Gas Deals at COP27 Egypt: All You Need To Know

27 November 2022 – by Viktor Tachev

A massive fossil fuel lobby, a boom of gas deals and a reluctance to talk about the fossil fuel phaseout marked 2022 United Nations Climate Change Conference, COP27, in Sharm El Sheikh, Egypt. As a result, the decision on fossil fuels’ future was delayed for the next conferences. Considering that the UAE will host COP28 Dubai, the industry would likely live to fight another day, as many experts believe. Asian countries, however, shouldn’t wait for COP leaders set any new agendas. Many nations across the continent have already suffered from the drawbacks of fossil fuels and are embracing renewables at scale. The rest should follow.

A Disappointing Final COP27 Agreement

The COP27 agreement was a major success in terms of loss and damage financing. Regarding fossil fuels, however, it only succeeded in extending their life.

The summary reaffirmed that “limiting global warming to 1.5°C requires rapid, deep and sustained” emissions reductions. Yet, at the last minute, the final text was expanded to include that “low-emission” energy should be a part of the world’s future. Many analysts think the low-emission energy in question is gas.

According to Bloomberg, the situation has been long in the making. In the lead-up to the final days of COP27, oil and gas countries were preparing to push back against a potential final agreement calling for a fossil fuel phase-down.

The COP27 agreement also didn’t build upon last year’s emissions reduction pledges.

All this came after a group of 50 NGOs reported that over 96% of the oil and gas industry is planning a “frightening” expansion. It would result in 115 billion tonnes of CO2 in emissions, equivalent to more than 24 years of US emissions.

A Boom in Gas Deals at COP27 2022

COP27 (27th session of the Conference of the Parties) not only failed to seal the fossil fuel phaseout but also decided that oil and gas would continue playing a leading role in the energy transition. At the conference, described by some as a “fossil fuel industry trade show,” African leaders announced plans to exploit their existing oil and gas reserves actively. The EU endorsed these aspirations.

Leading oil-producing nations like the UAE and Saudi Arabia announced that they would continue pumping fossil fuels while investing billions in renewables.

The host, Egypt, endorsed fossil gas as “the perfect solution” to the energy crisis and encouraged deals.

In the run-up and during COP27, at least 14 gas announcements have been made.

The EU received its first gas delivery from Mozambique and became an immediate target of African activists. European companies were also very active, signing deals for gas operations abroad.

Japan, Thailand and Indonesia, alongside Japanese, Chinese and Indian companies, struck several oil and gas deals. These included deals for short-term and long-term imports and capacity development projects.

“The world is not facing an energy crisis – we are facing a fossil fuel crisis. The science is unequivocal: immediately ending expansion of fossil fuels and making a rapid, just transition to efficiency and renewables is our only hope of limiting warming to 1.5°C.”

Catherine Abreu, Director and Founder of Destination Zero

The Gas Expansion Risks

The number one risk of relying on natural gas is its damaging climate impact. That is why many experts were left stunned that governments used a climate conference to strike new gas deals.

“The continued expansion of oil and gas production is an existential threat to Pacific nations.”

Lavetanalagis Seru, Regional Policy Coordinator at Pacific Islands Climate Action Network

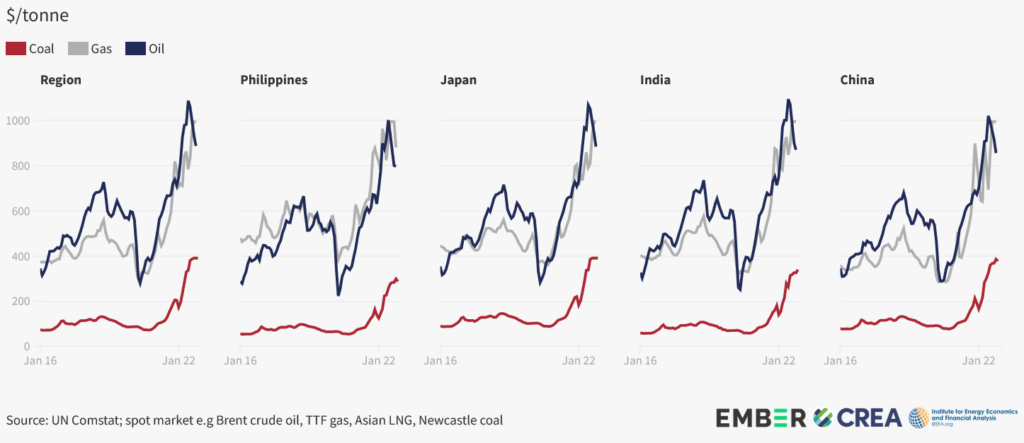

But, the financial impact of new fossil fuel deals is equally devastating. The continued reliance on natural gas by developing Asian economies bears massive financial risks. These have long-lasting consequences for all stakeholders, which include the need to bear with highly-volatile energy prices, up to USD 500 billion in stranded assets, energy dependency, project delays and cancellations and more.

