Hydrogen’s Role in the Asia Pacific’s Energy Transition

13 June 2024 – by Viktor Tachev

The Asia-Pacific region is home to five of the top 10 biggest emitters globally, cementing its crucial role in the global energy transition. While decarbonising hydrogen is becoming an ever-important topic for Asia, the IEA and various hydrogen market experts warn that its role should be complementary. Instead, Asia should focus on more efficient, ready-to-deploy and cheaper mitigation solutions, like solar and wind power.

The Hydrogen Plans of the Asia Pacific

Strong government policy support, private sector commitment and increased investments have accelerated Asia’s plans for hydrogen development in recent years.

China is the undisputed leader in hydrogen advancements in Asia and is a global producer. While most of the hydrogen still comes from fossil fuels, by 2050, the country expects around 70% of it to be green.

Under the Hydrogen Industry Development Plan (2021-2035), China aims to produce up to 200,000 tonnes per year by 2025. Local governments also support hydrogen development in the country, introducing favourable policies to encourage companies to invest in projects.

As of the end of 2023, China had around 1.2 GW of installed hydrogen capacity. This is close to half of the global total.

Japan is among the biggest proponents of hydrogen, as Energy Tracker Asia has previously reported. Through the Basic Hydrogen Strategy, the government plans to turn the country into the first hydrogen economy. It has already demonstrated leadership in several areas, such as marine transportation and hydrogen fuel cells, where it holds the most patents globally.

The country intends to boost the annual hydrogen supply to 3 million tonnes by 2030. By 2040 and 2050, this figure will jump to 12 and 20 million tonnes, respectively. The government has recently passed a law to provide 15-year subsidies for locally produced and imported hydrogen. However, the outlook is that the country will meet its demand mainly through deliveries. In total, Japan plans to spend USD 107 billion on hydrogen supply chains. Furthermore, it intends to assist in the development of ammonia co-firing and hydrogen across several developing Asian countries.

Other Asian Countries

India launched its National Green Hydrogen Mission, an investment program aiming to make the country the leading green hydrogen supplier. Among the targets is producing 5 million tonnes of renewable hydrogen by 2030. The country also plans to provide substantial financial incentives to encourage domestic electrolyser manufacturing and green hydrogen production.

Recognising low-carbon hydrogen as a key component of its future power mix, Singapore has devised a National Hydrogen Strategy. Under the framework, the country plans to invest in green hydrogen R&D and pursue global green hydrogen supply chains.

South Korea has also recognised green hydrogen as a cornerstone for its net-zero roadmap. The country is actively working to introduce policies aiming to ease the sector’s development. For example, under the 2019 Hydrogen Economy Roadmap, it aims for 93% clean hydrogen consumption by 2050. It also has ambitious targets to scale hydrogen use within the transportation sector.

Other Asian countries, like Indonesia, for example, have acknowledged the potential for hydrogen technologies, but are yet to actively tap into the market.

Experts Say Hydrogen Has Limited Role in the Energy Transition

“Hydrogen, as a whole, is not used as a fuel or energy carrier right now at all,” says Paul Martin, a chemical engineer, founder of Spitfire Research and co-founder of the Hydrogen Science Coalition.

Many hydrogen market experts share the opinion that green hydrogen, as a whole, remains a widely untested, expensive and inefficient technology. There aren’t strong signals that the situation will change. Bloomberg NEF’s Hydrogen Supply Outlook 2024 report projects the market’s future to remain uncertain.

According to the Hydrogen Science Coalition, which advocates a fact-based approach to hydrogen as an energy source to ensure that public investments in hydrogen are used responsibly and effectively, the world should prioritise renewable hydrogen to replace black and blue hydrogen first and then concentrate on its potential application across niche sectors without existing electrification solutions. The group also says that renewable hydrogen’s economic and efficiency challenges make its blending into existing gas grids unreasonable since it will only have a limited impact on emissions savings.

