ASEAN Energy Transition: The Role of LNG

14 May 2024 – by Viktor Tachev

Most Asian countries, especially ASEAN economies, plan for LNG to be integral to their energy policies and transition pathways. However, over the past four years, LNG has proven unreliable, exposing countries to recurring energy shortages, power blackouts and economic hurdles. While gas still has a role in a net-zero scenario by 2050, the financial, geopolitical and environmental arguments mandate that it should be limited only to supporting renewables as the backbone of Asia’s energy system.

Asia To Lead Global Gas and LNG Infrastructure Expansion Plans

According to Shell, the industrial demand in China and the flourishing economies in South and Southeast Asia will cause an estimated 50% rise in global LNG demand by 2040. The oil giant notes that this would necessitate significant investments in LNG import infrastructure.

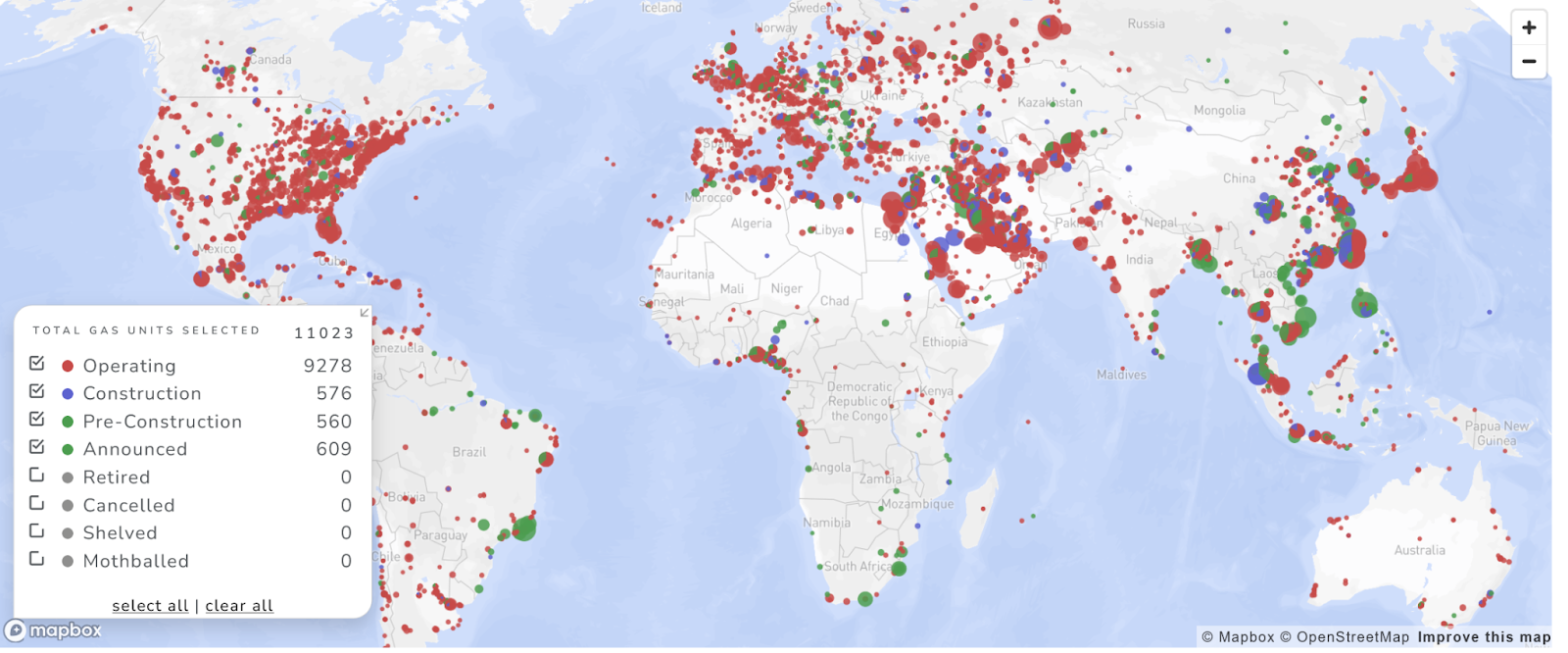

