Future of Renewable Energy in the World: Massive Growth Expected

22 January 2024 – by Viktor Tachev

What is the Future of Renewable Energy?

The IEA 2023 renewables report reveals that the future of renewable energy in the world is brighter than ever, with a record amount of new renewable energy capacity in the pipeline over the next five years. While the growth trend is positive, to achieve the 1.5°C target, the IEA says that growth should be accompanied by a series of measures to fight climate change. Among them are the policy support and implementation for doubling energy efficiency rates, cutting methane emissions, phasing fossil fuels out and scaling up financing for the needs of emerging and developing economies.

IEA: Over 500 GW Added in 2023, With Unprecedented Growth Expected Over the Next Five Years

The IEA’s Renewables 2023, the agency’s flagship report for renewable energy market developments, reveals that the world has been adding new capacity at an unprecedented rate over the past three decades.

In 2023, a total of 510 GW of clean energy capacity went online. This is over 50% more than in the previous year.

Renewable Energy Sources: Solar Power and Wind Power

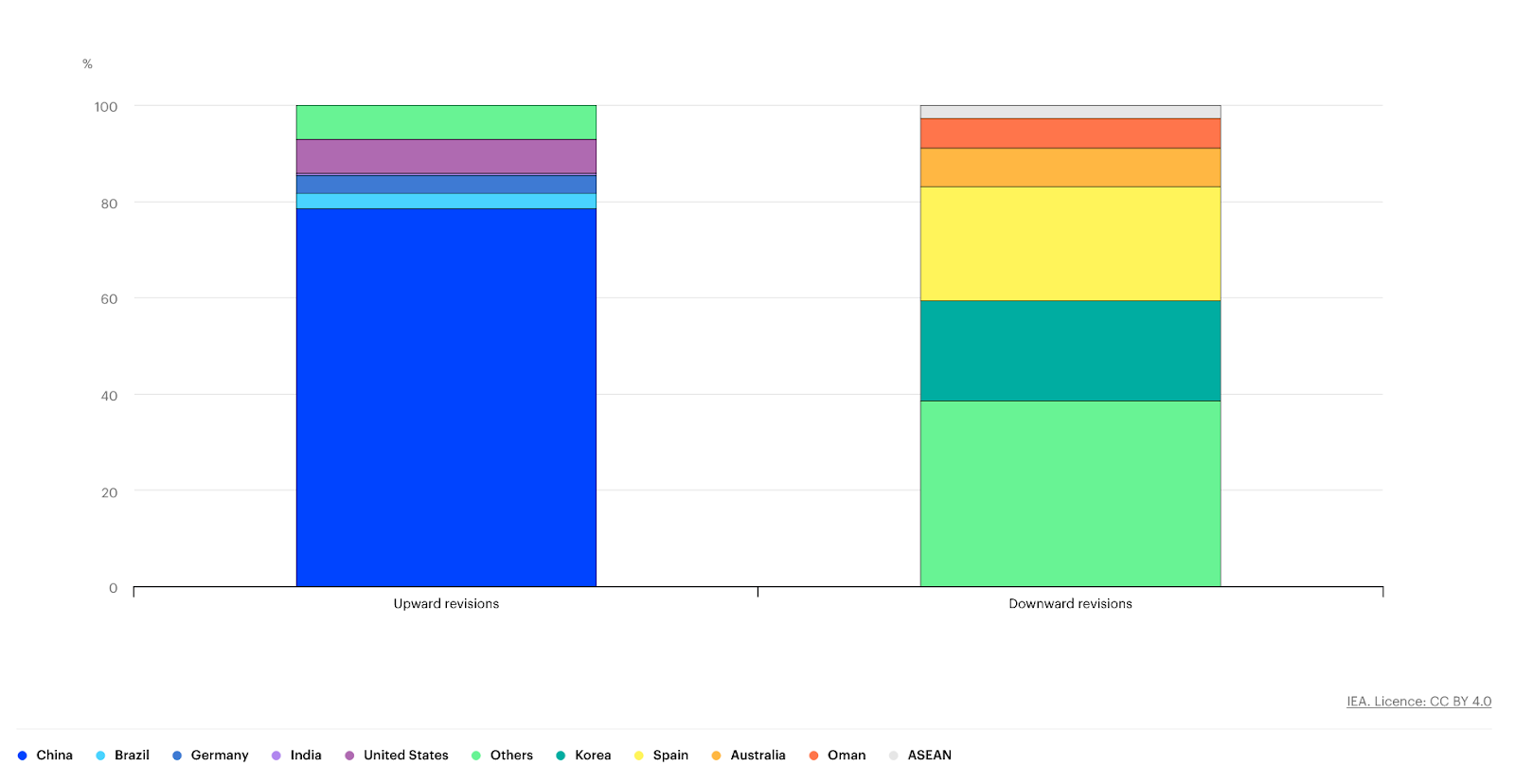

Solar power was responsible for 75% of the new additions. However, just 10 countries were responsible for 80% of global annual additions.

More importantly, the agency projects that over the next five years, we will experience the fastest growth to date.

