2025 Renewable Energy Trends in the Asia Pacific Region

26 January 2025 – by Viktor Tachev

In 2025, the Asia-Pacific (APAC) region will once again set the renewable energy trends for the global energy transition. From increased solar PV and onshore wind deployment to advancing green technologies such as offshore wind power, floating solar, batteries, EVs and green hydrogen, Asia will again lead the global decarbonisation journey. The initial signs are that this won’t fly under the radar of energy transition investors, who will continue to look favourably toward the Asia Pacific as the preferred region for their investments.

The Top Renewable Energy Trends in Asia in 2025

In 2025, China is likely to surpass its target of having 1,200 GW of clean power by 2030, reaching 1,500 GW, while its CO2 emissions have already peaked or will do so in 2025. Projections reveal that between now and 2030, China will account for nearly 60% of all renewable energy capacity installed worldwide. By the decade’s end, the country will have over 50% of the world’s renewables. Alongside India, it will be the engine behind the accelerated deployment of renewables. Between now and 2030, clean energy is expected to roll out at three times the pace of the previous six years.

Furthermore, China’s share in all the manufacturing stages of solar panels today exceeds 80%. The country is also home to the world’s top 10 solar PV manufacturing equipment suppliers and has been instrumental in bringing down costs worldwide for solar PV. According to the IEA, the world will almost completely rely on China to supply key building blocks for solar panel production through 2025.

When it comes to wind, the Global Wind Energy Council finds that the onshore wind capacity in the APAC region could more than double to 1,084 GW by the decade’s end.

Not only will ground-mounted solar PV and onshore wind energy capacity be deployed faster than ever in Asia, but accompanying green technologies will make major leaps.

1. Offshore Wind

According to the Global Wind Energy Council, the Asia-Pacific region possesses some of the most attractive onshore and offshore wind resources globally and could play a pivotal role in the global energy transition. By 2030, over 122 GW of new capacity could come online, taking the cumulative regional total to 162 GW.

As with other green technologies, China will be by far the largest onshore and offshore wind market. By 2030, China will have around 130 GW of offshore wind. Japan and South Korea have already held offshore wind auctions, with the first awarded projects to come online from 2026, deploying 4 and 6 GW, respectively. Vietnam is working towards deploying 6 GW of offshore wind by 2030 and 70–91.5 GW by 2050. From 2024 to 2030, operational offshore wind capacity in APAC is set to increase sixfold.

Currently, APAC’s wind turbine supply dwarfs that of manufacturers from the rest of the world. Furthermore, most of the demand comes from within the region, positioning the local industry for significant growth in the upcoming years.

However, to maximise the region’s potential and meet the 2030 targeted wind installations, GWEC recommends that APAC governments prioritise scaling up regional supply chains. Crucial on that front would be increasing the public support for supply chain capacity building outside of auctions to boost resilience and ease the price pressure on developers. According to experts, international collaboration to scale up the floating wind supply chain would also be of great importance. South Korea’s Floating Wind project, which will consist of between 60 and 100 wind turbines, with power expected in 2028, and Doosan Enerbility’s Changwon plant are shining examples of global cooperation in the field.