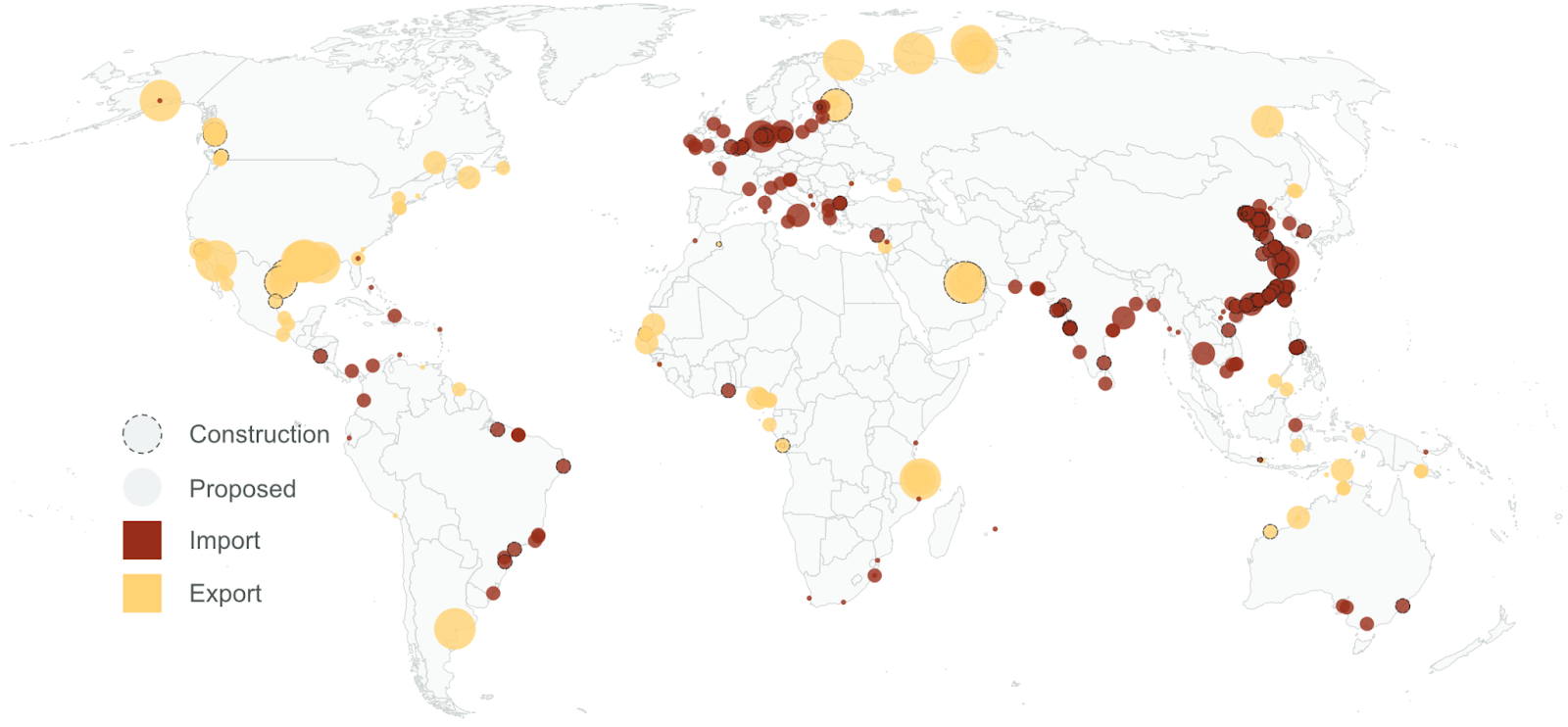

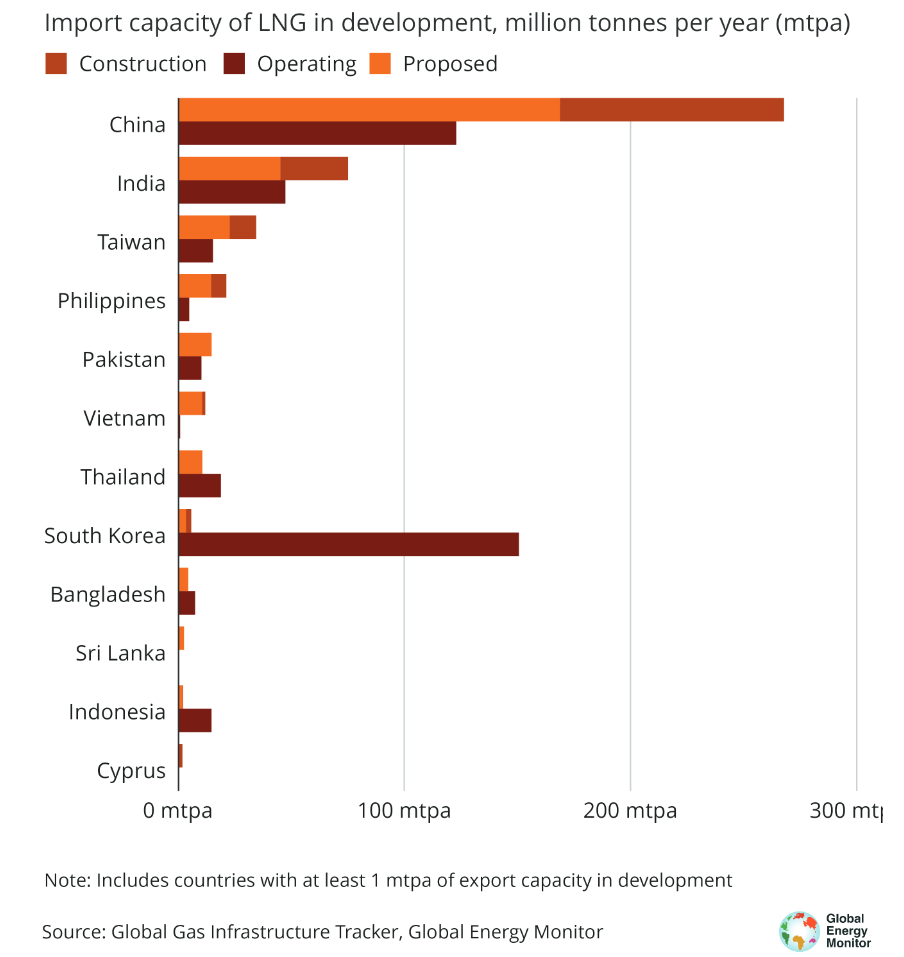

According to Global Energy Monitor, Asia demonstrates many ambitious gas and LNG infrastructure expansion plans. Asian countries have the most significant pipeline of announced gas units and projects in the construction and pre-construction phases.

According to the Global Oil and Gas Tracker (GOGET) report, at least 19 new gas fields in Southeast Asia will receive final investment decisions between 2022 and 2025.

