Investors Pulling Out of the Barossa Gas Project Adds to the Uncertainty

19 August 2024 – by Viktor Tachev

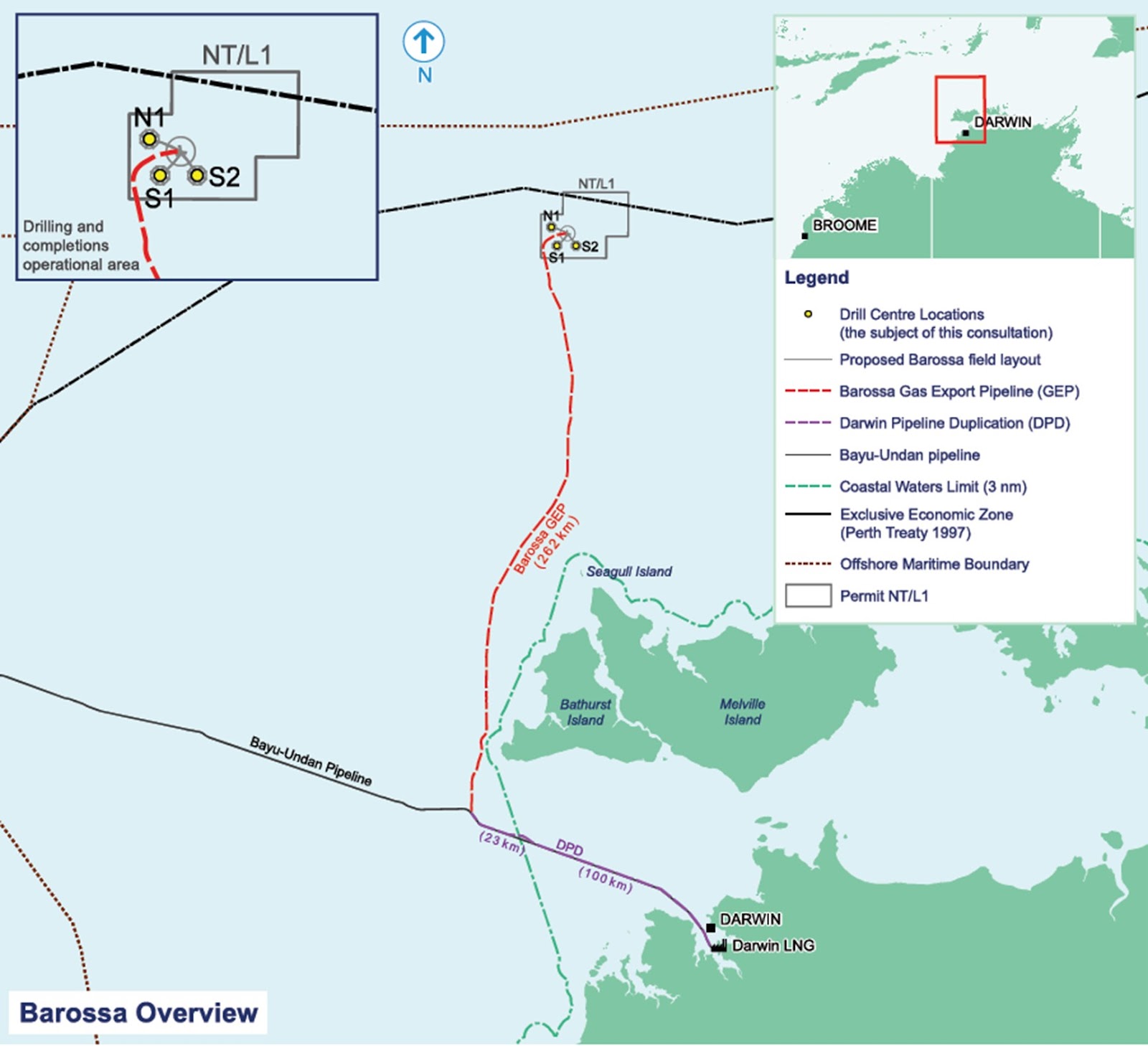

The Barossa Gas Project is an offshore gas and condensate project. It aims to extract natural gas from the Barossa gas field in the Commonwealth waters near Australia, 300 km offshore from Darwin in the Northern Territory. The gas will be transported via gas export pipeline to the Darwin LNG facility. The project’s annual production capacity is 3.7 million tonnes (Mt) of liquefied natural gas and 1.5 million barrels of gas. The first gas deliveries are expected in 2025.