2. Floating and Rooftop Solar Panels

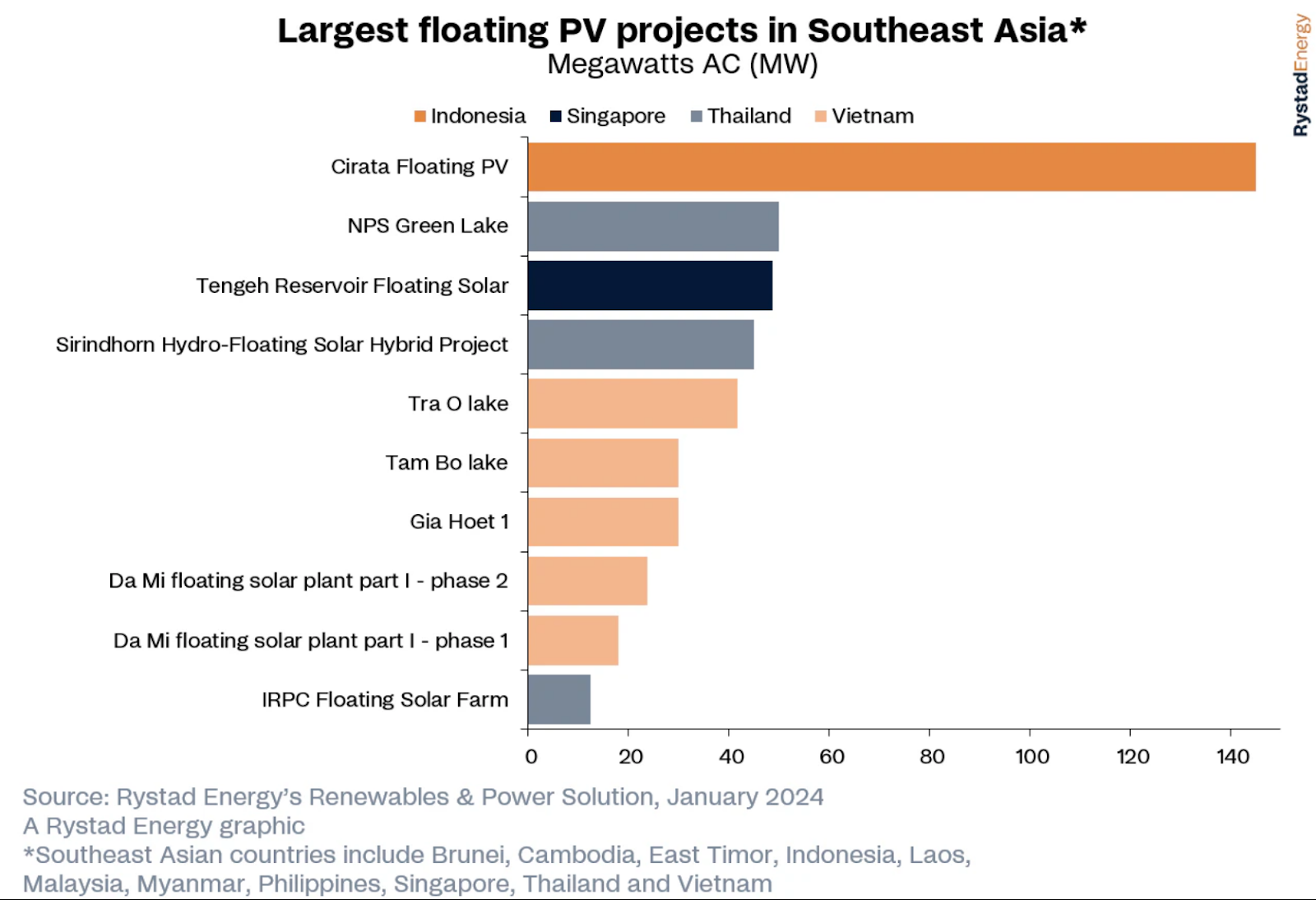

Wood Mackenzie projects that APAC will be home to nine of the top 10 global floating solar markets. Together, they will account for 57 of the 77 GW of installed floating solar capacity globally by 2033. India, China and Indonesia will be the three largest markets.

In 2024, China already opened the world’s largest open-sea floating solar project – a 1 GW power plant in the Shandong Province. However, growth is also expected in Southeast Asian countries.

Rystad Energy expects floating PV to play a key role in Southeast Asia’s solar expansion, accounting for 10% of the region’s total solar capacity by 2030. The experts identify the Philippines, Indonesia and Thailand as the countries leading this growing trend.

Vietnam has emerged as the world’s second-leading solar panel manufacturer after China and plans to continue advancing on that route through supportive policies and incentives. In 2024, the country issued policy guidelines for the rooftop solar market to stimulate self-produced and self-consumed solar energy in a bid to create favourable conditions and attract foreign investors to Vietnam’s renewable sector. According to the IEA, based on today’s deployment plans, Vietnam will remain Southeast Asia’s largest renewable power market by a wide margin. The country’s efforts to equip half of the office buildings and homes with rooftop solar panels will prove crucial for this development.