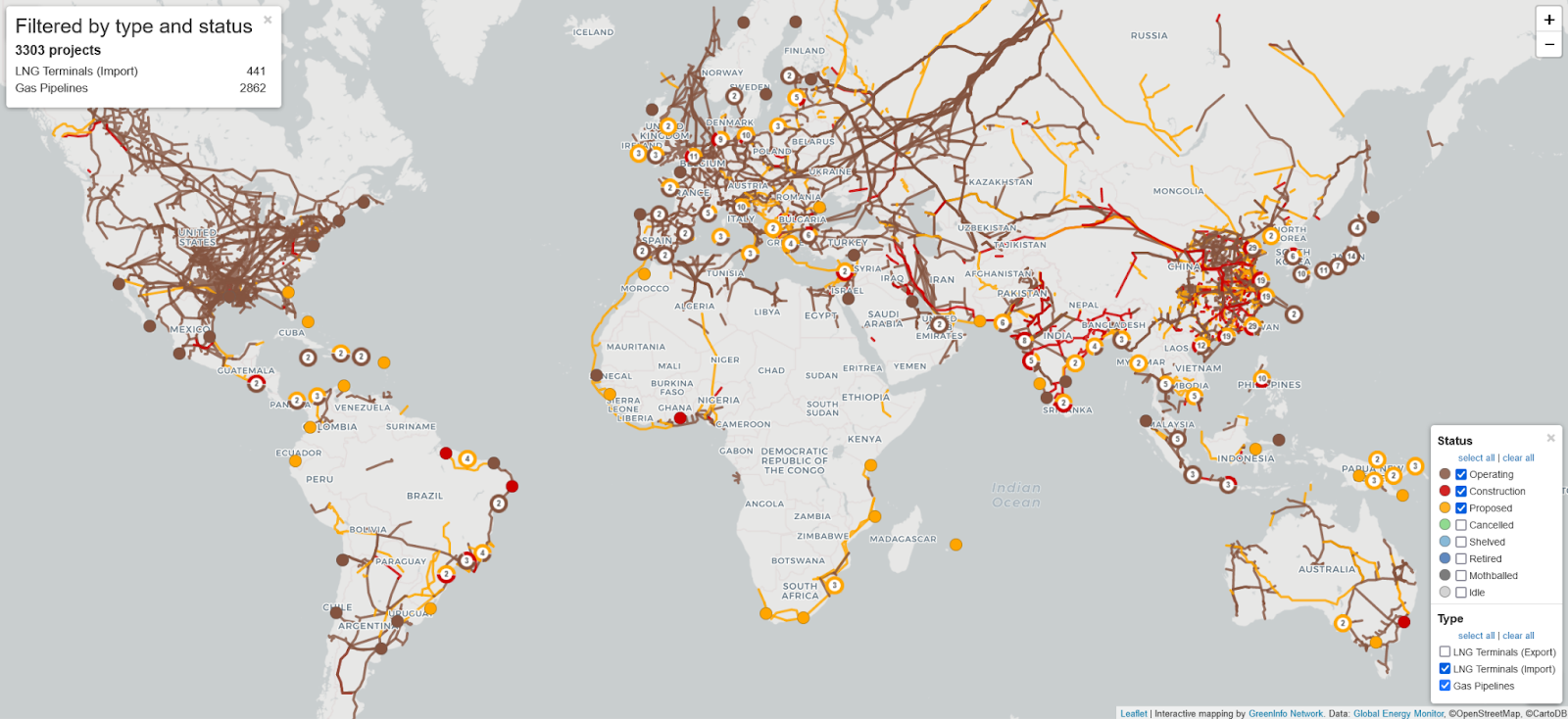

The case is similar when it comes to LNG infrastructure. Asia accounts for a major part of the globally announced pipeline, LNG import terminal projects and those in the construction and pre-construction phases.