Santos, a leading Australian gas and LNG supplier, holds the majority share in the Barossa gas project, with 50%. Other partners include the Korean SK E&S with 37.5% and Japan’s JERA with 12.5%.

Approved by National Offshore Petroleum Safety and Environmental Management Authority

Australia’s independent expert regulator for offshore oil and gas development, the National Offshore Petroleum Safety and Environmental Management Authority approved the Barossa Offshore Project Proposal in March 2018. In 2021, Santos made a final investment decision for USD 3.6 billion. Nine international banks provided USD 1.15 billion in debt financing for the project. Additional financial support came from the Export-Import Bank of Korea (KEXIM) and K-Sure (Korea Trade Insurance).

According to Santos, as of July 2024, the project was 77% complete and on target to launch in Q3, 2025.

Santos had previously described the project as important for enhancing Australia’s relationships with investors and gas customers in Asia.

Leading Barossa Gas Project Investors Are Pulling Out

“Santos and its partners in the Barossa development should take their losses as they are before they grow greater still,” warned John Robert in an analysis published by the Institute for Energy Economics and Financial Analysis (IEEFA) in February 2022.

Fast forward two years, and investors seem to be acting upon Robert’s advice.

According to reports, K-Sure, the South Korean government’s export credit agency, withdrew the insurance underwriting SK E&S’ investment in the project in January. Solutions for Our Climate, a Korean environmental group, described the rare withdrawal of the insurance agreement as a loss of confidence in the developer’s ability to meet the deadline and get the project back on track after one of the multiple delays.

BNP Paribas has pulled from its role as a financial adviser to SK E&S. KEXIM has also confirmed that it hasn’t renewed its loans to SK E&S for the Barossa project.

Campaigners from Market Forces, an Australian think tank, urged Australian banks to follow BNP Paribas’ and KEXIM’s steps and cut ties with Santos.

The financial support of the parties pulling out of the project to SK, which has a 37.5% stake in the project, is USD 700 million. Aside from the direct financial implications, the move can also have indirect consequences by further exacerbating the uncertainty and eroding the trust of other investors in the project. According to the Financial Times, the moves mean financing could now become an issue for the project.

Experts Warn Prospective Barossa Gas Project Investors of Major Risks

Santos estimates that the Barossa gas project will cost USD 4.3 billion to build. Considering the number of investors backing out of the project, financing will have to be sought elsewhere. Japanese financiers are a likely source, with JERA already a part of the project.

However, recent developments, the gas market outlook and banks’ decarbonisation goals would make new investors wary of committing. For example, 24 of 100 leading global financing institutions already have exclusions on financing new oil and gas projects.

According to Market Forces, many of these exclusions have been adopted in the past two years, and the trend is likely to accelerate as banks strengthen their net-zero commitments. Project financing exclusions aside, many banks now require credible transition plans from oil and gas companies to provide funding, which is something that Santos lacks, according to the think tank.

Gloomy Natural Gas Market Outlook

According to reports, the Australian government has identified LNG as a critical part of the national energy strategy beyond 2050. However, the IEEFA doesn’t see as bright of a future for Australian LNG, as the bullish strategy projects. The analysts say that between 2025 and 2028, LNG supply will increase by 40%. This will create a glut of new, low-cost LNG that will intensify competition. The IEA also reaches similar conclusions, noting that from 2025, the world will see an unprecedented surge in new LNG projects, with over 250 billion cubic metres of new capacity per year to come online by 2030 – almost half of the total global LNG supply today.

At the same time, the demand is projected to drop. According to the IEA, peak gas demand this decade is already set in the current global policy settings and market dynamics. For Asia, in particular, existing national climate pledges indicate a 40% drop in the region’s gas consumption by 2050.

