Oil Market Forecast 2023: Oil To Peak and Renewables To Accelerate

PradeepGaurs / Shutterstock.com

05 July 2023 – by Viktor Tachev

The IEA’s medium-term oil market report sees looming demand destruction for the resource before the decade’s end. By 2028, growth in global oil demand will slow down significantly. The agency cites the boosted momentum behind clean energy adoption and the global energy crisis, which has highlighted the importance of energy security, as the main reasons. Developing Asian countries should concentrate on developing energy policies in line with the new energy system paradigm. Failure to do so risks locking themselves into a future of high power costs and failed climate pledges.

The 2022 Energy Crisis and Its Effects on Asian Countries

The global energy crisis of 2022, escalated by the Russia-Ukraine war, left no country unaffected. However, developed nations were better prepared to withstand it. Wealthier, power-hungry markets, like Europe, continuously won the bidding war for gas deliveries. The inability to bear the high fossil fuel and oil prices wreaked havoc across developing Asia. Many countries closed schools, hospitals, factories and offices to save power and decrease energy consumption. Even those willing to pay above-market rates weren’t guaranteed deliveries.

Due to the high energy prices, Sri Lanka defaulted on its foreign debt. Energy prices in Indonesia rose by 30%. Nations like Pakistan had to bear with extended blackouts lasting over 12 hours. In Vietnam and many other Asian countries, the power disruptions continue to date, threatening the economy and disrupting everyday life. For countries like Bangladesh, analysts see blackouts extending until 2026. After years of focusing on coal while neglecting clean energy, India now faces a high risk of continuous power cuts in the coming years.

Renewables as a Lifeline in the Energy Crisis

According to the IEA, almost 60% of utility-scale solar PV and wind deployment in the next two years will originate in countries with remuneration policies like fixed tariffs, premiums and utility-owned projects.

In a bid to capture the momentum while protecting their economies from price shocks and reducing their dependence on fossil fuel suppliers, governments all across Asia have started actively working on policies to stimulate clean energy adoption.

China

China remains the undisputed leader in renewables expansion and clean energy technology development. Between 2023 and 2024, the country will account for a 55% share of all renewable energy capacity additions. The IEA notes that China is now responsible for the biggest policy-driven renewable capacity expansion.

India

In 2022, India reached a record-breaking 14 GW of new clean power capacity. After a temporary slowdown in 2023, the country is expected to continue on its upward trajectory in 2024. The Indian government also adopted measures to stimulate auction schemes, paving the way for higher clean energy deployment beyond 2025.

India also has ambitious targets for battery storage. Under the National Programme on Advanced Chemistry Cell Battery Storage, the government plans to provide over USD 2 billion in support for the battery industry.

Indonesia and Vietnam

Indonesia is pushing ahead with ambitious policies to stimulate local biofuel production. The move is motivated by energy security considerations and aims to capitalise on greater biofuel use to offset a part of the oil imports.

Alongside Vietnam, it has benefitted from a Just Energy Transition Partnership with donor countries. The financing mechanisms will capitalise on foreign financial support to stimulate clean energy development and the gradual phaseout of fossil fuels.

Vietnam’s generous FiT policy skyrocketed wind and solar PV capacity from 500 MW in 2018 to 25 GW in 2022. However, this also caused grid issues and led to clean power generation curtailment. The government then decided to halt most incentives in the short term to handle the power system situation.

However, new incentives for clean energy investments and development are already in the works, including investment credits, technology R&D support, FiTs, tax stimulus policies and more.

IEA: Oil Market To Peak by 2028

The IEA’s latest report on oil concludes that the oil market for combustion purposes will rise by around 6% over the next five years and peak by 2028. Annual global demand growth will drop from today’s 2.4 million barrels per day to 400,000 in 2028.

The use of oil in the transport sector will start declining after 2026. However, gasoline’s growth will decline after 2023.

A telling sign about the looming decline in the oil market is that China, the second biggest oil consumer globally, will see its oil demand growth peak in 2024 and slow notably onwards.

However, the IEA notes that overall oil demand would continue to rise through the forecasted period. The reason is that particular segments of the oil market are expected to flourish. Among them are petrochemical demand and strong oil consumption growth in emerging and developing economies. Moreover, the agency finds that these dynamics will offset the anticipated contraction in advanced economies.