Like Vietnam, the Philippines has also initiated strategic policies and regulations to boost rooftop solar power deployment.

Malaysia’s government also plans to make the country a key player in the global green technology supply chain. It has already claimed a spot among the world’s leading solar PV manufacturers after China, Vietnam and Thailand.

3. EVs and Batteries

In October 2024, China’s share of the global electric car market rose spectacularly to 76%. After seeing its green vehicle sales jump 40% domestically while exports soared 20% in 2024, China will continue leading the global EV transition in 2025 as well. While exports are likely to slow down this year, IEA’s Global EV Outlook 2024 report sees the country responsible for over 50% of EV sales globally – a target China initially set for 2035. Other analysts expect China to have an even greater share in global electric vehicle sales this year.

Other Asian markets, such as Vietnam and Thailand, also promise to make strides in EV manufacturing. The former is already manufacturing EVs domestically, while in 2024, for example, China’s BYD, the world’s largest EV maker, opened its first EV factory in Southeast Asia in Thailand.

Regarding battery technology, China will continue to lead the world in the upcoming years. As per the IEA’s Announced Policies Scenario, its total committed battery manufacturing capacity will remain two times greater than its domestic demand by 2030, opening opportunities for exports. Aside from manufacturing, the country will advance global battery recycling capacity, 80% of which occurred in China in 2023. For reference, Europe and the United States are responsible for under 2% each. By 2030, global recycling capacity could exceed 1,500 GWh, of which 70% could be from China.

Vietnam plans to capitalise on the fact that it holds the world’s second-largest rare earth resources by increasing domestic production and becoming a key cog in the global critical minerals supply chain.

Together with Vietnam and Indonesia, Malaysia will be responsible for around 1% of the committed battery manufacturing capacity globally in 2030. In 2024, it announced plans to build the region’s largest battery energy storage system project.

Thailand is already home to Southeast Asia’s first lithium-ion battery gigafactory.

The Philippines is building the world’s largest solar and battery storage power plant. Currently, alongside Indonesia, it forms the world’s top nickel producers, accounting for about 65% of global mined production. Under the new leadership, Indonesia also aims to continue marching toward becoming a nickel mining centre for EV batteries.

4. Green Hydrogen

In the past two years, reputable analysis desks from BloombergNEF, Citibank and Deloitte have all issued reports calling the clean hydrogen market situation a “reality check”.

According to BNEF, while a supportive policy environment and a maturing project pipeline will make clean H2 supply skyrocket 30-fold to 16.4 million tonnes per year by 2030, it won’t meet most government targets. Furthermore, the experts expect just a third of the 1,600 projects announced to date to materialise and often later than planned. Of these, half would be green hydrogen.