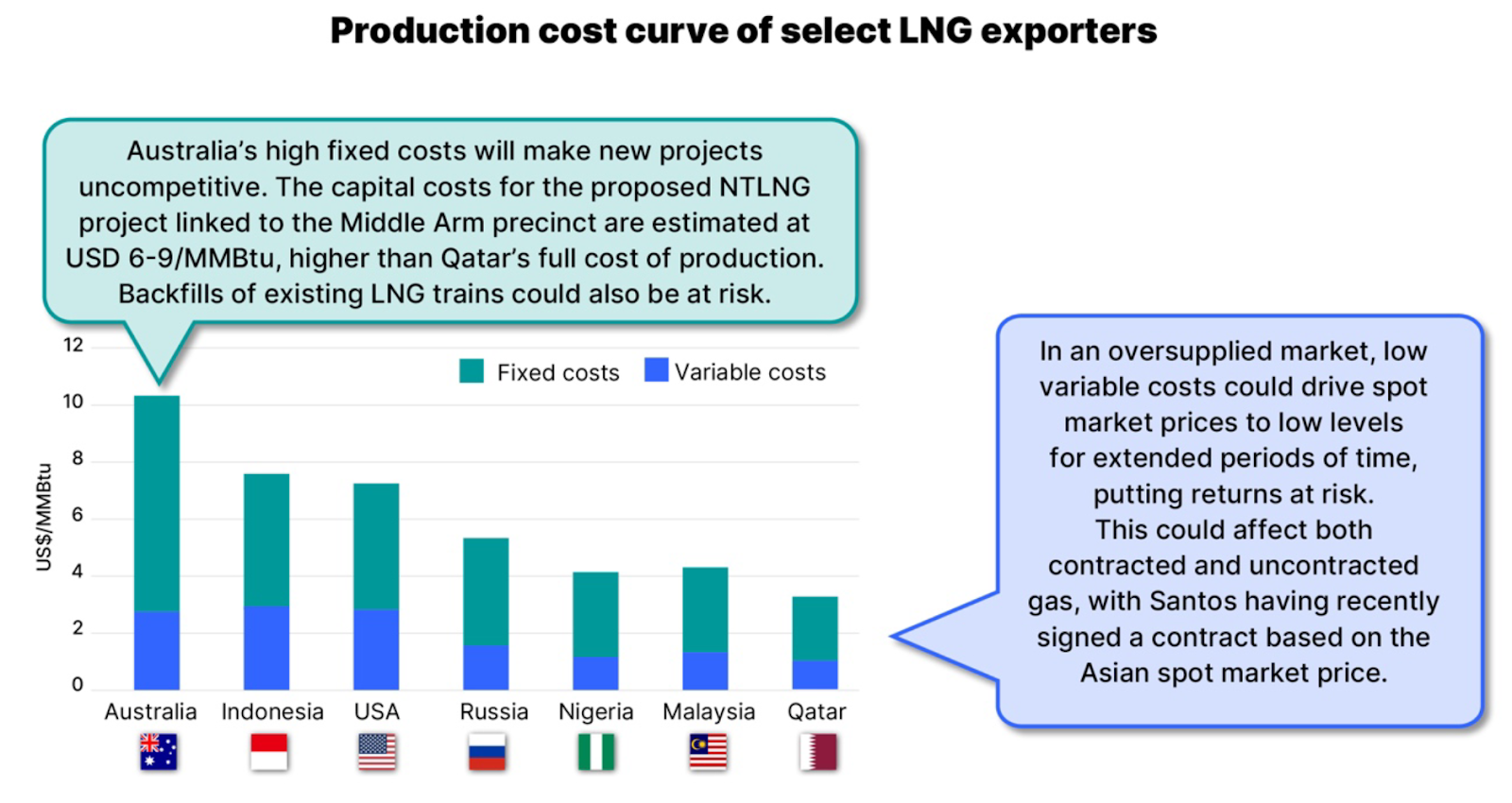

As a result of these factors, the IEEFA has questioned the commercial viability of Australian gas producers and their ability to compete successfully against lower-cost producing countries, such as Qatar.

Most of the gas produced by Santos and competitors like Woodside is made in Australia and exported. According to some projections, LNG demand in South Korea and Japan, the two key export markets of Santos over the past decade and a prime target for the Barossa gas project, has already peaked. In fact, as Energy Tracker Asia has reported, Japanese utilities expect a potential oversupply by 2030 due to steadily declining domestic LNG demand. South Korea is scrapping LNG import infrastructure projects due to high costs, lack of economic reasoning and weakening demand. Both countries even plan to offload excess LNG to emerging Asian markets, meaning they can even turn from prospective customers to competitors.