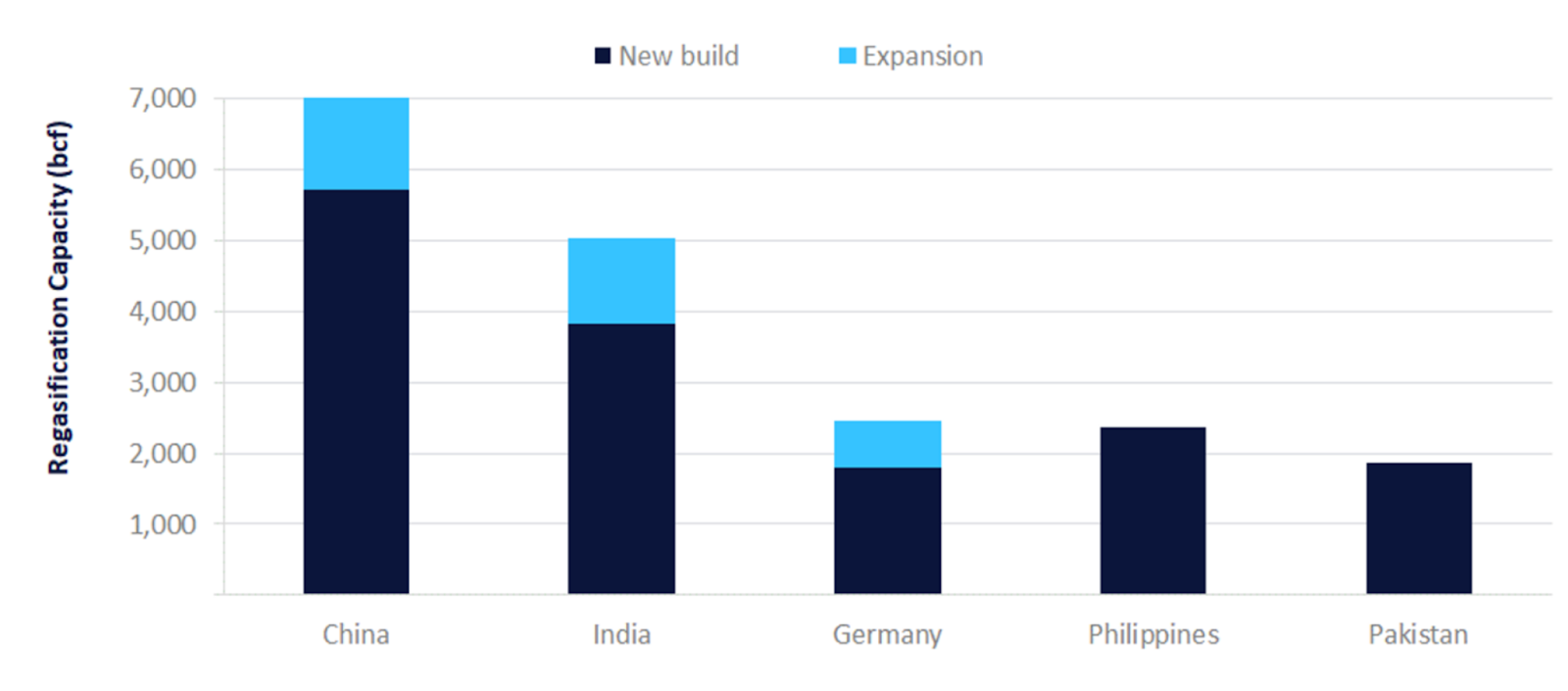

Analysts estimate that Asia will contribute around 70% of the expected total new build and expansion regasification capacity additions by 2027.

Oil and gas industry insiders and LNG exporters consider Asia the primary market for demand growth. They project the region to account for over 75% of the global LNG market by 2050.

The broad sentiment shared throughout the AtoZero Asia 2024 Conference was that LNG will continue playing a role in Asia’s energy mix come 2050 as the region moves away from coal. However, experts were clear that the path won’t be as straightforward as expected, with uncertainty to remain an integral part of the gas market.

Gas and LNG Uncertainty: The Financial and Energy Security Risks For Asia

Global Energy Monitor notes that future LNG demand in Asia is “highly uncertain”. According to the International Gas Union, there is a real risk that future LNG demand in Asia will decline, given the region’s price sensitivity. The IEEFA warns that long-term LNG contracts with deliveries starting before 2026 are reportedly sold out globally, forcing Southeast Asian countries to purchase from expensive spot markets.