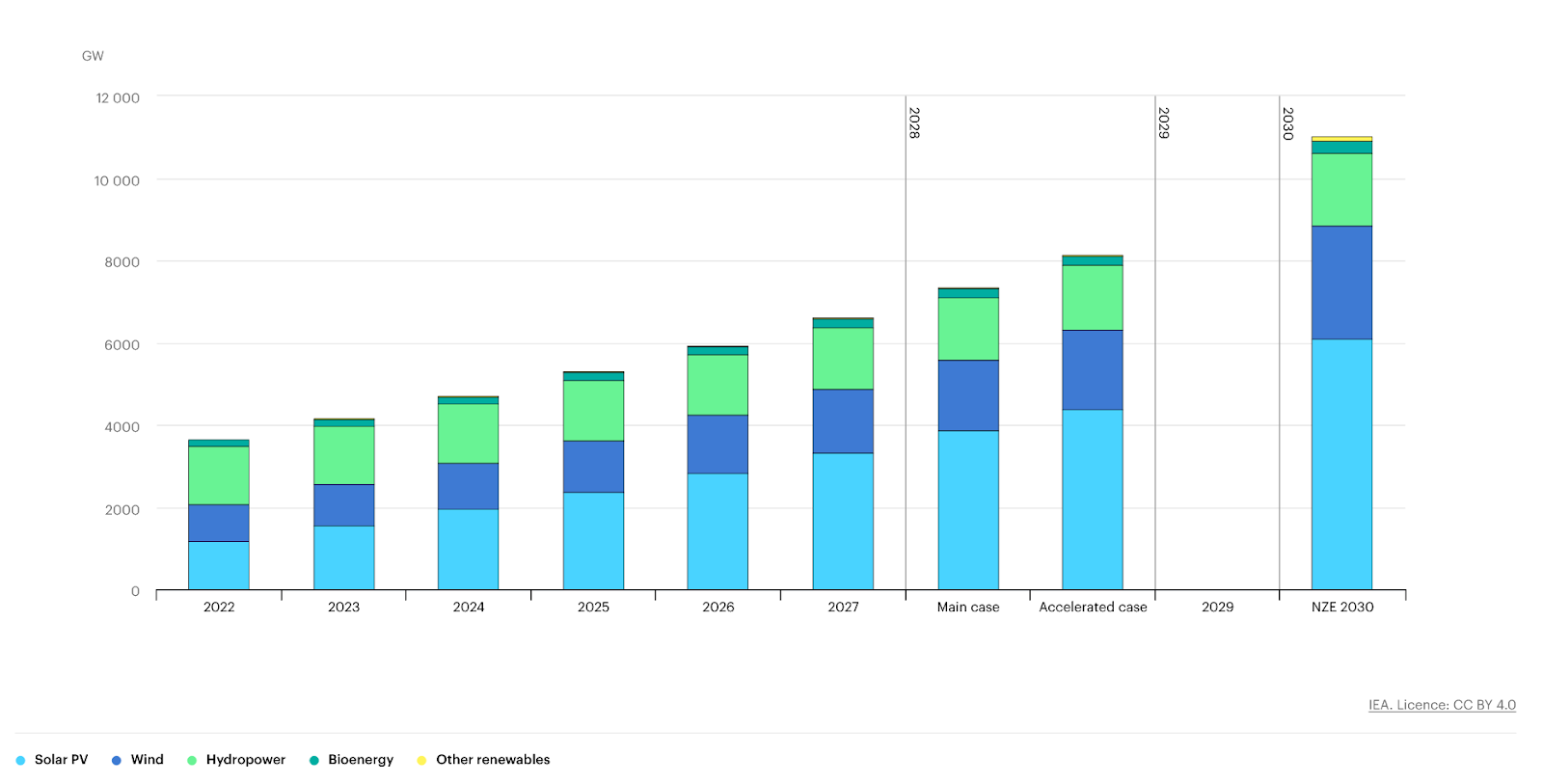

By 2028, the global renewable energy capacity will top 7.3 TW. Solar and wind power will account for 95% of the growth. As a result, renewables will overtake coal and become the world’s largest source of electricity generation by 2025.

The agency finds that throughout 2023, solar PV spot prices dropped by 50%. By the end of 2024, the global manufacturing supply for solar panels will reach 1.1 TW. The potential output will be three times the current demand forecast.

The International Energy Agency (IEA) also states that the projected growth in renewable energy production will not come without its challenges. The main ones include weak policy support and a lack of financing for emerging and developing economies.

The report also remains pessimistic regarding the progress of green hydrogen. IEA’s analysis finds that just 7% of the proposed projects will come online by 2030.

Spotlight On Asia: China Leads While Southeast Asia’s Progress Stalls

Zero Carbon Analytics’ report from December 2023 found Asia demonstrated the fastest growth rate in wind and solar power capacity addition globally. At a remarkable 35% growth rate per year, the sector has outpaced all other regions since the Paris Agreement. The region’s wind and solar energy capacity increased by 300% to over 1 TW since 2015. As of 2022, Asia accounts for 52.5% of global wind and solar power capacity.

However, the progress isn’t uniform across countries.

The IEA’s Renewables 2023 report reveals that Asia’s story is one of leaders and laggards. While the region was once again the main driver behind the global clean energy capacity growth in 2023, not all countries demonstrated comparable progress.

