High Costs and Renewables Surge Weaken Asian Gas Demand Forecasts

19 June 2024 – by Viktor Tachev

Asian gas demand has long been dubbed the engine behind the growth of the global natural gas market. However, a series of factors are now weakening the bullish market forecasts. According to Zero Carbon Analytics, Asian gas demand is starting to slow down, mainly due to the surge in renewable energy deployment. In the long term, the question is not if but how long it will take for countries to transition to cheaper, more secure and cleaner solar and wind power as the backbone of their energy systems while limiting the role of natural gas to a complementary one.

Renewables Are Making Gas Market Growth Slow Down

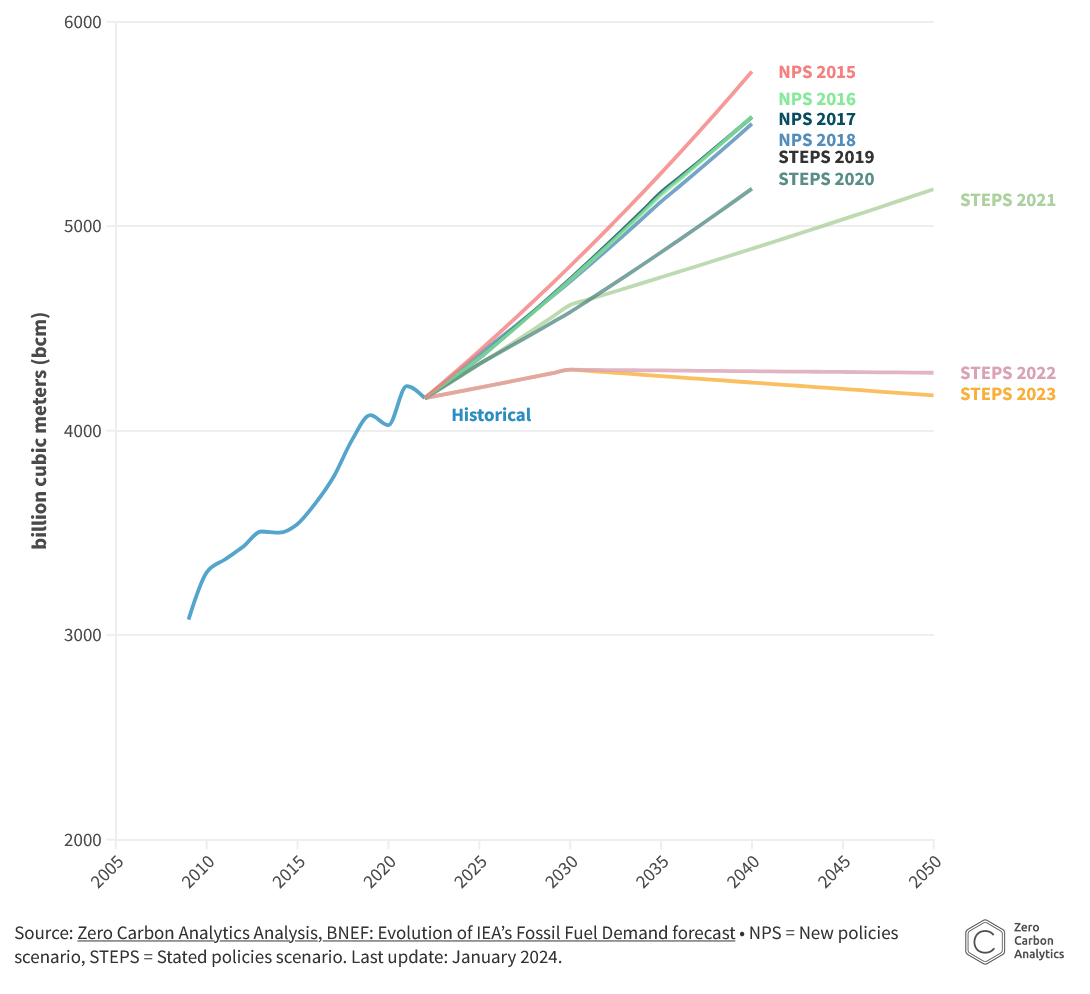

In the 2023 edition of its Global Energy Outlook report, the IEA forecast that gas demand would peak this decade in all scenarios. The reason: the accelerated shift to renewables from leading economies. In fact, between 2015 and 2023, the momentum behind clean energy has made the IEA slash its global 2040 gas demand forecast by 1,500 billion cubic metres.