Global upstream investments in oil and gas exploration, extraction and production will jump by 11% to USD 528 billion in 2023. The IEA warns that the level of investment is not enough to get to net-zero.

Reasons Behind the Crude Oil Market’s Dynamics

The IEA notes that investments in clean energy are accelerating faster than fossil fuels because of the global energy crisis that followed the COVID-19 pandemic and the Russia-Ukraine war.

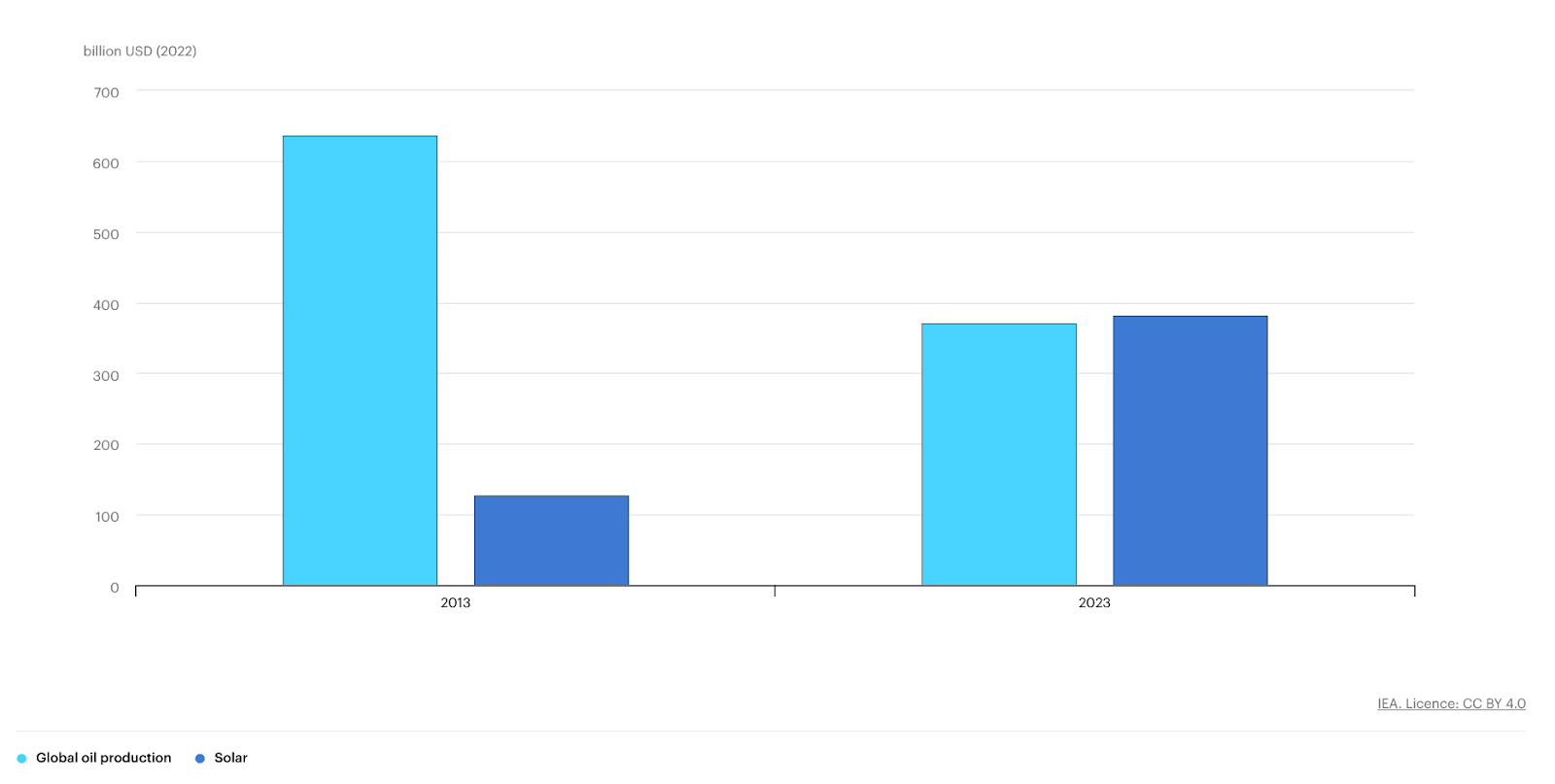

For example, in its 2023 energy investment report, the IEA found that solar investments now exceed oil production investments. The agency identifies the stronger drive by governments towards a low-emissions future and energy security concerns as major reasons for this.