China

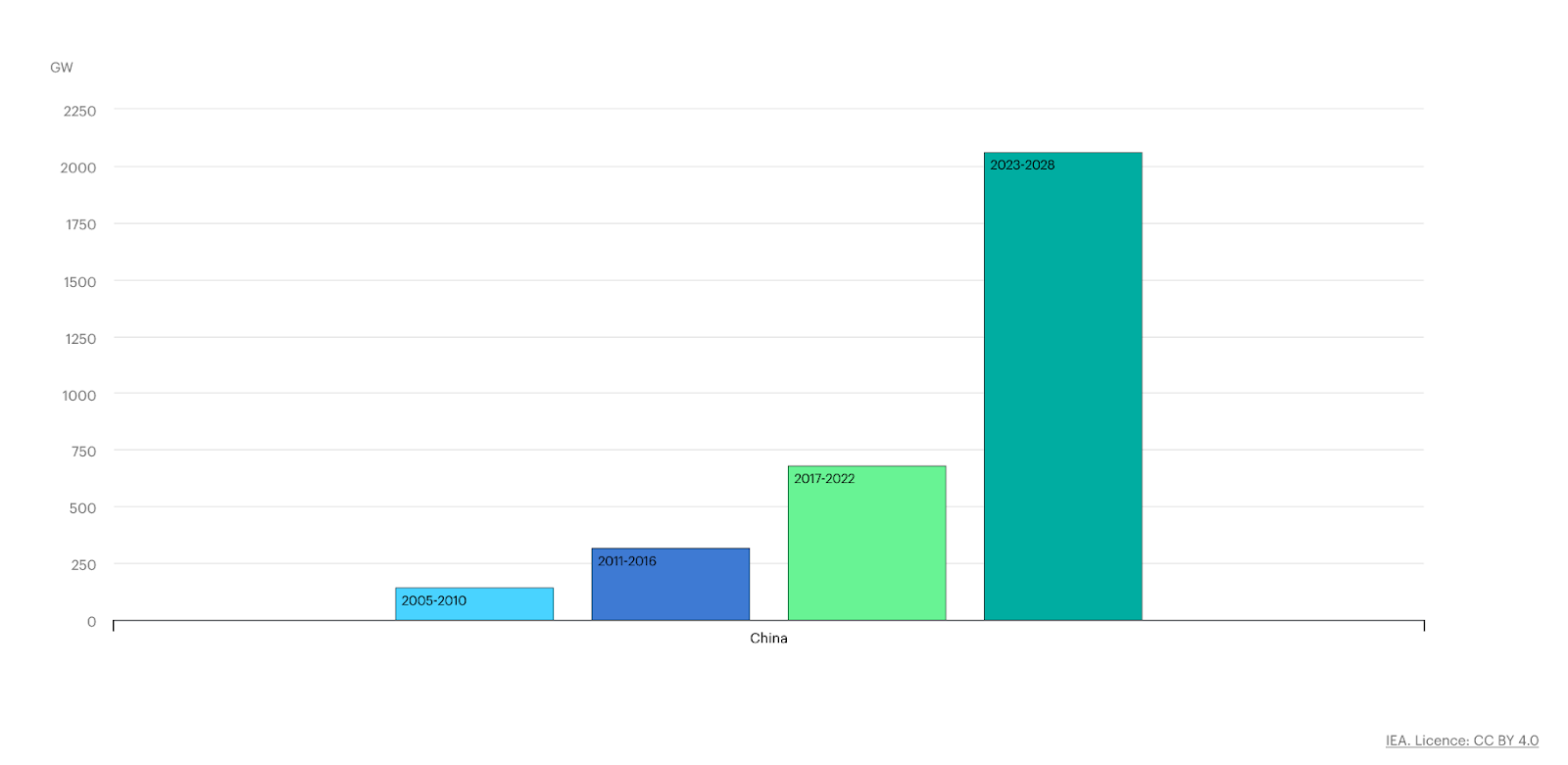

China was again the undisputed leader in new clean power additions, marking the highest amount of growth. Over 2023, it added as much solar power as the entire world did in 2022. Furthermore, its wind power additions jumped by 66% year-on-year.