Increased Costs and Project Viability

Australia’s record of high capital costs and poor shareholder returns for existing LNG plants are another factor to consider. According to the IEEFA, this makes it unlikely for Australia to see any new LNG projects reach a final investment decision. Even the government’s Future Gas Strategy report states that established production would be more competitive than prospective new sites in the current market, which puts additional strain on new projects, such as Barossa.

According to the IEEFA, project delays and CO2 emission offset requirements have notably escalated the initial cost of USD 5.5/MMBtu of the Barossa project. As a result, they are much higher than peer projects. In Qatar, for example, the LNG marginal cost is around USD 2/MMBtu, with a long-term marginal cost of USD 4/MMBtu).

Joshua Runciman, the IEEFA’s lead analyst for Australian gas, says that the Barossa project could face poor financial returns. In addition, he adds that Santos would likely face additional costs for offsetting the very high CO2 content in the Barossa field.

Market Forces expects the Barossa project may face a highly challenging operating environment.

In addition to the shaky economics, experts consider the uncertain project timeline as another critical risk factor for investors in the Barossa project. The multiple delays over the past couple of years have prompted Kevin Morrison, an energy finance analyst at IEEFA, to describe Barrossa’s timeline as “increasingly unrealistic“.

Environmental Concerns

Experts and business leaders have expressed concerns about the pollution, describing the project as “a carbon-dioxide emissions factory, with an LNG by-product” and “one of the most polluting projects in the world”. The Australian Conservation Foundation notes that, over its 25-year lifespan, the project would emit 401 million tonnes of GHG emissions, which is close to Australia’s total annual emissions. The IEEFA considers Barossa the most carbon-intensive gas project in Australia, with CO2 emissions twice the Australian LNG industry’s average. According to the Australian Institute, Barossa will produce three times more CO2 than peer gas projects.

These findings contradict the new climate legislation introduced by the Australian government, requiring Australia’s fossil fuel facilities to reduce their emissions in line with the national emission reduction targets of 43% below 2005 levels by 2030 and net zero by 2050.

While the project will be accompanied by the Bayu-Undan carbon capture and storage plant, with a final investment decision in 2025, the IEEFA finds that Barossa’s emissions profile won’t change with or without it. And according to market analysts, gas buyers are increasingly looking to turn towards less carbon-heavy gas.

To address the environmental risks and other concerns and how it plans to address them, Santos has published a detailed guide and a FAQ document. However, these have proven insufficient to satisfy ecoactivists and Tiwi Islanders.

The Tiwi Islands in Australia have been a sanctuary for Indigenous peoples. They possess diverse marine ecosystems, and their coastal areas are internationally significant nesting sites for aquatic turtles.

In September 2022, a judge ruled that the Indigenous population of the Tiwi Islands in the Timor Sea, where the 262-km Barossa gas pipeline would pass through, hadn’t been properly consulted about the Barossa gas project. The landmark win granted Santos two weeks to remove its equipment from the islands and suspend drilling. The infrastructure sat idle for over a year until the company received approval for a revised drilling plan in December 2023.

Indigenous communities expressed concerns that the Barossa project risked disturbing their “Sea Country” ecosystem, including the turtle population. They were also reportedly afraid of another Juukan Gorge disaster – a 2020 case when Rio Tinto blew up a 46,000-year-old heritage site while expanding an iron ore mine.

Locals’ concerns have grounds, considering Santos is no stranger to environmental controversies. Last year, a former employee criticised the company for its reaction to an oil spill that killed marine wildlife, claiming that it had lied about the severity of the problem. In 2021, the Australasian Centre for Corporate Responsibility filed a lawsuit against Santos and its statements about gas being “clean” and having a clear pathway to net zero by 2040.

More recently, Santos has also faced another legal battle over claims by Indigenous Tiwi islanders that the Barossa gas project would disturb Ampitji, a rainbow serpent, and Jirakupai, the Crocodile Man – two beings that they consider sacred. The court dismissed the claims.

Despite this, the case highlighted the increasing uncertainty surrounding gas projects, ultimately leading to delays and increased costs for project developers. Due to environmental opposition, the Barossa project faced several delays in pipelaying and drilling development. In the most recent case, Santos reportedly had to pay close to USD 20 million per month to keep a pipe-laying vessel on standby. The Australasian Centre for Corporate Responsibility estimates that all the regulatory delays could have cost the Barossa project USD 800 million. According to the IEEFA, the Barossa project is the largest in Santos’ portfolio, with a 13% share, and any timing changes are material to the company and its investors.

