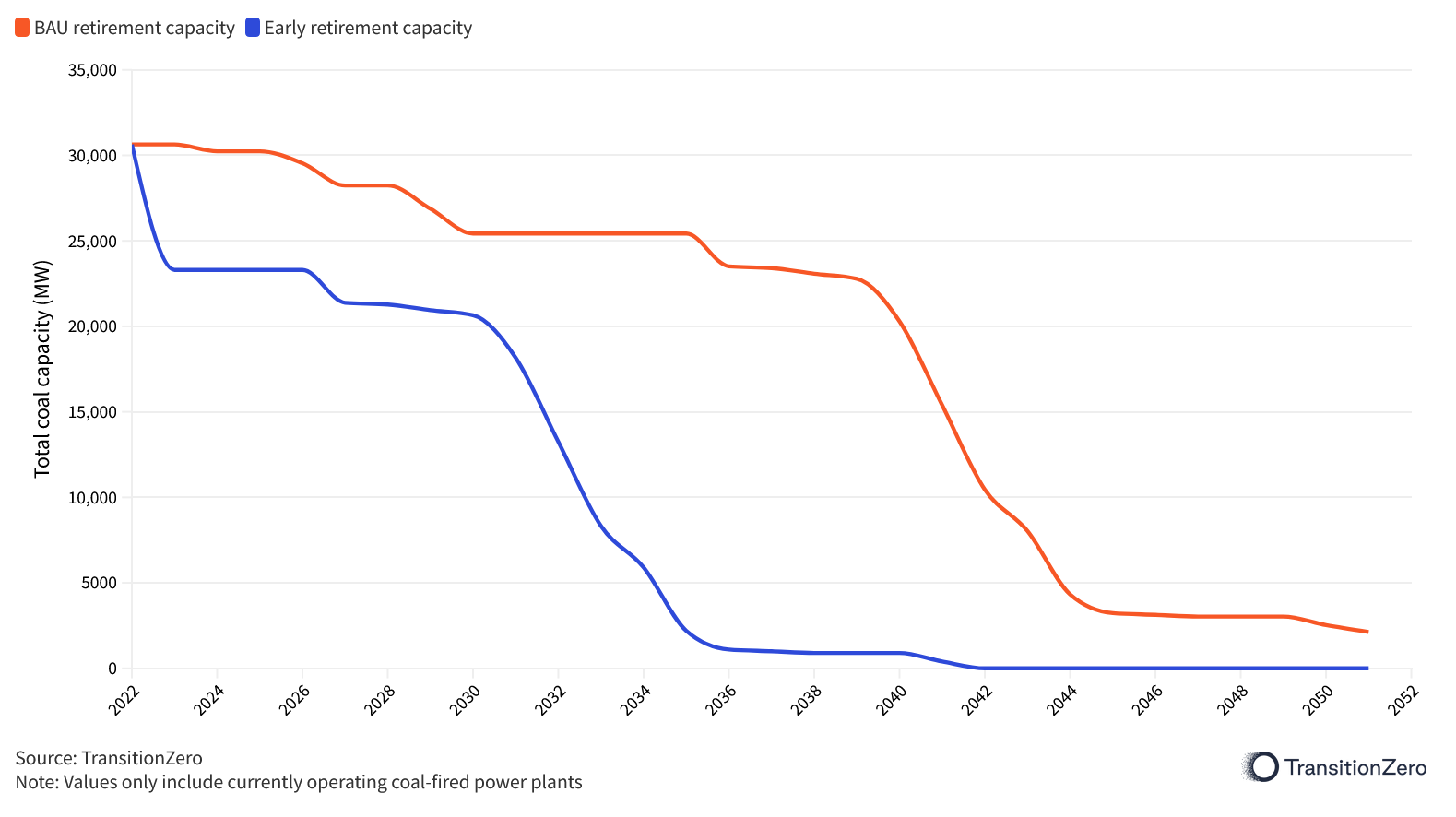

Early Phaseout Cheaper than a Business-as-usual Strategy

TransitionZero finds that Indonesia can close all its 118 coal plants by 2040 in line with the Paris Agreement without incurring massive losses. To do so, it will have to buy out coal power plants before the end of their life cycle and power purchase agreements.

The total cost of the early retirement of Indonesia’s coal plants is estimated at USD 37 billion. For comparison, in 2021, Indonesia paid over USD 10 billion in coal subsidies. Furthermore, in 2022, the country had to budget USD 37.75 billion or 19.87% of its total 2022 expenditure for subsidies and compensation to keep most energy and fuel prices unchanged and protect consumers. According to the EU-ASEAN Business Council, this is twice Indonesia’s 2022 healthcare budget and four times its defence budget.