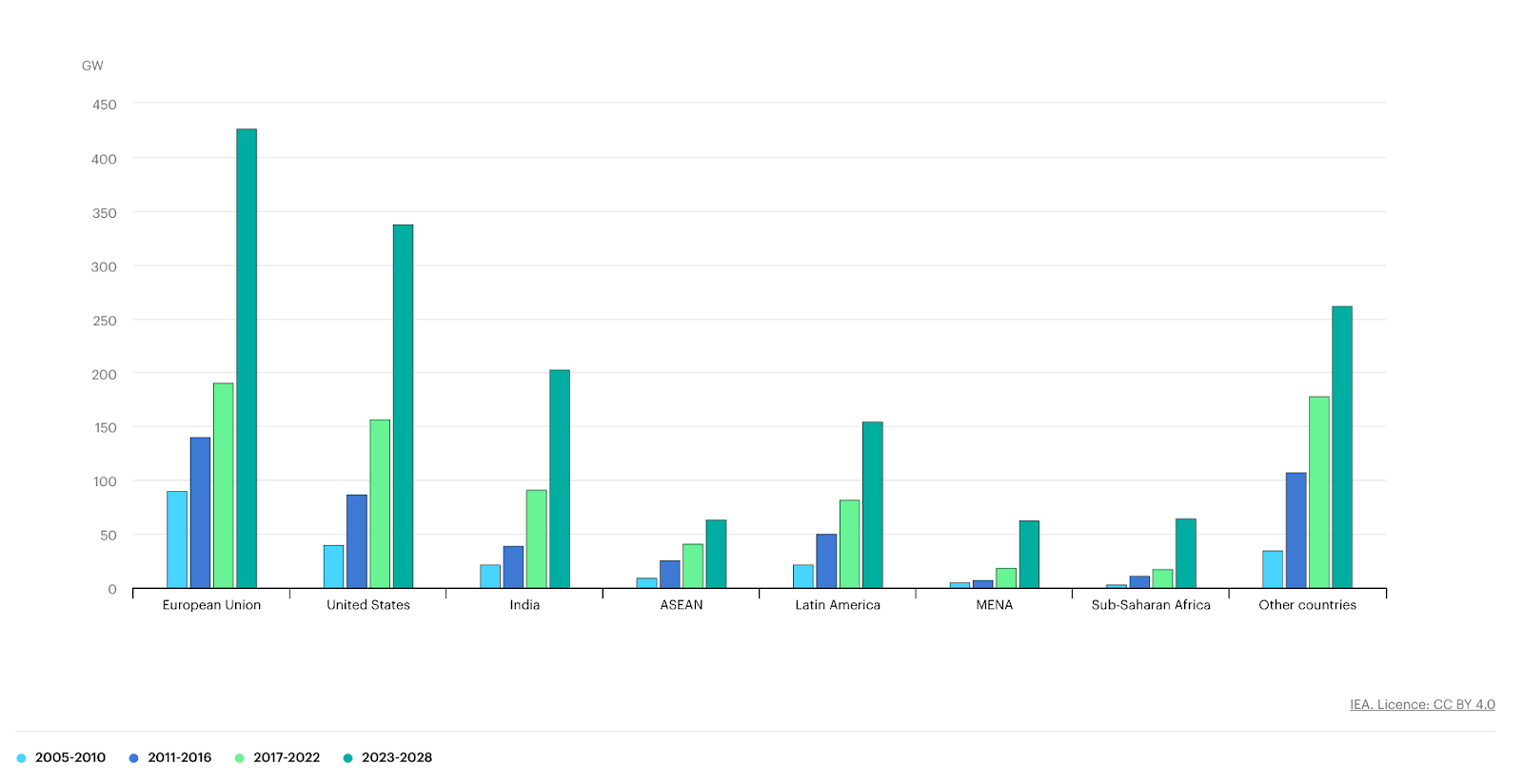

The IEA notes that the country will triple its growth in the next five years. Europe will double it, for reference. The agency estimates that China’s sustainable energy capacity will expand by over 2 TW by 2028, accounting for 60% of the global additions.

China will also retain its leadership position in clean energy technology manufacturing. The country will be responsible for 80-95% of the global supply chains.

India

Between 2023 and 2028, India will double its 2022 cumulative installed capacity, adding 205 GW. This will take the share of solar and wind in the power mix from 11% to 19%.

More importantly, IEA notes that if India addresses existing administrative or technological challenges, the country will be able to install almost 45% more renewable energy capacity. This is the highest upward potential among the world’s largest renewable energy markets.

Japan

Japan is also projected to show increased ambition. Due to renewable projects awarded under the previous feed-in tariff scheme and the newly introduced feed-in premium mechanism, IEA has raised its forecast by 15%.

Japan’s renewable energy capacity is about to expand 47 GW between 2023 and 2028. Solar will account for 80% of it, followed by wind.

South Korea

The IEA slashed its 2022 forecast for South Korea by over 40% due to the government’s strategy to prioritise nuclear energy instead of renewables. Between 2023 and 2028, Korea is expected to add 16 GW of clean energy.