On account of Shell’s projections that gas demand will continue increasing in the years up to 2040 due to China’s and Southeast Asia’s booming industrialisation, the IEEFA notes that the oil giant is overlooking China’s policies for limiting gas dependence. Furthermore, the analysts warn of LNG’s high costs and the critical barriers to value chain financing that are likely to constrain demand growth in the South and Southeast Asian markets.

The uncertainty is also fuelled by the upcoming elections and policy reviews that will take place across various Asian countries in 2024. Such events usually have long-lasting impacts on gas markets.

“Taking into account the ongoing strains and volatility in traditional energy markets today, claims that oil and gas represent safe or secure choices for the world’s energy and climate future look weaker than ever,” notes IEA Executive Director Fatih Birol.

These warnings are particularly valid for Asia, where the projected demand growth potentially poses various challenges.

Increased LNG Import Dependence

Global Energy Monitor’s map demonstrates that the region dominates the new LNG import capacity, accounting for two-thirds of all capacity in development globally.

The increased reliance on LNG imports has, in the past, caused economic catastrophe for several developing Asian countries. Nations that struggled to afford LNG cargoes experienced blackouts, economic growth slowdowns and alleviated energy poverty. For example, the blackouts in Bangladesh will likely last until at least 2026.

As Carbon Tracker warns, in addition to the economic drawbacks, gas import dependence can also expose nations to geopolitical risk.

Underutilisation Risk

The increased build-up of LNG import infrastructure bears a significant underutilisation risk.

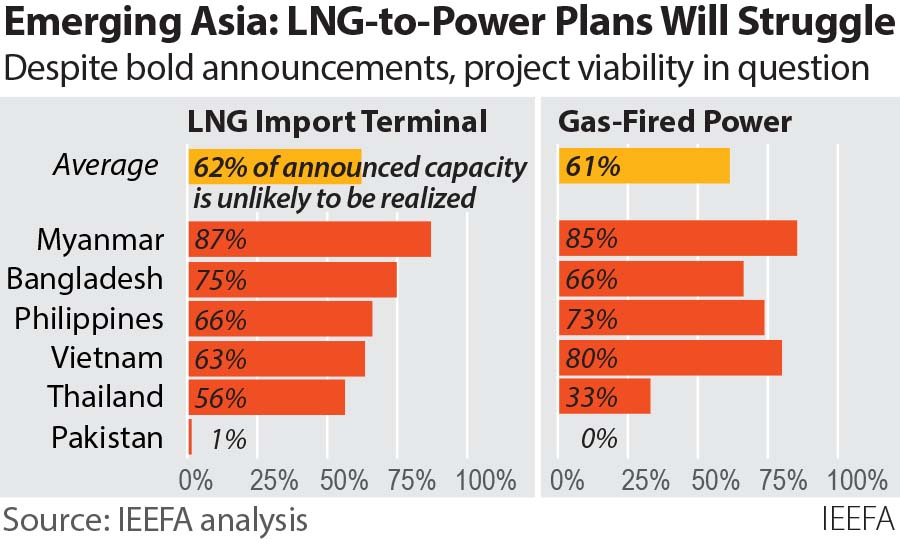

One particular case is Japan, where demand is decreasing and local utilities will face a continued surplus problem throughout 2030. In the case of long-term contract lock-ups, such as with different projects in the Philippines, LNG imports can become an increasingly risky strategy. The first LNG terminal commissioned in the Philippines, for example, is already facing a risk of underutilisation due to high costs.

According to Wood Mackenzie, Asia’s regasification capacity plans could create the “highest level of underutilisation in 10 years on average”.

Shaky Economics Risk Causing LNG Project Delays and Cancellations

During the first day of the AtoZero Asia 2024 Conference a discussion panel was dedicated to the role of LNG in Asia’s transition. Industry insiders noted that the high LNG prices emerging economies had to bear significantly influenced the transition. Furthermore, the high costs have impacted investors’ decision-making and made them acknowledge the energy security and affordability issues related to gas investments.

