Renewable Energy Investing Needs in 2023

Faiz Zaki / Shutterstock.com

12 July 2023 – by Viktor Tachev

Emerging and developing nations face a key policy and financing challenge: finding the capital to address their renewable energy investment needs while dealing with more frequent climate change impacts. According to the International Energy Agency and the International Finance Corporation, the answer lies in attracting private institutions to invest in renewable energy projects. However, succeeding in this requires strong policy support, green capital market reforms and clear decarbonisation goals.

The Renewable Energy Investing Needs of Emerging and Developing Economies

Scaling Up Private Finance for Clean Energy in EMDEs, a joint report by the IEA and the IFC, estimates that emerging markets and developing economies’ (EMDEs) annual financing needs will reach up to USD 2.8 trillion by the early 2030s. The investments will need to triple from USD 770 billion in 2020 and remain at that level until 2050. The funds will help meet rising energy demand in a climate-friendly way. The main investment areas include clean electrification, energy efficiency and grid infrastructure and renewable energy generation.

The authors stress the importance of concessional financing for integral clean energy technologies that either haven’t reached scale yet or aren’t cost-competitive. Among them are batteries, offshore wind power, green desalination solutions, low-emission hydroelectric power and more. The concessional financing need will be between USD 80 billion and USD 100 billion per year by the early 2030s.

In the joint report, the IEA and the IFC also call for more focus on developing the green financing market in terms of the available instruments, harmonised taxonomies and certification practices.