By 2028, renewables will make up 9% of the country’s power generation, up from 5% in 2022. However, the IEA also finds that the country can increase its clean energy additions by 40% through adequate policy support.

Indonesia

Between 2023 and 2028, Indonesia will add 14 GW of renewables to quadruple the growth over the past six years. However, just half of it will come from solar, with the rest from hydropower. As a result, the share of variable renewable energy like solar and wind in power generation will jump from 0% in 2022 to just 3% by 2028.

Additionally, Indonesia will add 1.75 GW of geothermal energy, or half of the global growth during that period.

The Philippines

In the Philippines, the growth in the share of solar and wind in the total energy mix between 2022 and 2028 will be 6%. By 2028, their share will be 9%. Over the projected period, the country will add 9 GW in new capacity – a fivefold increase from the previous period.

However, the IEA finds that by addressing existing issues like grid connection delays, the high cost of financing, lengthy permitting procedures, inadequate transmission infrastructure and grid integration difficulties, the growth can jump by 66%.

Vietnam

Over the next five years, Vietnam will add over 25 GW of renewable capacity. In 2028, the share of wind and solar in total power generation will be 22%, compared to 15% in 2022.

However, the IEA also notes that by increasing grid investments in transmission and distribution and ensuring more ambitious policy support in the form of competitive auctions, Vietnam can add about 45% more capacity.