For Asia, in particular, existing national climate pledges indicate a 40% drop in the region’s gas consumption by 2050.

According to Zero Carbon Analytics, an international research group, shaping a precise forecast for gas demand trajectories is challenging. The reason is the number of variables involved. Some of them include regional and temporal differences in the transition from fossil fuels, major LNG importers’ willingness to reduce their reliance, financial challenges affecting gas infrastructure development, gas price volatility and clean energy power costs getting cheaper by the day.

Asia Remains the Leading Natural Gas Growth Market

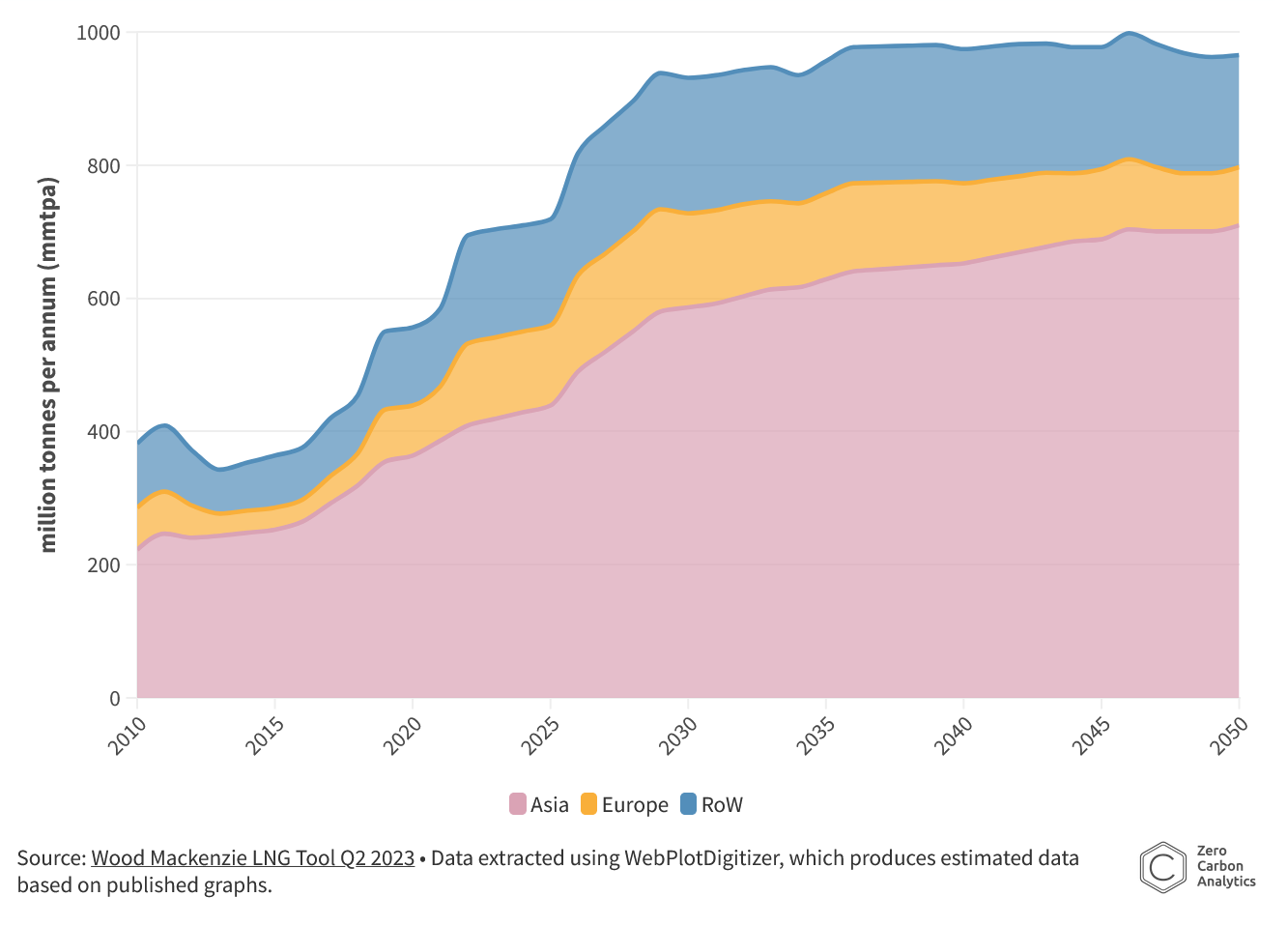

Zero Carbon Analytics notes that Asia, projected to account for as much as 75% of the global LNG market dominance by 2050, is now facing a potential demand deficit due to renewables’ cost competitiveness. As Energy Tracker Asia has reported, Japanese utilities are already bracing themselves for a potential oversupply by 2030 due to steadily declining domestic LNG demand.

In fact, Japan, the world’s second-leading LNG importer for 2023, already saw a peak in gas demand during the last decade. The same is true for South Korea, which remains the third-largest importer. As a result, the two countries are facing oversupply and plan to offload LNG to emerging Asian markets to compensate for some of the losses.