Reputational Risks For Investors

Santos aside, investors in the Barossa project have also been subject to increased public pressure. Ecoactivists and Indigenous leaders from the Tiwi Islands visited South Korea and Japan and urged local institutions to stop financing the project. First Nations groups lodged a human rights complaint against Australia’s top 20 superannuation funds over their financial support for the Barossa project, urging them to cut ties with Santos.

In fact, the Export-Import Bank of Korea has previously threatened to withdraw USD 330 million of its funding for the Barossa project if no emissions reduction efforts are made.

Financial Risks From Legal Action

According to research by the University of Melbourne and Oxford University, polluting companies could be liable for trillions in damages from 2,500 climate lawsuits globally. The academics warn that financial assessments fail to adequately account for these risks. As a result, project investors were “flying blind” over climate lawsuit risks, potentially overlooking significant financial exposures.

“That means investors end up investing in the wrong projects and run risks that neither they nor regulators understand, thereby further aggravating the financial risks climate change entails,” explains Associate Professor Thom Wetzer, lead author and director of the Oxford Sustainable Law Program.

The study also stresses the scale of these lawsuits and their potential industry-wide implications. According to the researchers, the oil and gas giant Chevron alone could be liable for up to USD 8.5 trillion. For reference, its profits between 1990 and 2019 were USD 291 billion.

According to the study’s authors, climate litigation isn’t the only direct threat that companies face. Businesses can also be impacted by increasing borrowing costs or policy changes, such as subsidy reductions, emission reductions or enhanced disclosure requirements, all of which can significantly increase project uncertainty and distort investors’ ability to adequately plan ahead.

Transition Risk

Another factor that investors have to consider is the risk of stranded asset infrastructure. The Barossa gas project will have a production life of approximately 25 years. However, the poor economics of new Australian LNG plants and the pessimistic global gas market outlook signal a real risk of LNG and gas infrastructure mothballing way before the end of its useful life. According to the IEEFA, this undermines the returns anticipated at the time of the initial financial investment decision. The analysts warn that the early retirement of infrastructure would also bring forward decommissioning obligations, with substantial costs.

According to Market Forces, Santos continues to reject investor demands for a genuine climate risk management strategy, and its targets remain weak, with emissions expected to rise 22% by 2028. The think tank notes that Santos’ approach has already cost shareholders significant underperformance while exacerbating massive transition risk exposure.

Barossa, as well as other gas projects in the country, oppose the IEA’s recommendation that countries stop building new gas infrastructure to achieve net zero.

What Next For the Barossa Gas Project?

Northern Territory’s mining minister, Nicole Manison, who last year visited Japan and South Korea to convince financiers about the energy transition investment opportunities in the country, praised Santos for the “huge amount of work that they have undertaken” regarding consultations with Tiwi locals about the heritage sites in the area of the Barossa project. She also warned that “20 years’ worth of jobs” would disappear if Santos walked away from the project due to legal challenges from environmental campaigners and traditional owners.

Madeleine King, Australia’s resources minister, recently assured Japan that her country was determined to remain “a trusted and reliable partner on gas,” citing Barossa as an LNG project Australia would bring “to fruition”.

However, with the wave of investors pulling out of the Barossa project, it seems the assurances from Australian politicians and the project developers aren’t convincing enough. As a result, the project now faces significant question marks regarding financing. Santos will have the challenging task of scaling up capital by convincing investors that there is a viable, long-term strategy behind the project. However, without a dramatic change in strategy, the company’s inadequate response to shareholder concerns, financial underperformance and misguided growth strategy, as described by Market Forces, isn’t likely to instil confidence in investors that pouring their capital into Barossa would be worth it – nor will the project’s history of environmental issues, legal action and the looming financial and reputational risks investors can expect.

by Viktor Tachev

Viktor has years of experience in financial markets and energy finance, working as a marketing consultant and content creator for leading institutions, NGOs, and tech startups. He is a regular contributor to knowledge hubs and magazines, tackling the latest trends in sustainability and green energy.

Read moreOur Publications