Natural Gas Price Forecast 2025: Asia To Drive Global Demand

17 February 2025 – by Viktor Tachev

The IEA’s Gas Market Report for the first quarter of 2025 is out, providing natural gas-dependent countries with yet another reminder of energy market experts’ warnings. The expected price volatility, paired with the increased reliance on LNG imports, will undermine countries’ energy security and ability to ensure stable supplies. According to the report, the recent uncertainty around the natural gas market will extend into the first half of the year, a significant blow to Asian countries that will drive global natural gas demand and affect those with gas infrastructure expansion plans globally.

IEA’s Q1 Natural Gas Price Forecast 2025: Demand To Continue Increasing, Markets to Remain Unstable

The IEA’s Gas Market Report for the first quarter of 2025 reveals that on the demand side, global natural gas consumption reached an all-time high in 2024. The estimated year-on-year growth reached 2.8% – higher than the 2% average rate between 2010 and 2020. In total, natural gas met around 40% of the global increase in energy demand, higher than any other fuel. The trend is also expected to continue in 2025, driven primarily by fast-growing Asian markets.

However, as global demand for gas continues to climb, markets remain fragile, with several factors fueling the uncertainty.

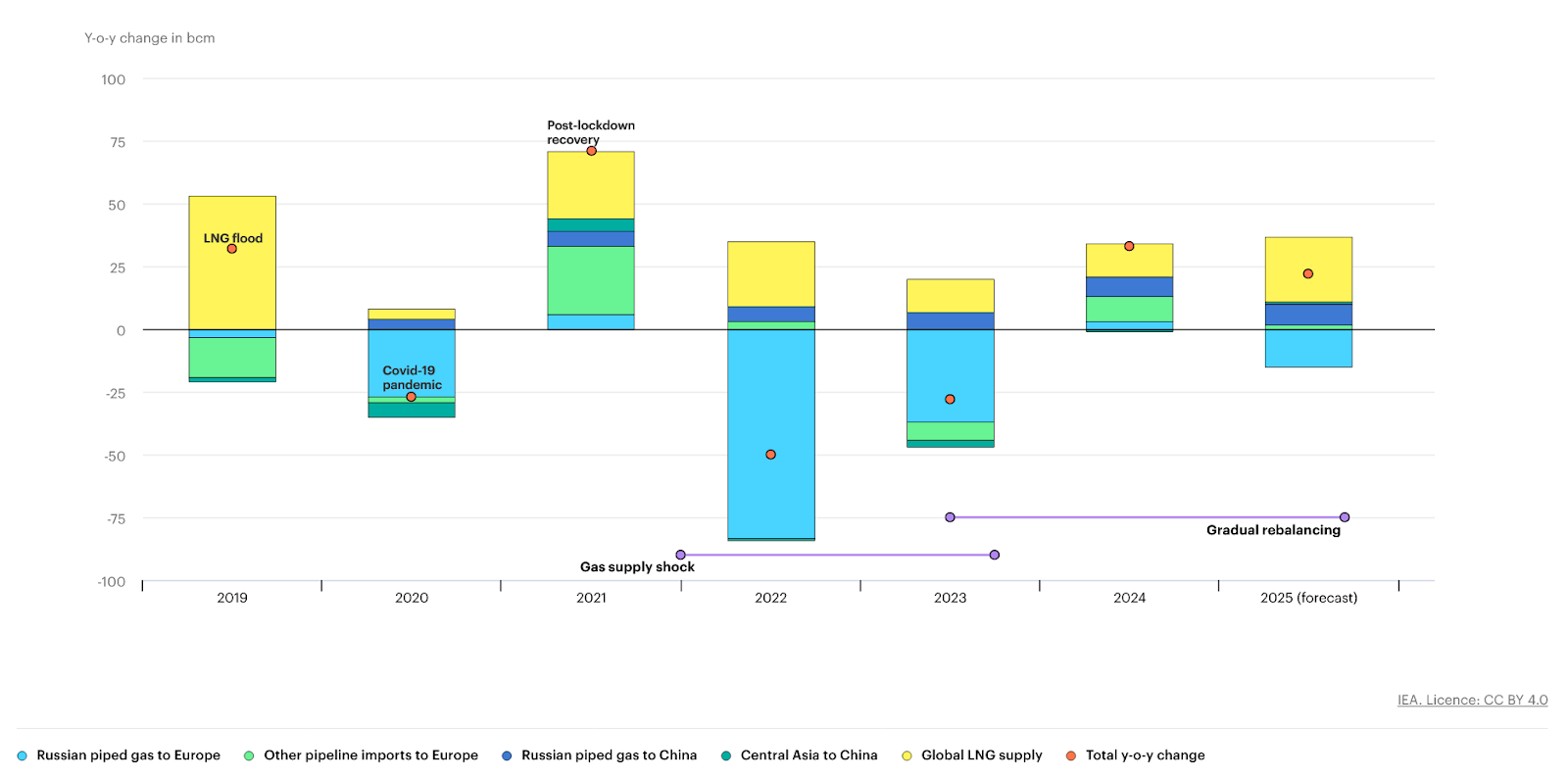

First, the below-average growth in LNG output has limited the available natural gas supply. In total, global liquefied natural gas supply grew by 2.5% in 2024 – a significantly lower rate than the average of 8% between 2016 and 2020. Factors like project delays and feedgas supply issues for some producers led to the situation. According to the IEA, global gas supply will increase to 5% in 2025. Yet, the susceptibility of natural gas markets to geopolitical instabilities and the resulting fuel price volatility, further highlighted by Russia’s war in Ukraine, will partially offset the growth.

Meanwhile, extreme weather events further fueled market strains in 2024, highlighting the crucial role of stable gas supplies for battling heat and ensuring electricity security. According to the IEA, the sensitivity of natural gas demand to weather changes, including prolonged cold or hot periods, is increasing. This was highlighted by a series of extreme weather events across the US, India, Brazil, Colombia and European countries. In those countries, gas-fired power plants provided backup to the power system, which also led to draining gas storage infrastructure.