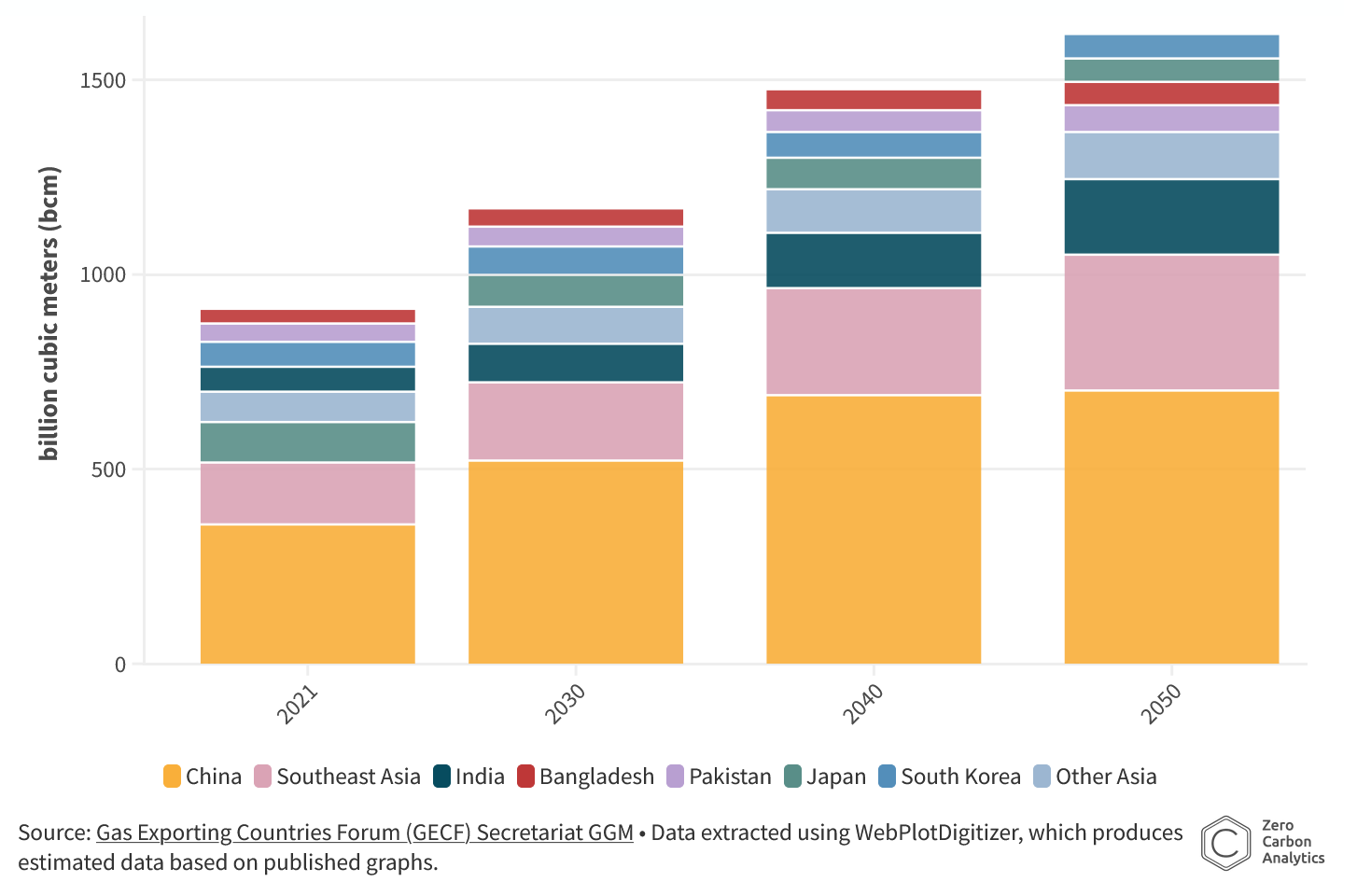

The research group also sees a shift in gas demand from mature to emerging Asian economies by 2040. This is motivated mainly by the power sector in emerging Asian countries and the transition from coal to gas.

According to Zero Carbon Analytics, China and India will continue to be the main engines behind Asia’s gas demand until 2050. However, cheaper renewables and energy security issues might further disrupt the gas market dynamics.

Reasons for Gas Demand Forecast Uncertainties

The energy crisis that shook Asian economies has eroded gas’ image as the reliable bridge fuel that every government needed to ensure a seamless energy transition. Energy security issues, paired with continuously decreasing clean energy costs and Asian governments’ decarbonisation goals, have also weakened the strong gas demand growth projections for the region. As a result, Asian policy-makers are now facing a crucial decision regarding their future energy systems