Another reason for the oil market’s slowdown is changes in consumer behaviour. For example, the use of oil for transport fuels will decline due to the switch to electric vehicles, the growth of biofuels and improvements in fuel economy.

Asia’s Changing Market Dynamics: Ensuring an Energy-secure Future

The IEA’s report notes that the Asia-Pacific will account for 90% of global oil demand growth.

India will be the key growth market. The country is expected to surpass China’s total year-over-year oil demand growth as early as 2027. Southeast Asian nations like Malaysia and Indonesia will see a similar trend, with oil consumption to jump by 20% between 2022 and 2028.

The findings resemble Asia’s stance on gas and LNG. While the world is moving away, Asian countries are pushing ahead. However, fossil fuel reliance threatens long-term energy stability and raises serious economic and security concerns. To avoid similar risks, governments should prioritise alternatives.

Learning From Others

To ensure it is better prepared for the next fossil fuel price crisis, developing Asia should learn from the leaders in clean energy policy development, including China, Europe and the US.

EU member states, for example, now see achieving emissions reduction targets as a legal obligation. Aside from union-wide policies, each country is implementing its own policy frameworks, adjusted to the local market’s requirements.

Whether it is France’s EV subsidies program targeting the poorest, the fair and just energy transition plans in Spain and Greece or the Czech and Irish plans for tackling energy poverty, Asian countries have shining examples to learn from. Moreover, many of those policies are designed specifically to address the problems for the poorest parts of the population. Considering that South and Southeast Asia are two of the three regions with the highest energy poverty, these cases should be of particular interest.

Developing Asia can also learn from Europe’s solidarity in times of crisis. The single market and the joint initiatives between member states ensured collective resilience to the turbulent energy market and economic hardships. A region-wide action plan can help Southeast Asian nations become more prepared for crises, regardless of whether they are related to climate change, the energy market or economic disruptions.