Spotlight on the Green Energy Investing Needs of Asian Economies

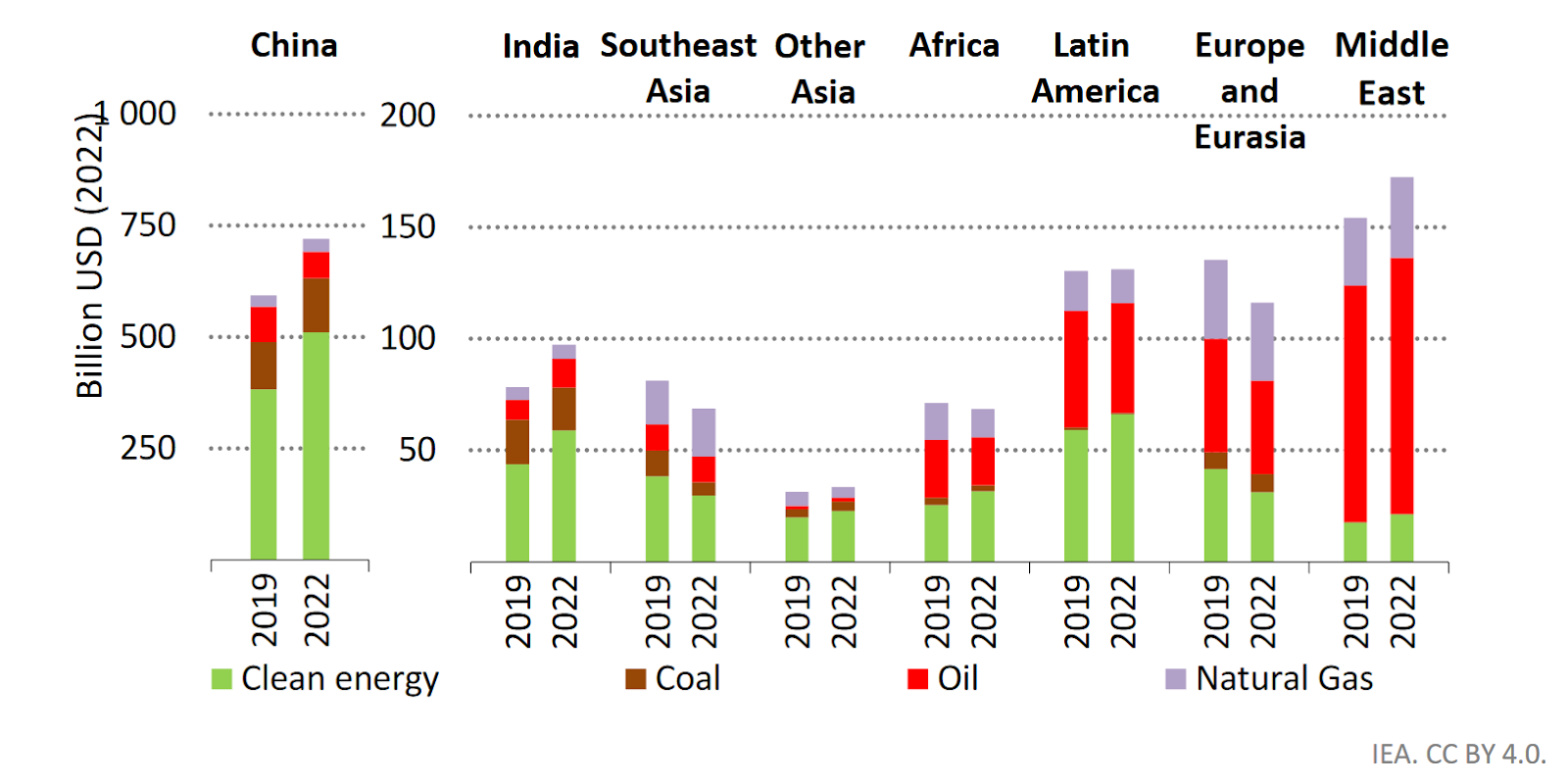

China accounts for two-thirds of the USD 770 billion in annual renewable investments. In 2022 alone, the country added 100 GW or 10 times Africa’s operating solar PV capacity. Alongside India and Brazil, it makes up over three-quarters of total annual investment in renewable energy today.

Going forward, the push for more sustainable investing initiatives will be especially strong in Southeast Asia. As of 2022, the region had the lowest average annual investment of just USD 30 billion. It must jump to USD 171-185 billion by 2026-30 and USD 208-244 billion by 2031-35.

India and other Asia also have massive renewable energy investment needs. For 2026-2030, the required capital is between USD 321-348 billion. By 2031-2035, it will be in the range of USD 418-467 billion. As of 2022, it sits at USD 82 billion.

Challenges and Opportunities From Scaling Up Renewable Energy Investments

The IFC’s Managing Director Makhtar Diop warns that the progress of EMDEs will determine the battle against climate change. The prerequisites to success are there, as most emerging and developing countries have massive clean energy potential. However, the main thing preventing them from capitalising on it is inadequate financing. To attract this, governments should concentrate on several key areas.