Asia: The Main Driver of Natural Gas Demand in 2024 and 2025

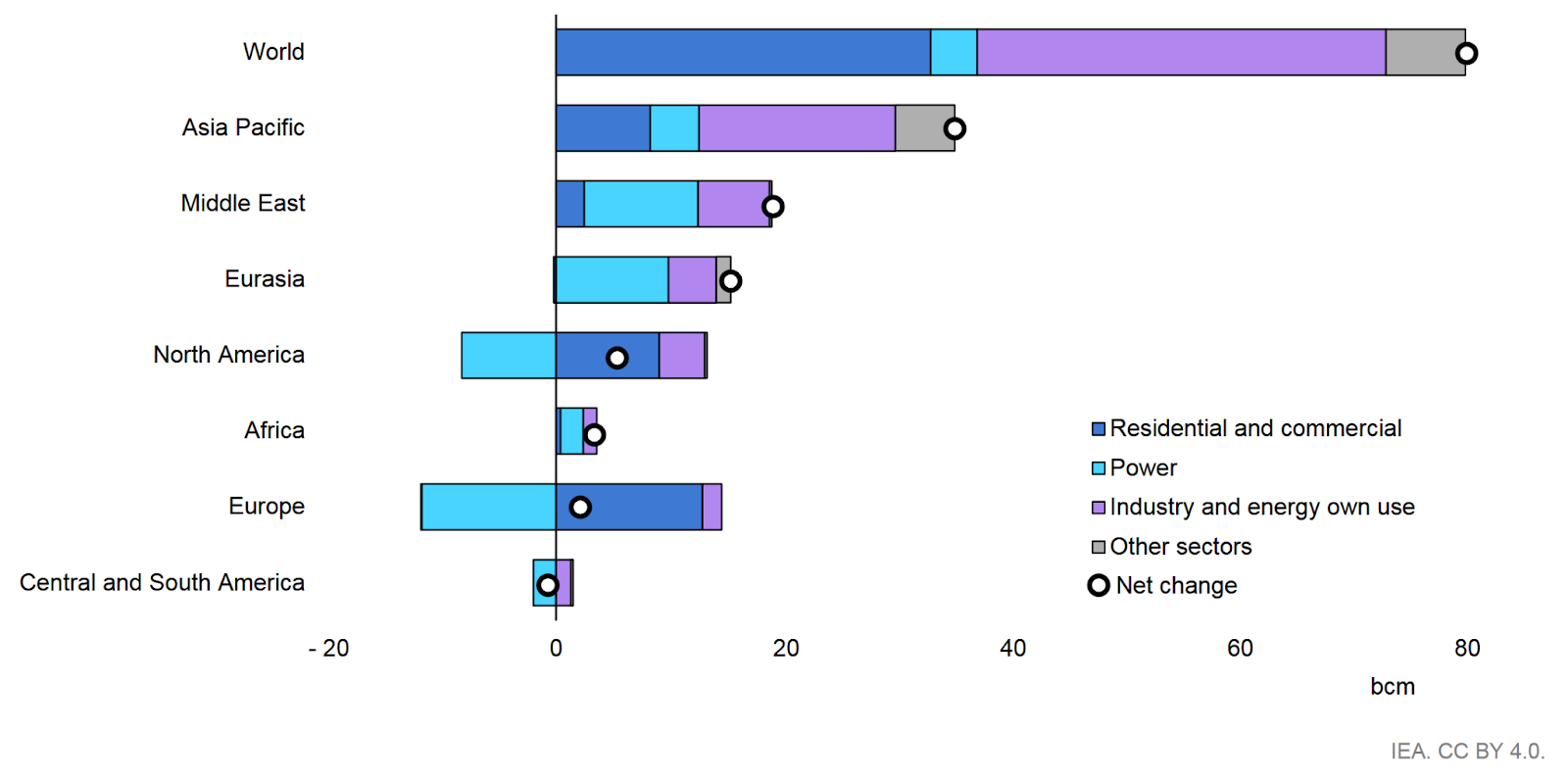

According to the IEA, the relatively strong growth in natural gas demand in 2024 was mainly due to the Asia-Pacific region, which accounted for almost 45%. Demand across most of Asia increased, including China (8%), Korea (7%), India (11%), Indonesia (7%) and Malaysia (8%). In contrast, in nations that recently experienced severe energy crises due to their natural gas import dependence, like Pakistan and Bangladesh, it dropped 1%. Emerging Asia’s gas consumption increased by an estimated 2.5% in 2024.

The agency finds that fast-growing Asian economies will again drive the global demand for natural gas imports in 2025.

However, the IEA warns that factors like geopolitical tension, limited gas supply and weather extremes will all fuel price volatility and cause gas market uncertainty, significantly undermining the energy security of Asian countries. In 2024, price volatility averaged at 40% for Asian countries – 90% above its 10-year average between 2010 and 2019.

The volatility might extend this year due to increased competition for gas deliveries, mainly from Europe. For example, on Jan. 1 gas transit to Europe through Ukraine was halted as the five-year transit deal expired, and Kyiv refused to extend it amid the ongoing war. The IEA finds that the decision shouldn’t pose an imminent supply security risk for the European Union due to its gas diversification strategy. However, it could increase the EU’s LNG import requirements and tighten market fundamentals this year, as European countries might still have to seek additional supplies. As a result, this could negatively affect countries that can’t afford to engage in bidding wars, including many Southeast Asian nations.

The World Bank also notes that Europe’s pivot away from Russian natural gas has increased the bloc’s competition with the Asia Pacific for LNG shipments, representing a clear upward price risk for 2025 and 2026.

Regarding the impact of extreme weather on natural gas markets, various projections and forecasts reveal that Asia will be one of the most exposed regions to extreme heat by 2030 and 2050. Paired with the fact that the weather is warming progressively and every consecutive year of the past 10 has become the hottest in history, along with more frequent, severe and long-lasting heatwaves, the need for countries to ensure the stability of their energy systems has become more crucial. When gas supplies remain insufficient to meet the growing demand, import-reliant Asian nations risk facing greater fiscal pressure as they fight to ensure supplies. For example, just last year, the powerful summer heatwaves in India increased the gas demand for power generation by 32% in the May to July period on year. The incremental gas demand was primarily met through increased LNG imports, the IEA notes.