Substituting Local Oil and Natural Gas Production with Renewables

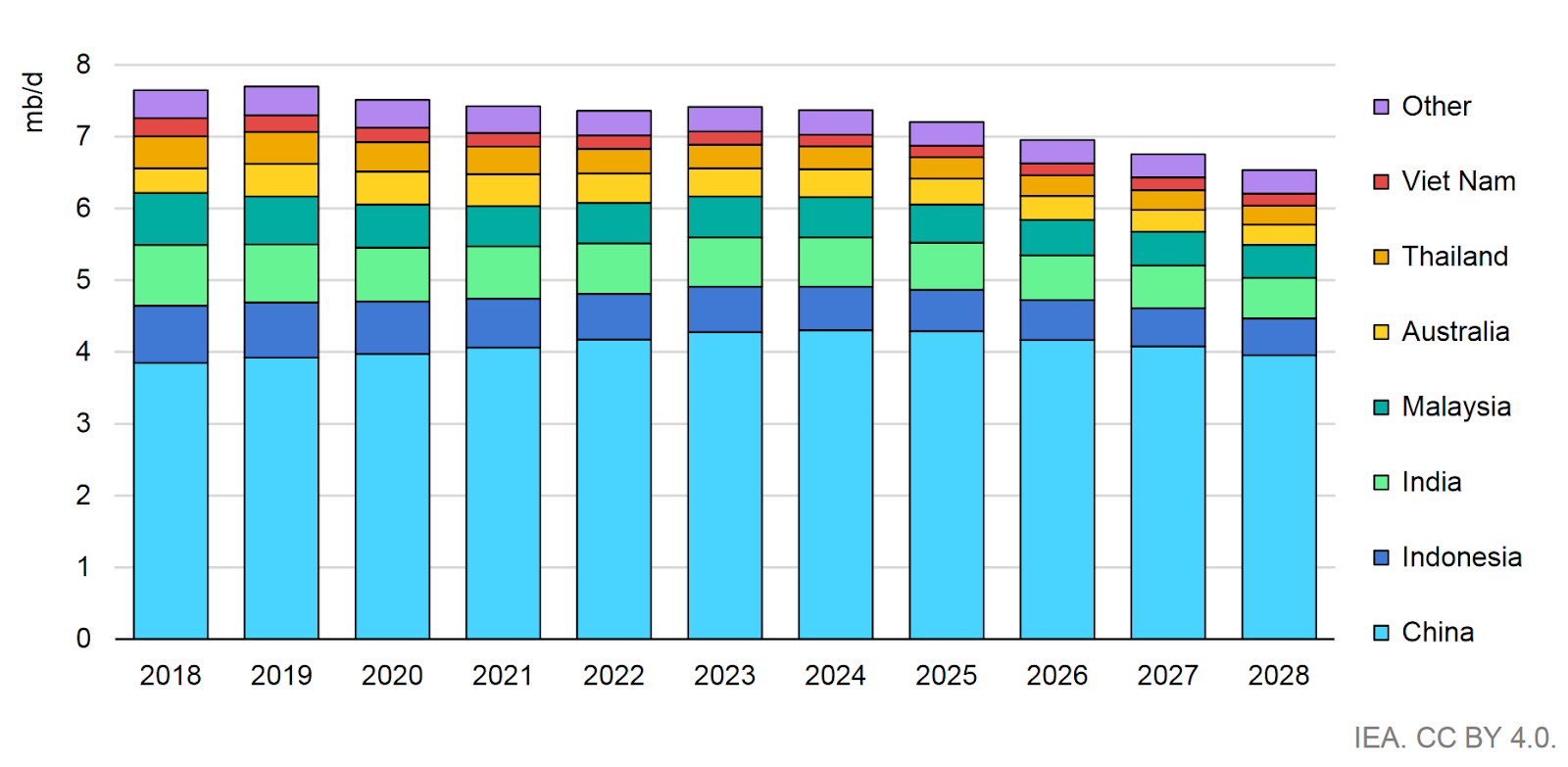

While not among the leading suppliers, Asian nations, including China, Indonesia, India and Thailand will see their oil production drop significantly in the following years. According to the IEA, China, Australia, India, Indonesia and Thailand, will all post significant losses, totalling 690,000 barrels a day, by the end of the forecasted period.

Indonesia’s oil reserves are projected to deplete by around 2030. Malaysia’s will last until 2027. Bangladesh’s gas fields will run out by the early 2030s.

In a nutshell, local production will play a lesser role in Asian countries’ power systems. Governments have already started looking for ways to fill the gap. While many would be willing to lean towards imports, the energy crisis has proven how costly such a move might be. From environmental and economic points of view, the only viable solution is clean energy sources. New solar and wind power is now cheaper than operating existing coal or gas plants, let alone building new ones.

Stimulating investments in renewable energy infrastructure will ease the transition towards a more sustainable and stable energy system that empowers rather than hinders economic growth.

Moving Towards More Sustainable Investments

The IEA’s Executive Director Fatih Birol warned oil producers to “pay careful attention to the gathering pace of change and calibrate their investment decisions to ensure an orderly transition”.

Despite the warnings, the oil and gas industry seems to be doing the opposite. Companies prefer distributing their record-high profits instead of investing in decarbonisation. For reference, just 5% of their total upstream investments in 2022 went to clean electricity, renewable energy or carbon capture technologies.

However, the industry realises that the soaring profits it has benefited from in the past years will only decline. This might lead it to make one final push to lock in power-starving economies with new fossil fuel infrastructure.

Without strong policy support for decarbonisation, developing Asia, which has become a dumping ground for foreign fossil fuels, might crumble under pressure.

However, considering the projected decline in the oil market, investing in new infrastructure will notably increase the potential stranded asset risk exposure. Today, the global stranded asset risk for oil and gas infrastructure is estimated at USD 1 trillion.