Cheaper Renewables

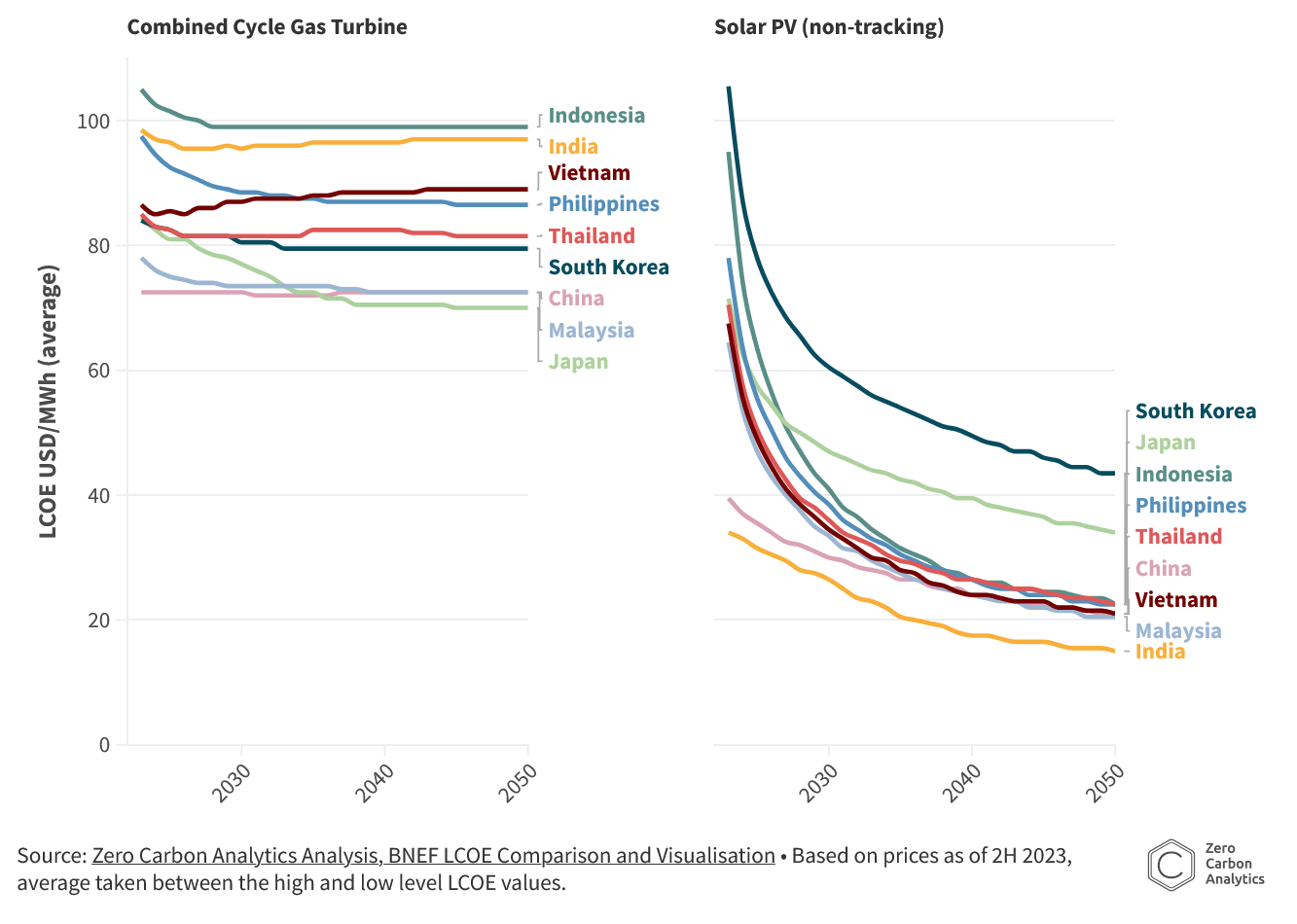

In 2023, 96% of newly installed, utility-scale solar PV and onshore wind had lower generation costs than new coal and gas plants. In the Asia Pacific, solar costs dropped 23%, making solar power the cheapest energy source in the region. Furthermore, the levelised cost of electricity (LCOE) of solar power is expected to plunge further in the years up to 2050. In comparison, gas prices are likely to remain at similar levels.

Due to renewables’ rapid drop in LCOE and stable gas prices on global markets, natural gas’ cost competitiveness is expected to erode further. This provides a significant incentive for emerging economies to consider accelerating solar and wind power deployment.

Zero Carbon Analytics notes that China and India already benefit from lower solar costs compared to combined cycle gas turbines. For example, China’s lowest LCOE for solar PV over the second half of 2023 was less than half the price of gas. In India, the difference was more than three times.

Gas Market Volatility and Energy Security Issues

The natural gas market’s unpredictability is making leading Asian LNG importers reconsider their long-term strategies in a bid to improve their energy security. According to Zero Carbon Analytics, price volatility remains an unpredictable factor for Asian gas demand forecasts, as LNG purchases at spot market prices are proving fiscally unsustainable for many emerging economies in the region.