Getting the Private Sector Financiers Involved

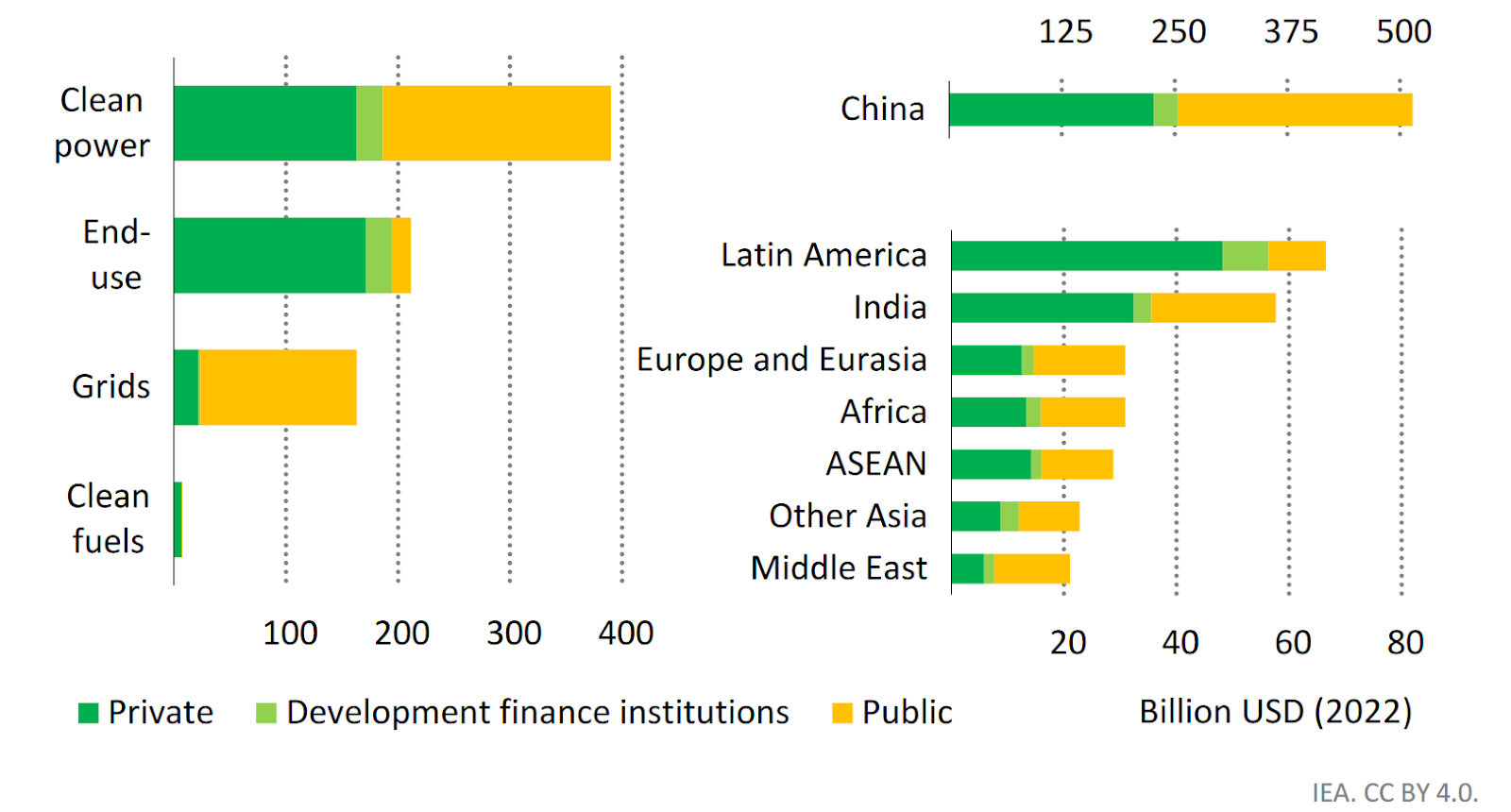

The IEA and IFC call for a blended finance approach. Their joint report notes that, in climate-driven scenarios, the private energy sector must finance about 60% of the clean energy bill in EMDEs since public funding would be insufficient.

While nowadays, the annual figure for renewable energy project financing in EMDEs outside China stands at USD 135 billion, it will need to rise to over USD 1.1 trillion within the next decade.

Attracting private capital should come from both international and domestic sources. While domestic sources are the leading providers in China and India, this isn’t the case for the rest of Asia. Furthermore, the report’s authors advise emerging and developing countries to improve the domestic bond, equity and derivatives markets to attract more local clean energy project investors.

Focus on Regulatory Changes

Governments should concentrate on acquiring greater global technical, regulatory and financial support to address their renewable energy investing needs.

On a domestic level, it is imperative to strengthen existing and design new regulatory frameworks that stimulate clean energy investing and incentivise private sector participation. This has been a widely spread practice across developed countries, and its effects are now evident. For example, in 2022, financing from public entities accounted for about half of EMDEs’ clean energy spending. For comparison, it was less than 20% in advanced economies.