The COP28 Goal: Tripling Global Renewable Capacity by 2030 Hinges on Policy Support and Implementation

The IEA’s analysis notes that the massive expansion of renewable power that has taken place in 2023 opens the door to achieving the COP28 goal of tripling global renewable energy capacity.

However, even though the world will experience unprecedented growth in new clean energy additions, these will only take global capacity to 7.3 TW by 2028. Alternatively, this will be 2.5 times the current level by 2030. However, this falls short of the COP28 target for 11 TW of clean power by 2030.

“It’s not enough yet to reach the COP28 goal of tripling renewables, but we’re moving closer – and governments have the tools needed to close the gap,” notes IEA Executive Director Fatih Birol.

However, the IEA says that succeeding in this mission requires addressing several issues. While they vary significantly by country, region and technology, the key two factors are ensuring adequate policy support and implementation and scaling up financing and investments. The sluggish progress on those two measures explains why the 2023 growth across developing nations in the ASEAN region remained stagnant, with no changes from the past year.

For emerging and developing countries, the IEA notes that achieving the COP28 target depends on access to finance, strong governance, and robust regulatory frameworks. These factors are essential to reduce risk and attract investment.

Bruce Douglas, CEO of the Global Renewables Alliance, says: “In order to reach the target and spread the benefits of renewable energy equitably, significant low-cost financing must be made available, project permitting must be accelerated and development of strong and diverse supply chains must be facilitated.”

Developing Asia Should Change Course

According to the IEA, the overcapacity of existing coal and gas-fired power plants in some ASEAN countries, including Indonesia, the Philippines, Thailand, and Malaysia, hinders faster renewable energy deployment. Over the last decade, many countries in the region overinvested in conventional generation assets, mainly coal-fired. The region also has a very young fossil fuel-fired fleet capable of meeting electricity demand even in 2028.

As a result, the region doesn’t need to invest in new fossil fuel infrastructure to meet future demand. Yet, developing Asia is poised to drive global natural gas demand in the upcoming years, locking itself into a future of high energy costs and elevated emissions. Furthermore, some countries, including Indonesia, are considering building more coal plants – a strategy many market experts find alarming.

However, Sean Rai-Roche, policy advisor at the independent climate think tank E3G, says that fossil fuels are getting “squeezed out”. “Renewables will soon overtake coal as the largest global source of power generation, which marks a major milestone in the climate fight, given coal is the dirtiest of all fossil fuels,” remarks Rai-Roche. He adds: “This report should act as a wake-up call for any governments still looking to invest in coal – it’s a bad bet with increasing irrelevance for our future power systems.“

Meanwhile, Dave Jones, a program director at global energy think tank Ember, holds hope for renewables. “2024 will be the year that renewables changed from a nuisance for the fossil fuel industry to an existential threat,” he says.

The Economic Case of Renewable Energy

Zero Carbon Analytics notes that renewable energy deployment since 2000 has helped Asia save USD 199 billion in fossil fuel costs in 2022.

Furthermore, the costs of renewable technologies continue to fall. The IEA’s report finds that during 2023, spot prices for solar PV modules dropped by 50% compared to 2022. Moreover, the manufacturing capacity today is three times higher than that of 2021.

Furthermore, the organisation notes that onshore wind and solar PV are cheaper than new and existing fossil fuel plants. In 2023, 96% of newly installed, utility-scale solar PV and onshore wind capacity had lower generation costs than new coal and natural gas plants.

In addition, 75% of new wind and solar PV plants offered cheaper power than existing fossil fuel facilities. The IEA notes that wind and solar PV systems will become even more cost-competitive in the next five years.

Looking Ahead

Joyce Lee, head of policy at the Global Wind Energy Council, says, “The IEA report makes it clear that energy policy is holding back the energy transition – not technology, not costs and certainly not ambition.”

Countries like Indonesia, the Philippines and Vietnam have massive clean energy potential. Yet, their targets are lacking, with weak policy support to enable private capital inflows. In that sense, developing Asia should reconsider its focus for the sake of its economy, decarbonisation goals and the population’s well-being.

by Viktor Tachev

Viktor has years of experience in financial markets and energy finance, working as a marketing consultant and content creator for leading institutions, NGOs, and tech startups. He is a regular contributor to knowledge hubs and magazines, tackling the latest trends in sustainability and green energy.

Read more