Asia’s Natural Gas Import Dependence Continues to Deepen

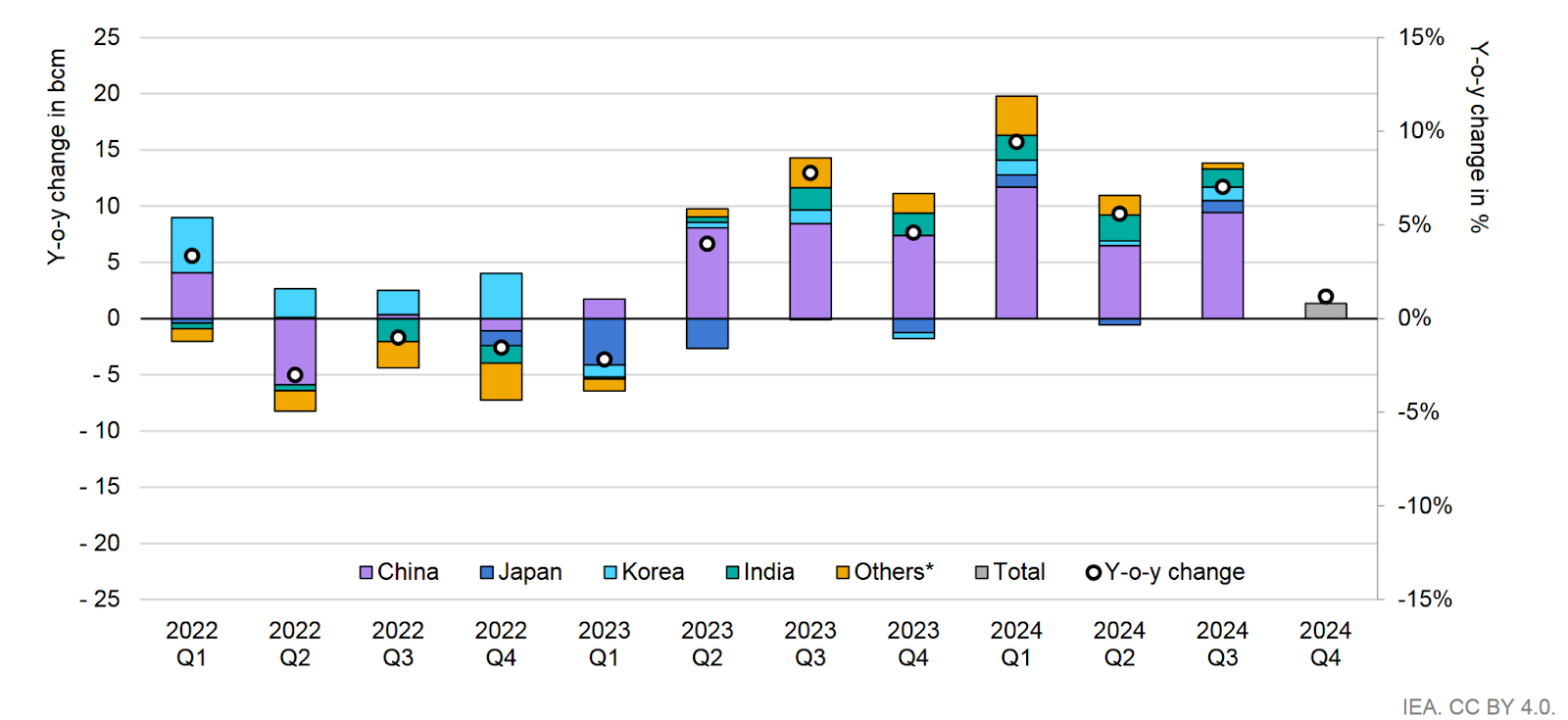

Although Asian gas prices remained over double their historical average in the last quarter of 2024, the IEA finds that Asian buyers continued to dominate the share of contracted import volumes in 2024. LNG import growth in the Asia-Pacific region more than doubled from 2023 levels, reaching 9.3%, the most significant volumetric increase since 2018. China’s imports grew 11%, while India’s 21%. In Japan and Korea, they jumped 1.3% and 7%, respectively.