In the past, the price volatility and unreliability embedded in the DNA of global LNG markets have proven that they are unable to compete with alternative power sources and stressed the lack of economic reasoning to invest in such projects.

Countries like Pakistan and Bangladesh were priced out of the gas markets and left starving for power. Bangladesh also faces USD 5 billion in outstanding energy payments due to high imported fuel costs.

The IEEFA notes that the price laid out in India’s recent renewal of its LNG contract with Qatar would need to fall by half to compete with coal imports and even further to compete with cheaper, domestically produced resources.

Many developing Asian countries, such as Vietnam and the Philippines, remain fully exposed to spot market volatility due to a lack of long-term contracts.

The unpredictability of global gas markets has made some Asian countries reassess their priorities. Pakistan plans to phase out imported LNG and prioritise domestic power generation, including solar and wind.

In Thailand, where high fuel costs and subsidies in 2022 threw the state-owned utility into a liquidity crisis, the government has decided to ramp up domestic gas production and accelerate its shift to cheaper clean energy, doubling its capacity by 2030.

As a result of shaky economics and rising costs, around 81 GW of planned gas capacity was cancelled in Asia between 2022 and 2023. The IEEFA sees a growing risk of planned LNG and gas infrastructure across Asia not being built due to a lack of feasibility.

Shaky economics and demand uncertainties aside, some projects have also faced mounting scrutiny and increased risk of delays or cancellation due to their negative impact on the environment and communities.

Long Project Completion Times

For the bullish LNG forecasts to materialise, Asia will need a mass build-up of import and end-use facilities. And this isn’t always a straightforward process.

The IEEFA says that LNG-to-power projects require “a notoriously long time to negotiate and develop”. LNG projects, including the necessary infrastructure and pipelines, can take as long as three years to build. Depending on regulatory and geopolitical factors, that process can extend to five or more years. Meanwhile, gas-to-power plants can take up to six years to build.

A case in point is Vietnam, which completed its first LNG terminal in 2023. The country might have to wait until 2027 for its first LNG-fired power plant to finalise its offtake contract.

Carbon Tracker says new gas plant developers will have minimal time to build and start operating their units before their assets become unable to compete with renewables.

According to Global Energy Monitor, new Asian gas projects face USD 379 billion in stranded asset risk.