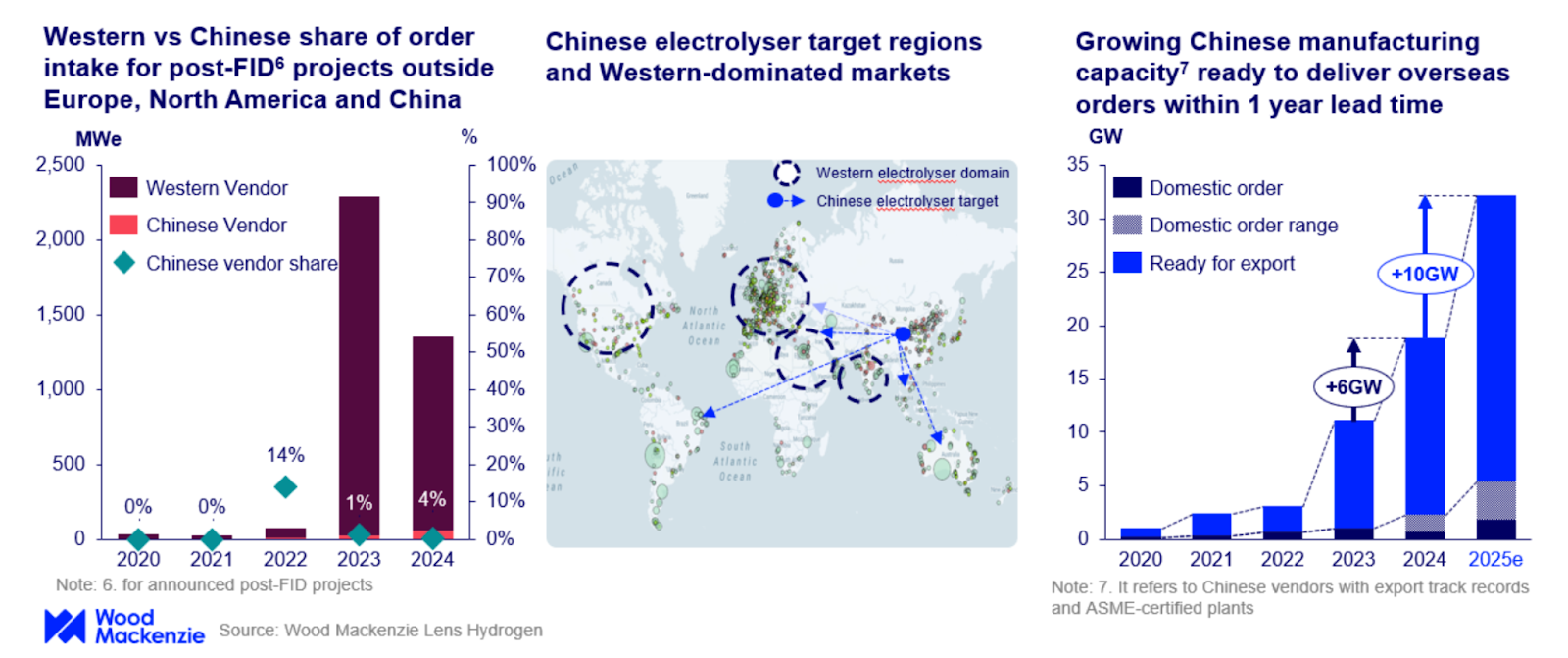

In a nutshell, there are just a handful of markets where the technology is proving economically feasible. According to a Wood Mackenzie analysis, in 2025, these would be regions that leverage cheap solar and wind power and benefit from government incentives that reduce costs and ensure financial viability. Cases in point are China and India. The experts note that the ability to ensure competitive pricing, shorter delivery times and strong manufacturing capacity will prove huge competitive advantages for Chinese electrolysers, which will capture a third of the global market outside the EU and North America. China plans to expand its domestic manufacturing capacity, including adding over 10 GW of capacity this year.

Yet, Wood Mackenzie’s analysis notes that the lack of transparency regarding offtake contracts across China makes assessing the full extent of uncontracted volumes in the country difficult. The uncertainty is also highlighted by BNEF.

Southeast Asia will also mark progress in green hydrogen, mainly due to benefitting from low-cost renewable energy and affordable electrolysers from Chinese manufacturers. According to Mordor Intelligence, Indonesia will emerge as the region’s leading green hydrogen production market in the years up to 2030.

S&P Global expects Japan and South Korea to be very active on the green hydrogen front, although it sees Asia’s pipeline experiencing major project cancellations and readjustments to original strategies in 2025. However, policy fragmentation and high production costs are expected to remain significant hurdles.

Asia To Continue Attracting Investors With Private Capital While Initiatives Play a Crucial Role

The IEA finds that investments in Asia’s clean electricity sector significantly outweigh those in fossil fuels, and the growth of coal power is declining. However, a more in-depth view reveals that Asia’s investment landscape is one of extremes. China has established itself as the undisputed global leader in clean energy investment growth between 2019 and 2024, while India ranks fourth after the US and the EU. Southeast Asia’s spending on clean energy makes up only about 2% of the global total.