In its document, the Long-term Strategy for Low Carbon and Climate Resilience 2050, Indonesia’s government plans to retrofit 75% of all coal plants with CCUS. However, such a strategy will also prove expensive. For example, retrofitting all state-owned coal power plants will cost USD 700 billion.

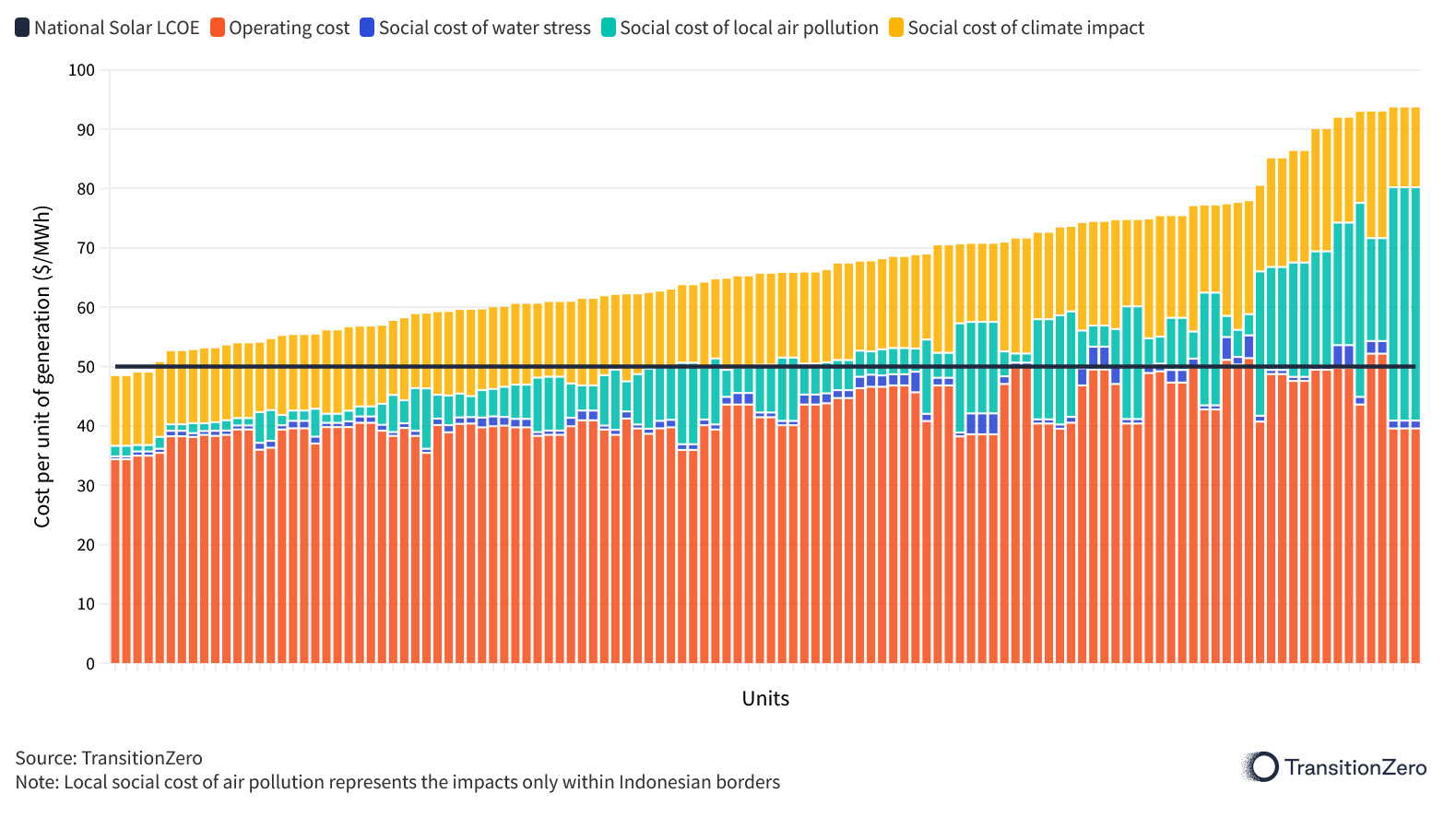

Furthermore, according to TransitionZero, when accounting for air, water and climate costs, the average operating cost of coal is 27% higher than that of clean energy.