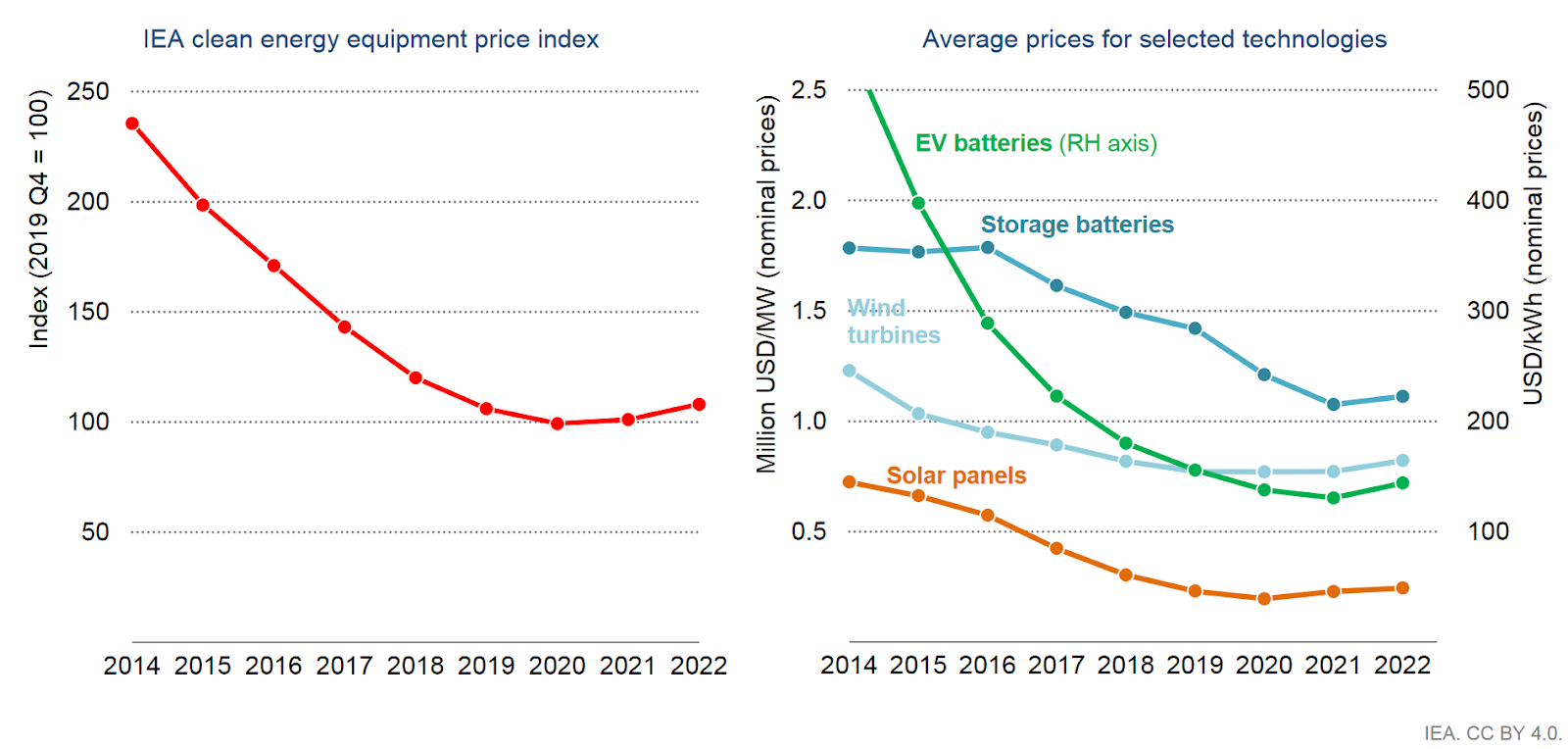

Furthermore, according to the IEA, building new oil infrastructure is now over 22% more expensive than in 2020 due to tightening monetary policy, ongoing labour shortages, higher rig rates and material costs.

At the same time, clean energy technology costs are getting cheaper by the day.

Furthermore, renewable electricity costs fell by up to 90% over the past decade. As a result, Asian countries relying on solar power, including China, India, Japan and more, saved around USD 34 billion, or 9% of their total fossil fuel expenditures, in the first half of 2022.

Oil Demand and Market Dynamics

The IEA notes that coal production has already peaked, while gas demand growth is slowing down. Now that oil demand is declining, everything indicates that the end of fossil fuel use is closer than ever.

After witnessing the drawbacks of extensive fossil fuel reliance, the EU and other developed countries are working to accelerate the transition towards renewables. At the same time, developing Asia remains locked in a carbon-intensive future where its economy’s stability and climate goals are significantly undermined. Whether or not it will change its course depends on its policy decisions. The first signs, at least, are positive.

by Viktor Tachev

Viktor has years of experience in financial markets and energy finance, working as a marketing consultant and content creator for leading institutions, NGOs, and tech startups. He is a regular contributor to knowledge hubs and magazines, tackling the latest trends in sustainability and green energy.

Read more