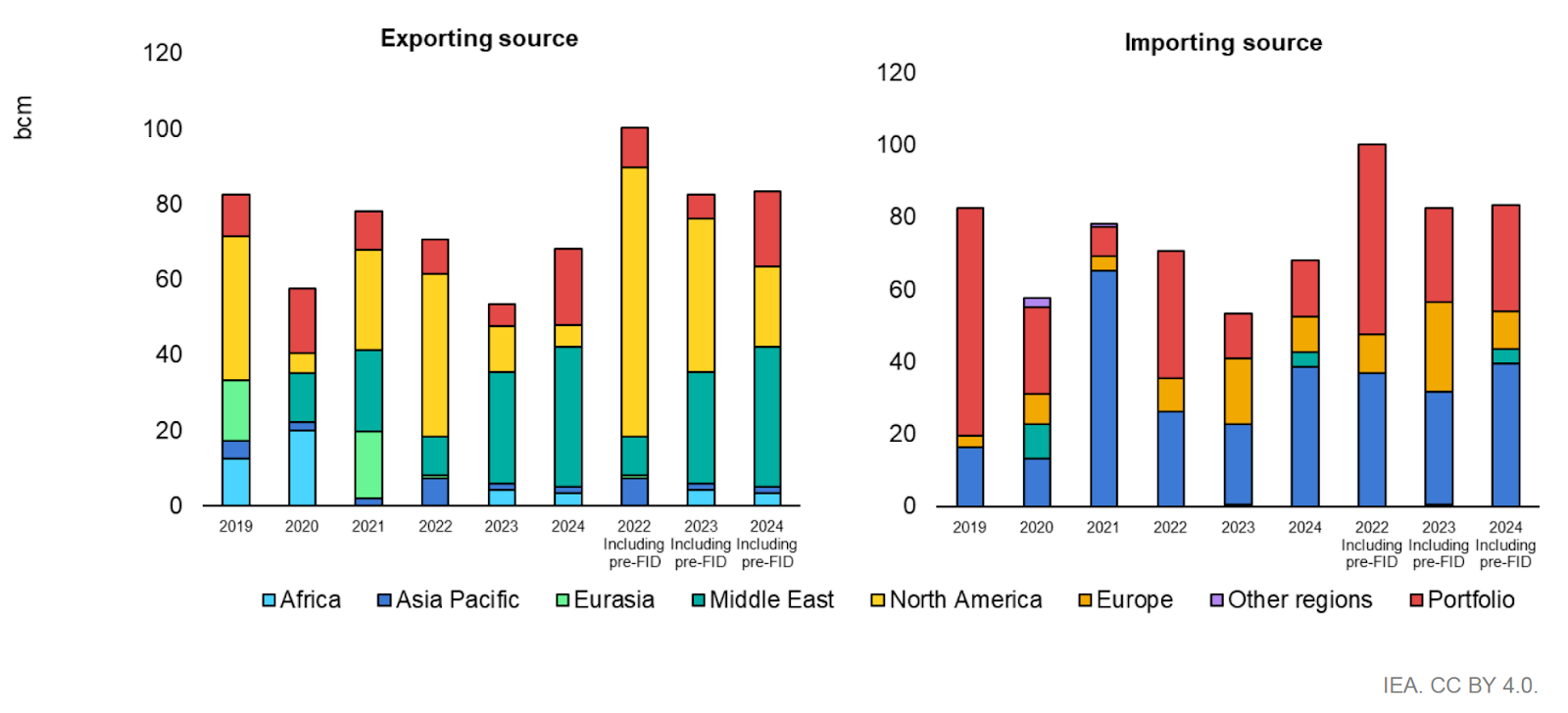

Furthermore, the region accounted for 57% of the volumes signed with post-FID projects. India was responsible for 40% of the contracted volumes, the largest share among Asian buyers. It even surpassed China, which had the largest share (around 70%) from 2021 to 2023.

Asian countries also collaborated to strengthen their natural gas and LNG supplies. Korea’s MOTIE and Japan’s METI agreed to cooperate to secure stable LNG supplies. As part of the initiative, Japanese and Korean companies (including JERA and KOGAS) will explore opportunities for joint procurement, cargo swaps and other forms of cooperation. Singapore is also researching joint LNG procurement opportunities with other Asian LNG buyers.

Asia to Continue Dealing With High Natural Gas Prices in 2025

S&P analysts say that 2025’s energy market dynamics will be more uncertain than every other year since the COVID-19 pandemic. According to McKinsey, LNG prices will remain high in 2025, affecting Asian demand growth.

Reuters’ market analysts also expect high and rising gas prices to raise power generation costs. They warn that the rapidly climbing gas-fired generation costs also raise the likelihood of Asian countries turning to coal, leading to significantly increased emissions as they generate around 55% more emissions per unit of power output. For example, spot LNG costs in Japan are already around 44% above the average coal-to-gas switching price. Reuters analysts also warn that power firms in China, South Korea and other parts of Asia that have the flexibility to use gas or coal for generation will likely opt to raise coal output faster.

The IEA urges producers and consumers to work together to overcome natural gas market instabilities and secure global gas supplies. In addition, Asian nations should accelerate their clean energy deployment plans to limit dependence on expensive and unreliable LNG imports and ensure more affordable, secure, clean and beneficial energy for their growing economies.

by Viktor Tachev

Viktor has years of experience in financial markets and energy finance, working as a marketing consultant and content creator for leading institutions, NGOs, and tech startups. He is a regular contributor to knowledge hubs and magazines, tackling the latest trends in sustainability and green energy.

Read moreOur Publications