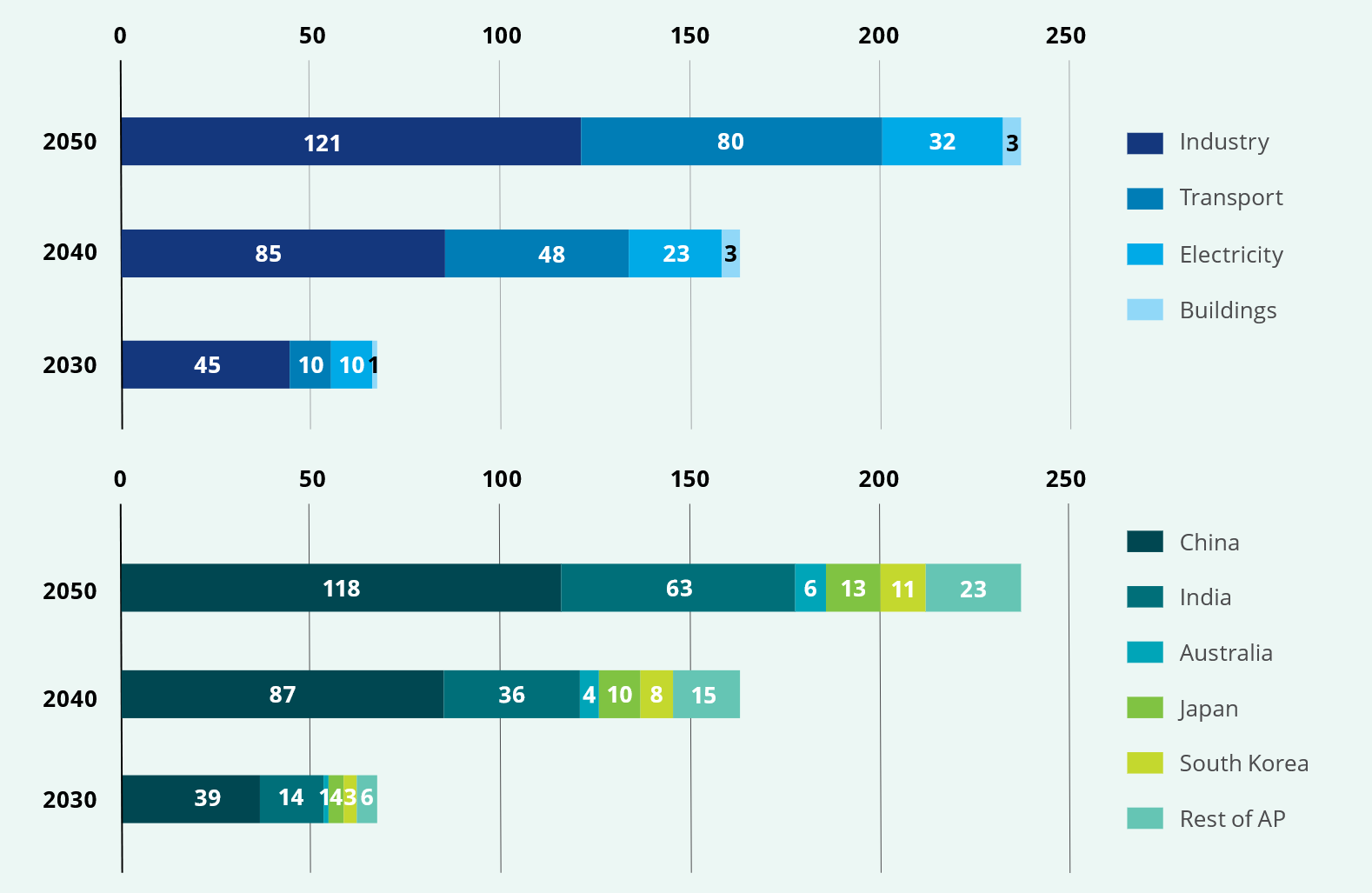

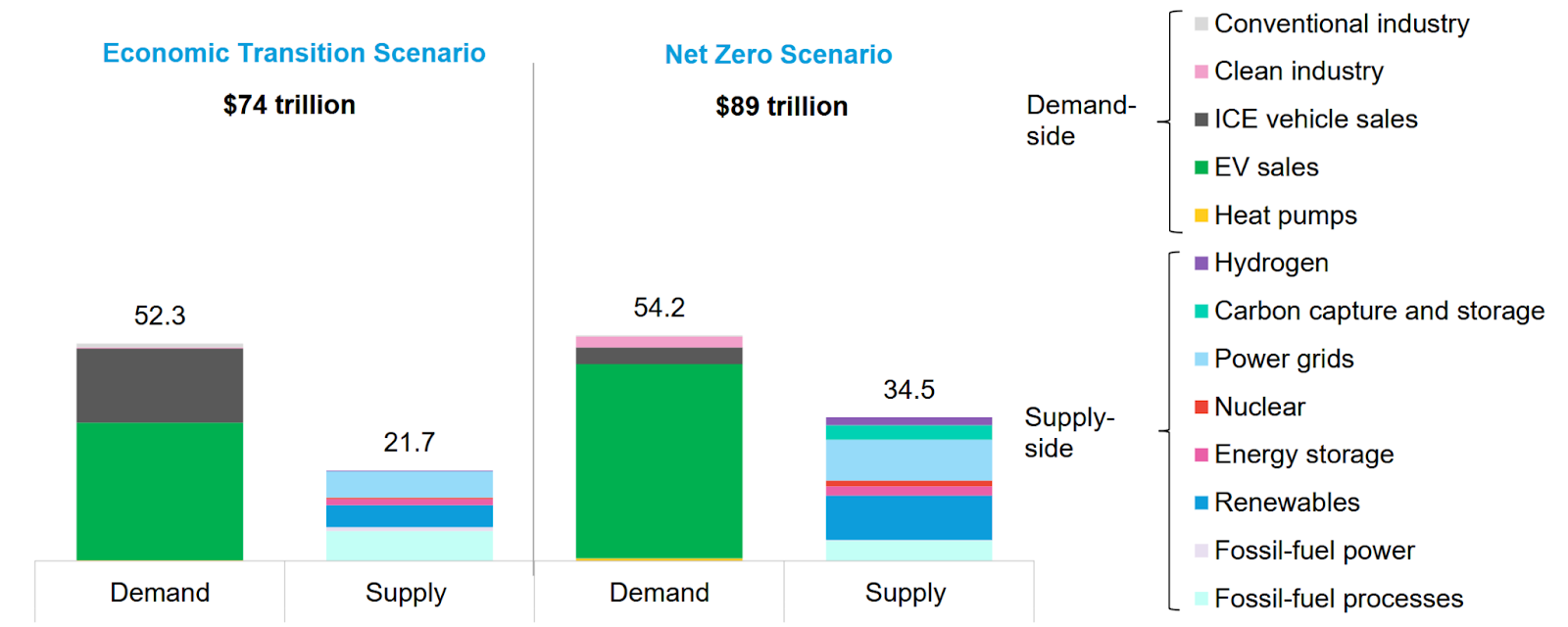

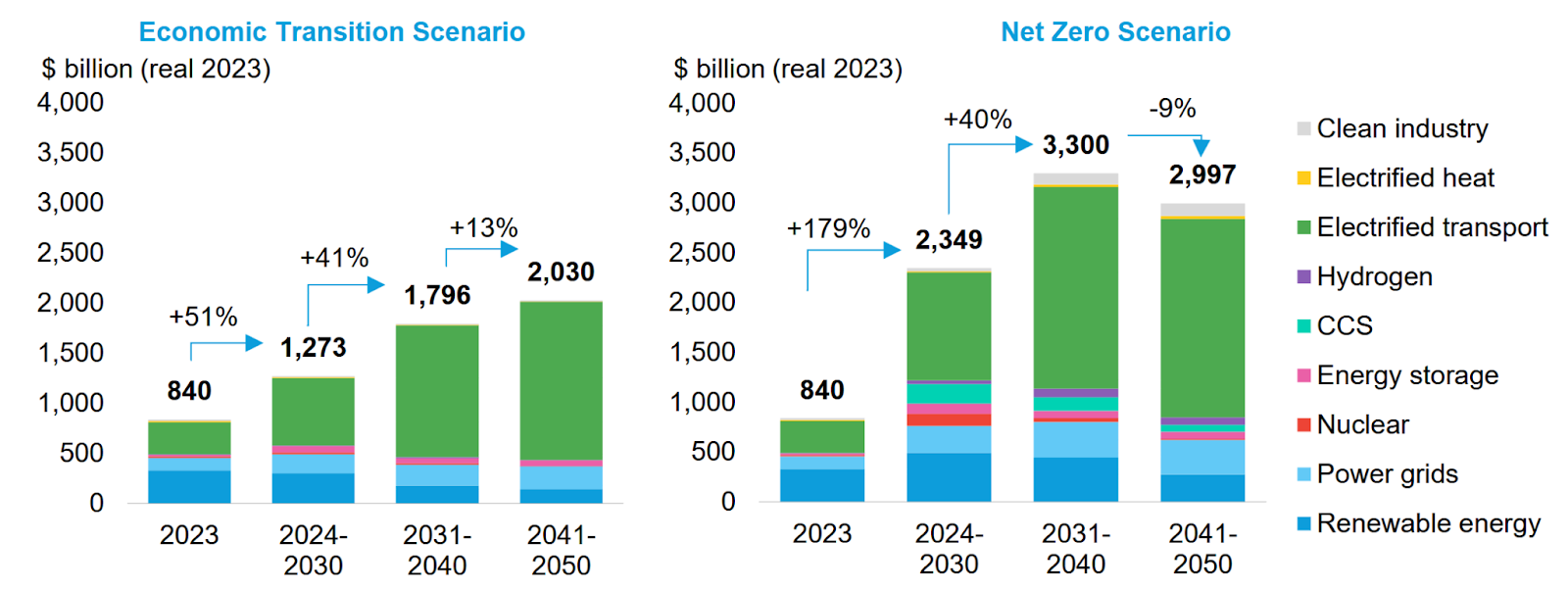

To stay on track with the Paris Agreement, BloombergNEF estimates that Asia-Pacific countries would need USD 88.7 trillion in investments. This is the total capital needed from all stakeholders, including companies, financial institutions, governments and consumers. Furthermore, the figures are just 20% higher compared to an Economic Transition Scenario (BNEF’s base case scenario), and the falling costs of low-carbon solutions, such as EVs and clean power, and new policy commitments will help close the spending gap between the two scenarios.

However, the experts estimate that clean energy investments in the region will have to increase significantly in the coming years. For example, the investments in the period between 2024 and 2030 should be triple the 2023 levels to align with the Paris Agreement’s goals.