For example, Japan already spent 1.1% of its GDP on gas in 2022.

Any new gas deals signed now and in the months ahead won’t bring gas prices down. They won’t address energy poverty or improve energy security. However, they risk exacerbating these issues, since the global LNG supply is expected to remain tight, at least until 2026. New gas capacity won’t come online earlier than 2026, either.

To overcome the energy crisis and the power blackouts tormenting Asian economies, countries need solutions now.

Renewables as the Viable Alternative to New Gas Purchases

Asian countries pursuing a renewable energy system will unlock many benefits. Among them are long-lasting energy security and independence, lower energy costs, emissions reduction, job creation and economic growth. Most importantly, as the IEA states, it gives the best way out of the energy crisis.

Continuously Decreasing Renewable Energy Technology and Electricity Costs

As we advance, renewables will provide around 95% of the new generation capacity. And the more renewable energy infrastructure is installed, the lower the costs will get.

Factors like Russia’s invasion of Ukraine and the energy crisis further accelerate clean energy infrastructure development and investments.

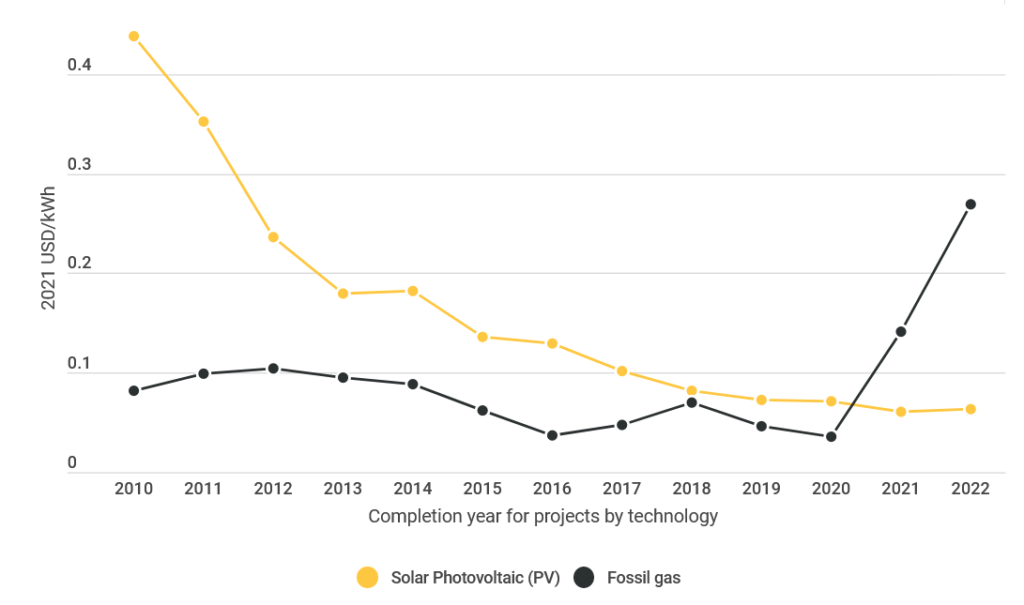

Globally, renewables are setting records for lower costs and new capacity development despite subsidy reductions. Even without subsidies and before the recent fossil fuel price hike, renewable energy sources have been cheaper than fossil fuels. Over the past decade, clean electricity costs have fallen by up to 90%.

Almost two-thirds of renewable power added during 2021 had lower costs than the cheapest coal-fired options in G20 countries. The power costs from new solar and onshore wind units are now around 40% lower than from new coal and gas-fired plants. And the gap continues to widen.

Renewables are the cheapest new power source for two-thirds of the world’s population and nine-tenths of electricity generation.

New solar and onshore wind power in Japan, South Korea and Vietnam, for example, are either already or will become cheaper overall investments than new gas infrastructure by 2025. New solar power with battery storage capacity in Japan and South Korea will be cost-competitive with existing gas plants during the early 2030s.

The clean energy capacity added during the past year will save around USD 55 billion in global energy generation costs in 2022. In the first half of 2022, solar generation helped China, India, Japan, South Korea, Vietnam, the Philippines and Thailand avoid potential fossil fuel costs of approximately USD 34 billion.

Job Creation

Today, there are more jobs in renewable energy than in fossil fuels. In 2022, renewable energy jobs hit 12.7 million globally, marking a jump of 700,000 new jobs in just a year.