At the same time, IRENA estimates that Indonesia’s energy transition requires around USD 16.2 billion in annual investment. By 2030, replacing fossil fuels with renewables will save between USD 15.6-51.7 billion when accounting for air pollution costs.

According to TransitionZero, accessing the right transition finance is the primary condition for the early retirement of Indonesia’s entire coal fleet.

Making the Most of the Just Energy Transition Partnership (JETP)

The USD 20-billion Just Energy Transition Partnership, announced in November 2022, is the developed world’s way of acknowledging Indonesia’s energy transition challenges. The financing mechanism aims to support the country’s economy in transitioning from a fossil fuel-intensive energy system to a sustainable one.

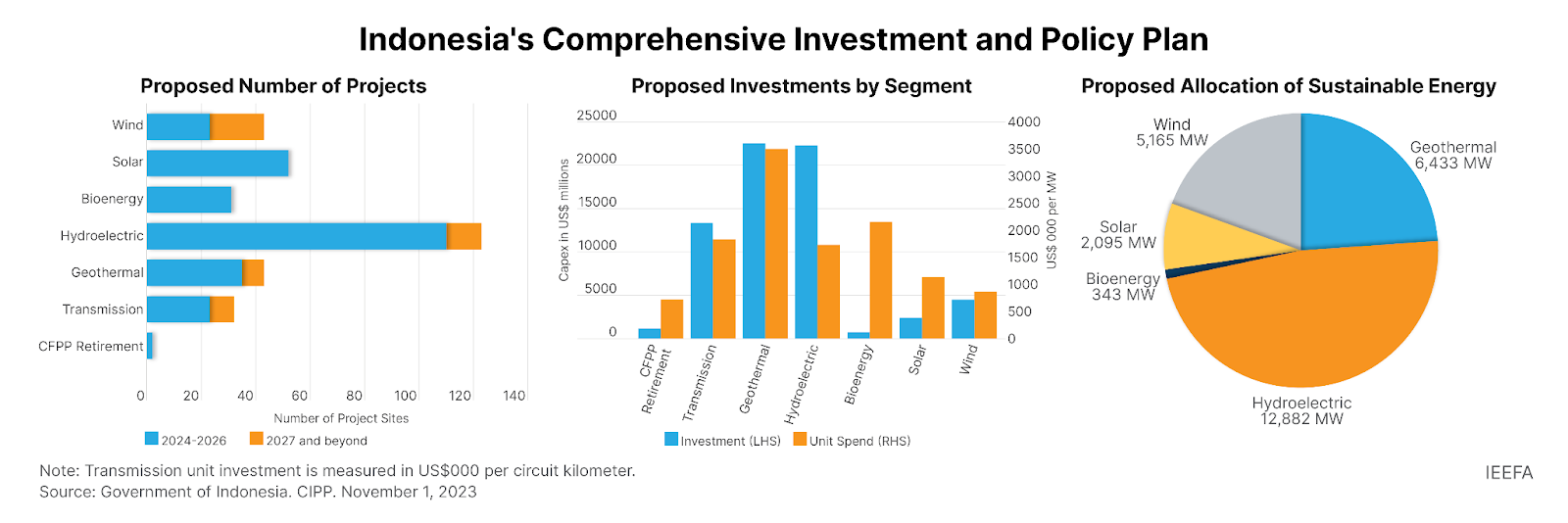

However, it is up to the Indonesian leadership to make the most out of the opportunities. In November 2023, the government made a crucial step by introducing the Comprehensive Investment and Policy Plan (CIPP). The plan collects and details the country’s JETP-related green transition policy and decarbonisation investment needs. For example, it identifies over 400 near-term investments and projects across transmission and distribution, hydroelectricity, geothermal, solar and wind.

The IEEFA’s Grant Hauber says that the government should focus on project prioritisation and pursuing projects with the greatest near-term benefits to reduce risk and increase certainty.

However, the country’s CIPP shows this isn’t the case. For example, solar energy has the least identified projects in the plan despite being the focus of domestic green manufacturing industry development and having the lowest lifecycle cost.

Furthermore, the government should acknowledge that there will be little room for unnecessary investments due to the 400 planned projects identified in the CIPP costing USD 67 billion. The USD 20-billion JETP isn’t nearly enough to finance the decarbonisation needs of Indonesia, meaning that any investments in hydrogen, ammonia and CCUS can prove painfully costly and distracting.