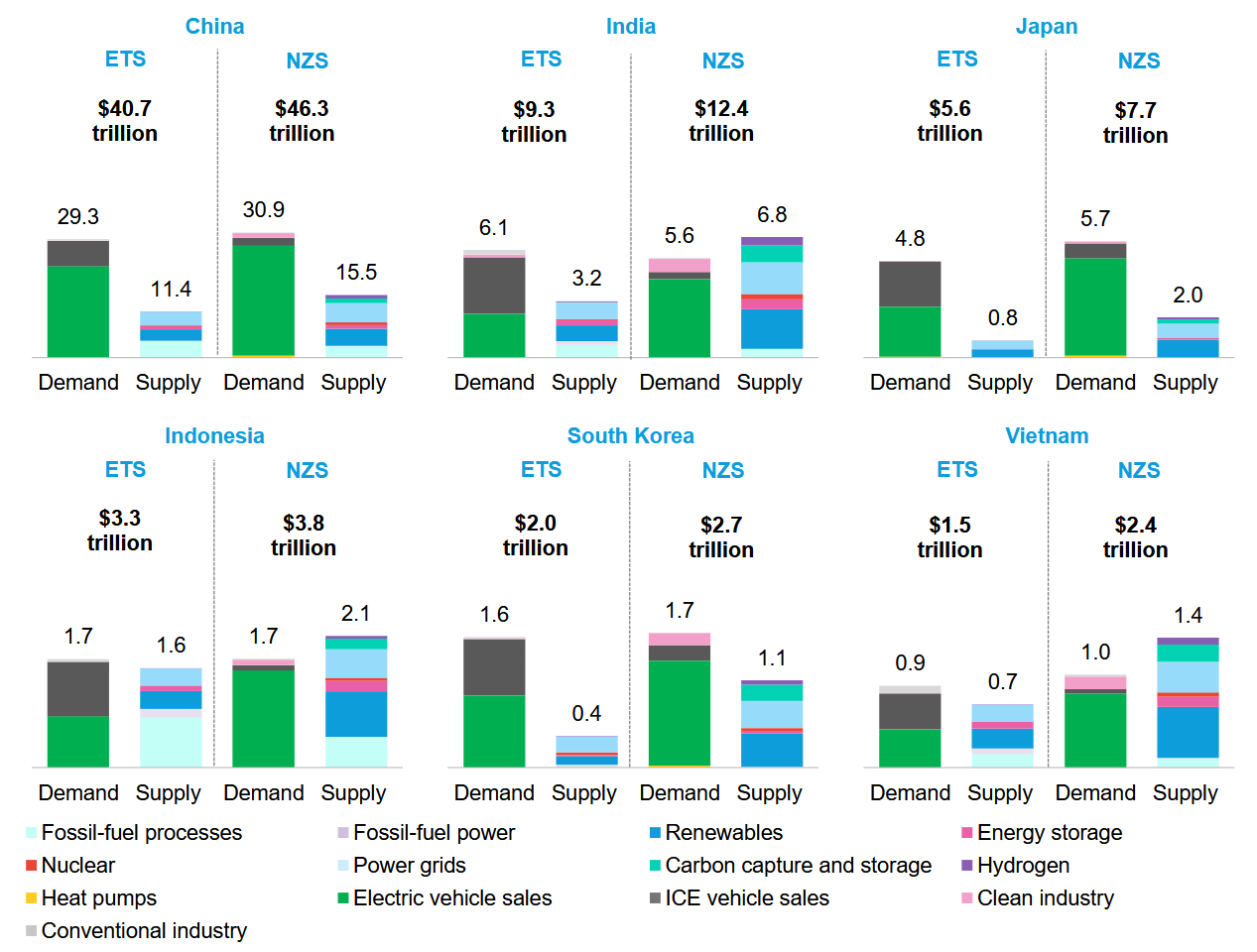

Regarding regional differences, China will represent 55% of the investments between 2024 and 2050, while in a net-zero-aligned scenario, India would represent an investment opportunity of USD 12.4 trillion.

However, investors are looking favourably toward Asia. According to KPMG, the recent progress on the regulatory front has helped create a more welcoming investment environment and established East Asia as the most preferred region for energy transition investors over the past two years. The consultancy finds that 2025 will be no different. While KPMG advises investors to move early into emerging markets to gain rewards, Asian governments must continue improving their regulatory frameworks to convince private capital holders that their markets are quickly maturing and capable of limiting investment risks. Governmental intervention and introduction of policies, such as feed-in tariffs, regulatory support, tax incentives, direct investments, subsidies and research and development grants are deemed most important for driving investments into energy transition technologies in APAC going forward.

by Viktor Tachev

Viktor has years of experience in financial markets and energy finance, working as a marketing consultant and content creator for leading institutions, NGOs, and tech startups. He is a regular contributor to knowledge hubs and magazines, tackling the latest trends in sustainability and green energy.

Read moreOur Publications