According to studies, a transition to wind, water and solar energy would create 28.6 million more long-term jobs than we currently have.

The International Labour Organisation finds that green energy projects can offset job losses from a decline in extractive industries and create a net gain in employment. Furthermore, seven in 10 jobs in the oil and gas industry have partial overlaps with renewable energy.

Averted Losses

Transitioning to a renewables-led energy system will save developing nations massive energy costs. The funds can help support other crucial areas, including improving disaster preparedness for loss and damage and more.

Without the net-zero transition, the global economy could lose up to 18% of GDP (or USD 23 trillion) from climate change by 2050. The 20 most vulnerable countries have lost USD 525 billion over the past two decades due to the climate crisis.

Other studies estimate the loss and damage costs to developing countries from weather events between 1998 and 2017 to be around USD 593 billion. However, these figures are conservative estimates, as they measure only the immediate damage and don’t include long-term economic impacts. Furthermore, 66% of those losses are in South Asia.

Oxford scientists project that loss and damage costs could reach USD 580 billion annually by 2030 and trillions by 2050.

The Asian Countries Marching Towards a Renewable Energy System Despite the Gas Deals at COP27

The cost of the energy transition is often dubbed as too high. However, in a previous article, we examined that the cost is incomparable to the cost of inaction. According to Stanford academics, the investment needed to switch to 100% renewables would pay off within six years.

Many Asian countries realise that and step up their efforts. India and the Philippines are among the nations with the best progress in the Climate Change Performance Index. To lessen its exposure to gas, the Phillippines recently approved 42 new offshore wind power projects with a total capacity of 31 GW.

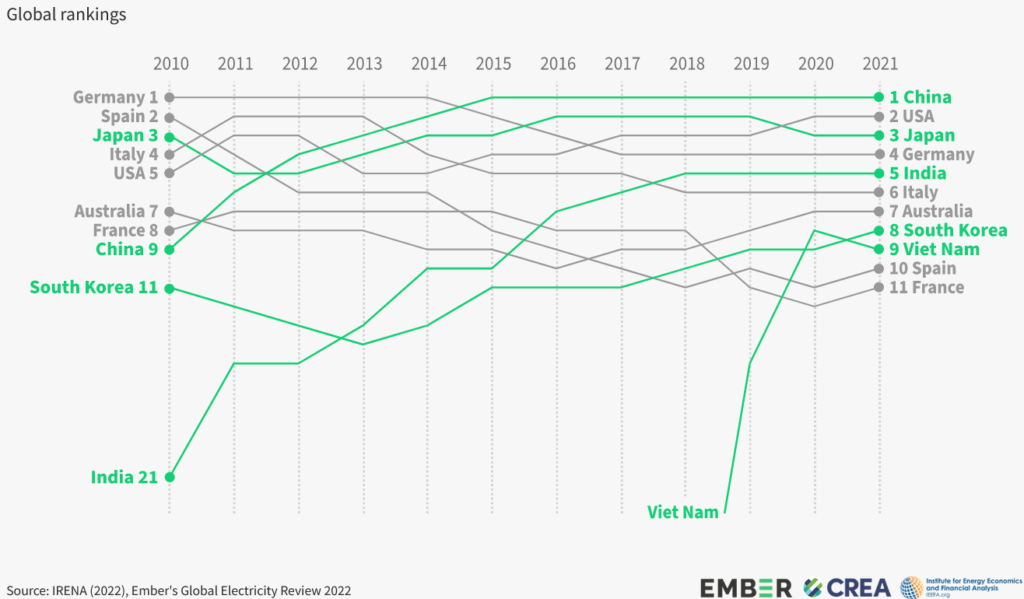

So far, there are five Asian countries in the top 10 for solar capacity globally in 2021.

China is increasing its solar high-efficiency cell production capacity almost every year, and projections show it will continue doing so up until 2024, at least. The country is also adding wind power capacity at unprecedented rates, dwarfing the results of all other markets. It is well positioned to reach its goal of installing a total of 1,200 GW of wind and solar by 2030.

Vietnam is also making strides. For just a year, in 2021, the country entered the top 10 markets with the biggest solar energy capacity after installing a massive 16.5 GW. The government has even more ambitious plans, including tapping into the estimated 311 GW of wind power potential.

Southeast Asian countries, as a whole, have one thing in common. They all have sufficient clean energy potential. However, the difference is that not all are capitalising on it. Once they start, the fossil fuel obsession will quickly vanish.

by Viktor Tachev

Viktor has years of experience in financial markets and energy finance, working as a marketing consultant and content creator for leading institutions, NGOs, and tech startups. He is a regular contributor to knowledge hubs and magazines, tackling the latest trends in sustainability and green energy.

Read more