A positive sign is that the government is reportedly in talks with the World Bank and the Asian Development Bank for additional financing for early coal retirement. Since this is an extensive process, whoever wins the election in February should continue the dialogue to ensure that the investment gap can be filled.

Attracting Private Capital

Private capital would prove crucial in filling Indonesia’s transition financing gap. However, to lure investors, the Indonesian government should pursue a transparent and inclusive investment framework that prioritises the needs of investors and affected communities. Alternatively, one that abandons the fossil fuel lobby’s interests to pursue scientific evidence and the economic reasoning of renewables.

The government is already moving in that direction. For example, Indonesia is among the success stories regarding the use of subsidy swaps. Due to moves like this, Indonesia’s leadership has ensured that some of the savings from fossil fuel subsidy reforms will help fund the clean energy transition.

Capitalising on the Indonesia’s Immense Renewable Energy Potential

The Ministry of Energy and Mineral Sources of the government of Indonesia estimates Indonesia’s solar power potential at 207 GW, while other sources see it as up to 500 GW. Yet, currently, the country has deployed just 291 MW. The case is similar when it comes to wind power.

According to Ember, solar and wind’s collective share in Indonesia’s power mix is near zero, compared to a global average of 12%. As a result, the country has one of the highest emissions-intensity rates globally.

Indonesia targeted a 23% share of renewables in the total power mix by 2025 and 31% by 2050. However, under the conditions of the JETP, in November 2023, Indonesia pledged to increase its clean energy generation target to 44% by 2030 and achieve net zero by 2050 instead of the initial 2060 deadline. Yet, just 8% of its renewable power capacity by 2030 will be solar. Instead, the focus will be on dispatchable technologies like geothermal and hydropower.

Currently, the total share of renewable energy, including geothermal, bioenergy, solar, wind, hydro and others, is just 14.5%.

The country can change course by capitalising on its vast clean energy potential. Easing regulatory burdens for project development and attracting green capital will be crucial for this mission. Currently, the annual renewable energy investments in the country sit at USD 1.6 billion, or less than the USD 1.7 billion in yearly savings that replacing fossil fuels with clean power sources can ensure by 2030.

Willingness to Embrace the Energy Transition

Polls reveal that Indonesians are not only on board with the renewable energy transition but are also actively supporting it.

The Southeast Asia Climate Outlook 2023 Survey Report by the Climate Change in Southeast Asia Programme at ISEAS reveals that a majority of the interviewed Indonesians think that their country should stop building new coal power plants immediately. In fact, Indonesian respondents are the strongest advocates of closing coal plants right away.

The locals are also among the most supportive of a national carbon tax and among the most concerned about climate change in the entire region.

Furthermore, Indonesian civil society groups have voiced their concerns about the plans for adopting technologies that will extend the life of fossil fuels in the country through a petition against the Japanese government. Activists even accused Japan of treating Indonesia as a “testing ground” for its dirty fossil-based technologies.

Crucial Months Ahead: The February Elections To Be Pivotal

Indonesia’s government has made notable progress in accelerating the energy transition towards net zero emissions and the economy’s decarbonisation in recent years. As per the IEA’s 2023 World Energy Outlook, Indonesia will become one of the leading solar panel exporters globally. Furthermore, the country aims to become a key player in EV and battery production.

However, much more is needed, and Indonesia’s leadership post-February will have a lot of work to do. A crucial step is introducing the needed market reforms laid out in the CIPP to help ensure a more competitive position for renewables.

Fixing the loopholes in the CIPP is another imperative step. Among them is prioritising dispatchable renewables like hydropower and geothermal, which are more expensive and have a longer time-to-market in comparison to solar and wind. The massive loopholes for building off-grid coal plants and the fact that just 1.4% of the JETP funding will come in the form of grants, which risk burdening Indonesia with debt, are other crucial points worth addressing.

Last but not least, the new government will have to make sure that the country’s plans for increased new coal and gas capacity buildup remain just on paper. Considering Indonesia’s strong industry interests, this won’t be a popular solution. But it would be a much-needed one to unlock green financing, attract private capital, and ease the burden of high energy prices for the economy and consumers.

by Viktor Tachev

Viktor has years of experience in financial markets and energy finance, working as a marketing consultant and content creator for leading institutions, NGOs, and tech startups. He is a regular contributor to knowledge hubs and magazines, tackling the latest trends in sustainability and green energy.

Read more