Gas and LNG Should Make Way For Clean Technologies

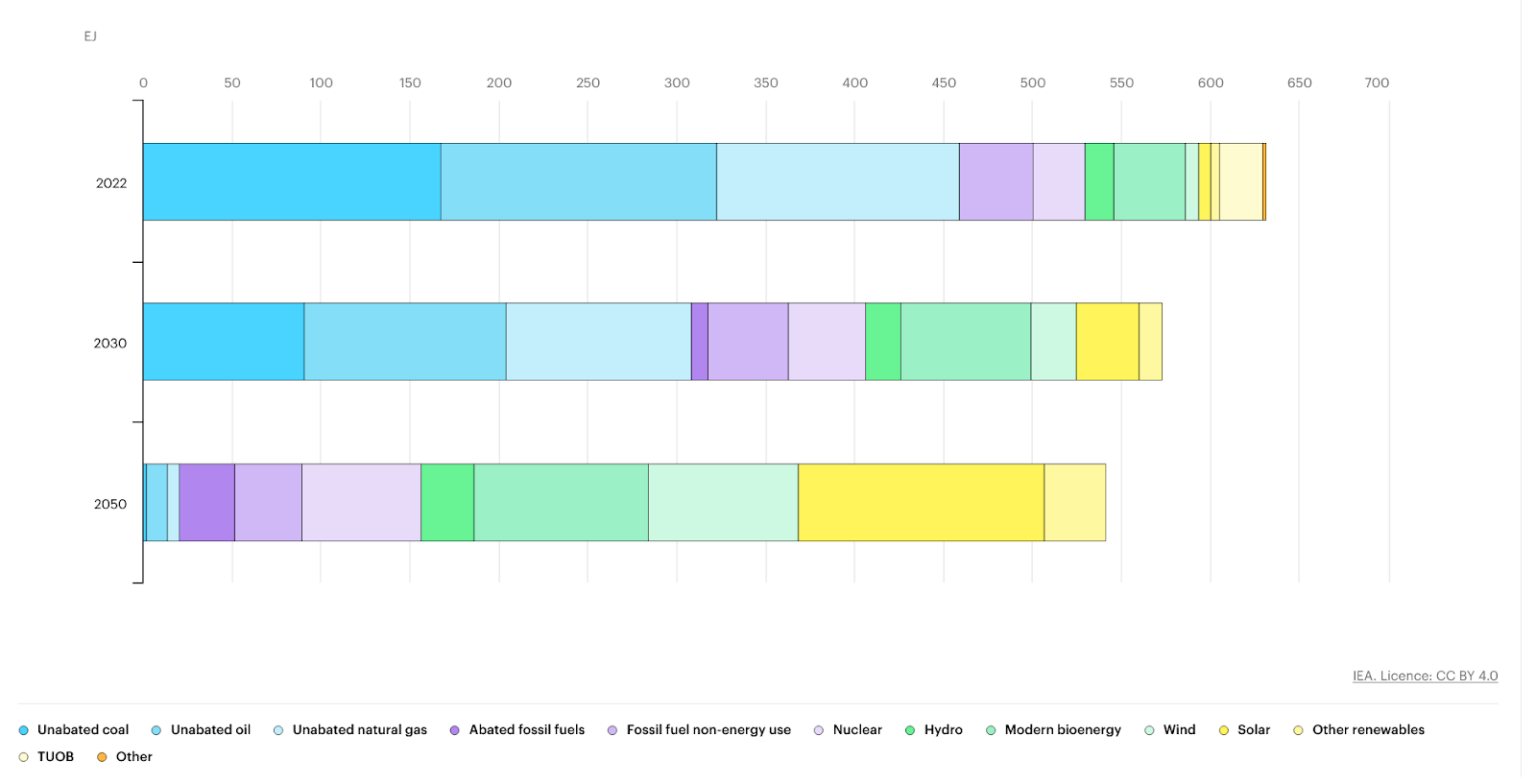

According to the IEA, come 2050, in a 1.5°C-aligned scenario, gas should play a negligible role in the global energy mix.

The IEEFA says the long-term investment case for LNG is fading. Industry signals also support that observation. Shell, which owns the largest LNG portfolio in the world with assets and contracts extending beyond 2050, reduced its global LNG demand expectations for 2040 by up to 11% compared to previous forecasts. More significantly, it predicted that demand would peak sometime in the 2040s, while acknowledging that the peak has already been reached in mature Asian LNG markets like Japan and South Korea in the last decade. The IEA sees gas demand to peak even earlier: by the end of this decade based on today’s policy settings. It says clean energy deployment is now “unstoppable”.

In its World Energy Outlook 2023 report, the agency suggests a significant reduction in fossil fuel use and a 75% reduction in methane emissions from fossil fuel operations. The most effective way for this is reducing gas demand. In addition, to get the world back on track, the IEA advises tripling global clean energy capacity, doubling the energy efficiency improvement rates and tripling clean energy investments in emerging and developing countries.

Considering that every dollar invested in the clean energy transition generates three to eight times the return, Asian countries that opt to continue pouring funds into LNG infrastructure and lock themselves in long-term energy insecurity are undermining their own economic, geopolitical and environmental well-being.

by Viktor Tachev

Viktor has years of experience in financial markets and energy finance, working as a marketing consultant and content creator for leading institutions, NGOs, and tech startups. He is a regular contributor to knowledge hubs and magazines, tackling the latest trends in sustainability and green energy.

Read moreOur Publications