Another factor that may tamper with the LNG demand is that new growth will mainly come from emerging Asia. Historically, these countries haven’t been major gas consumers. As a result, they lack the needed infrastructure to accommodate the demand. Overcoming this set of barriers is further complicated by the price volatility of natural gas. The price instability directly translates to financial challenges and viability risks for gas infrastructure projects across developing Asia. In fact, according to Global Energy Monitor, new Asian gas projects face USD 379 billion in stranded asset risk. On top of this, some markets are experiencing regulatory hurdles and project delays.

Factors like these are making Asian governments more cautious about the long-term role of gas in their energy mix.

In China, for example, local experts advocate for a 40% cap on LNG imports. The goal is to retain the country’s energy self-dependence rate above 80%.

Even long-term LNG deals can’t always shelter price-sensitive economies from high import costs due to existing loopholes. For example, despite signing a contract during the 2022 energy crisis, Pakistan saw its LNG deliveries cancelled and redirected to wealthier buyers for three times the contractual amount. As a result, the country had to purchase LNG from the spot market at significantly higher prices. This drained Pakistan’s foreign currency cash reserves and brought it close to default. The country faced an increase in poverty, with many businesses closing down.

Asia’s Clean Energy Transition is Accelerating

As of 2022, Asia accounts for 52.5% of global wind and solar capacity. In 2023, Asia accounted for 69.3% of the new renewable energy capacity. The past year has seen unrivalled clean energy deployment, and 2024 is on course to set another record.

The IEA’s 2024 World Energy Investment report finds that global clean energy investment will be almost double that of fossil fuels. Total energy investments worldwide will top USD 3 trillion for the first time. Of these, USD 2 trillion will go towards renewables, EVs, grids, storage, low-emissions fuels, efficiency improvements and heat pumps. The remainder will go to coal, gas and oil.

China will again lead the charge with an estimated USD 680 billion in clean energy investments. Between 2000 and 2022, the country doubled its wind and solar capacity every 1.5 years and 2.5 years, respectively. In 2023, China reached a new milestone, having 85% of its new capacity originating from renewables. Renewables already represent the country’s largest year-on-year increase in consumption by source. At the start of June, China launched the world’s biggest solar farm. The 3.5 GW farm will generate 6.09 billion kWh of electricity per year, equal to Papua New Guinea’s annual consumption. According to forecasts, China will increase its solar and wind capacity to over 1,200 GW by 2030.

India will register the fourth biggest clean energy investments this year. Sales of EVs have increased by 3,000% from 2015. Between 2016 and 2022, the country increased its solar and wind capacity fivefold. Between 2023 and 2028, India will double its 2022 cumulative installed capacity, adding 205 GW. The IEA notes that if India addresses existing administrative or technological challenges, it will be able to install almost 45% more renewable capacity.

Japan and South Korea, long considered clean energy laggards, will also see their gas demand drop notably. Instead, the countries will expand their renewable and nuclear power capacities.

Even Indonesia, the leading gas producer in Southeast Asia over the past two decades, will likely experience a gradual fall in gas demand as renewables deployment accelerates. The share of gas in Vietnam’s power generation mix is also declining, while renewables are doubling. The JETPs of the two countries can further accelerate the switch to clean power while limiting the role of gas.

Redefining the Role of Gas in the Energy Mix of Asian Economies

The IEEFA notes that the long-term investment case for LNG is fading, and industry signals also point in that direction.

The world is on a quest to triple renewable energy capacity by 2030, and Asia is in the driving seat. Considering that every dollar spent on decarbonisation will generate three to eight times the returns from avoiding climate change’s externality costs, Asian countries that opt to continue pouring funds into LNG and lock themselves into long-term energy insecurity will undermine their own economic, geopolitical and societal well-being.

by Viktor Tachev

Viktor has years of experience in financial markets and energy finance, working as a marketing consultant and content creator for leading institutions, NGOs, and tech startups. He is a regular contributor to knowledge hubs and magazines, tackling the latest trends in sustainability and green energy.

Read moreOur Publications