It is worth noting that developing nations’ governments often have to allocate scarce resources across various priorities. Engaging private investors to help address their clean energy financing needs can ease the pressure on their budgets. Furthermore, it can free up funds towards other pressing needs, like climate change adaptation and mitigation.

Other policy reforms that can help attract private investors include removing fossil fuel subsidies, overcoming lengthy project licensing processes, making land use rights more transparent, easing restrictions on private or foreign ownership and designing flexible and favourable pricing policies.

According to the IEA, one of the main motivations for investment in EMDEs by private financiers is to ensure adequate risk-adjusted returns. Governments can lure them in by introducing competitive auctions and long-term power purchase agreements. Another essential measure is allowing companies to contract directly to clean power producers.

Furthermore, governments must address market-specific issues surrounding new clean energy capacity buildup, including the high cost of capital and relatively high upfront costs. The IEA notes that, currently, the cost of capital for a typical utility-scale solar power project can be up to three times higher in key emerging countries than in advanced economies or China.

Developing the Market For Green Capital

Developing industry guidelines, harmonised taxonomies, and robust third-party certification mechanisms can help ease issuing more green, social, and sustainability-linked bonds. According to the report, such a move can bridge the gap between the relatively small size of energy transition projects in EMDEs and the fairly sizeable minimum investment size that major institutional investors require.

Furthermore, it will open up the market and help mobilise private capital at scale by attracting institutional investors that don’t typically invest in individual projects.

However, issuances of green financing instruments remain low. In 2022, around USD 136 billion out of the USD 1.2-1.6 trillion of the total private finance needed came from green, social, sustainable and sustainability-linked (GSSS) bonds issued by EMDEs. Furthermore, China accounted for half of that. Green bonds can act as a bridge between investors and renewable energy assets.

Developing Clear Decarbonisation Goals and Roadmaps

The IEA and IFC say that clean energy investments won’t start flowing without credible energy transition commitments. Furthermore, they suggest that EMDEs should show investors that they are determined to foster the scaling up of clean energy and renewable sources adoption.

Furthermore, energy infrastructure and market fundamentals should be improved to provide a favourable environment for accelerated renewable energy market growth. Such a move will help turn commitments into bankable projects and attract global investment.

The report’s authors also stress the critical role of low-emission fuels like low-emission hydrogen, sustainable biofuels and CCUS in the energy transition. However, EMDEs need to be cautious since these solutions can often be misrepresented to extend fossil fuels’ life, like in the case of Japan’s GX technologies.

Backing the Energy Transitions of EMDEs Will Benefit Everyone

Many emerging and developing countries suffer from the same problems: energy and cost of living crises, high debt, food and energy insecurity and, most importantly, ever-worsening climate change impacts. Renewable energy investments can be a crucial factor for taming or avoiding these problems and can benefit both the capital providers and recipients.

According to the IEA’s Executive Director Fatih Birol, ensuring the needed financing will help EMDEs expand energy access, replace fossil fuels, improve energy security, create jobs, grow the renewable energy sector and ensure a sustainable future.

At the same time, developing Asia can offer private investors the opportunity to invest in the entire clean energy supply chain, including solar panels, wind turbines and battery manufacturing, since it already is or remains well-positioned to flourish. China is home to over 75% of the world’s battery and solar panel manufacturing processes, and the country also has a solid track record in critical mineral processing. With its recent policy developments, India is now another growing market for clean technology manufacturing. Meanwhile, Southeast Asian nations are leading markets for metals, rare minerals and other resources crucial to battery production.

However, not enough action is taking place. Governments need sound regulations, favourable policies and greatly expanded international support to change the situation. The IEA and the IFC promise to help governments scale up private-sector climate financing. The question is, who will take the opportunity?

by Viktor Tachev

Viktor has years of experience in financial markets and energy finance, working as a marketing consultant and content creator for leading institutions, NGOs, and tech startups. He is a regular contributor to knowledge hubs and magazines, tackling the latest trends in sustainability and green energy.

Read more