High Costs

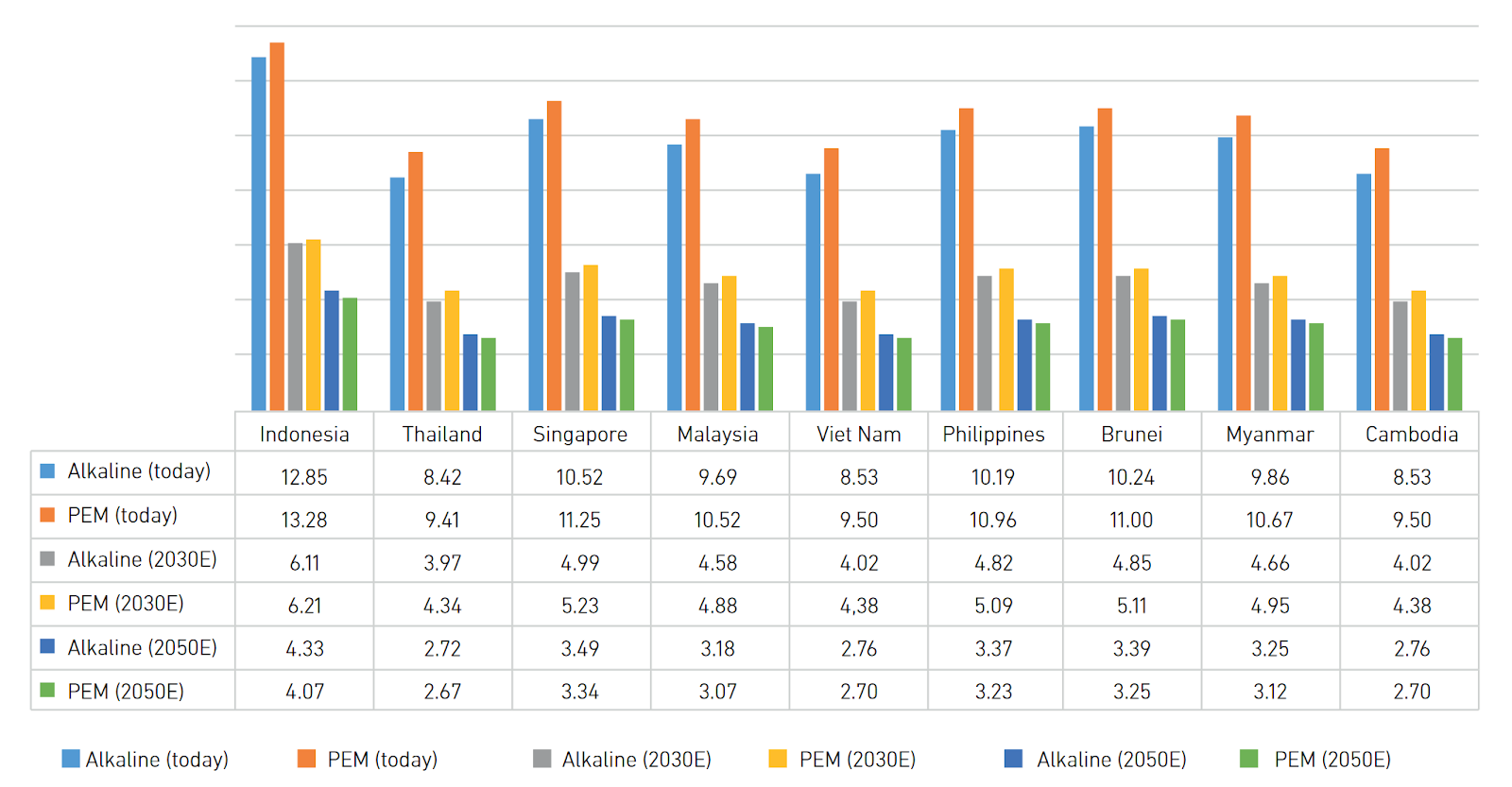

Green hydrogen remains expensive, so most countries invest in developing blue hydrogen, produced from natural gas with CCS. The costs of producing green hydrogen in the ASEAN region are as high as USD 8–13 per kg. The entire green hydrogen supply chain, including production, storage and transportation facilities, remains expensive due to its complexity. As a result, its development at the scale needed requires high capital investments.

“There is no green hydrogen to speak of right now. Why not? Because nobody can afford it,” says Martin. “The reality is that you can’t afford the electricity, or the capital, to make green hydrogen,” Martin added in a detailed analysis of the costs of green hydrogen.

The IEA warns that projects across the entire hydrogen value chain, which are highly capital intensive, are at risk of financial issues since equipment and financial costs are increasing. The agency notes that several projects have already revised their initial cost estimates upwards by up to 50%.

Factors like these are why Bloomberg NEF projects that, globally, less than a third of the announced clean hydrogen projects are likely to materialise. Those that do will often come online later than planned.

Furthermore, there are significant cost differences between markets. For example, BloombergNEF estimates the levelised cost for green hydrogen in Japan to be between two and three times higher than in China. However, if China decides to prioritise its hydrogen development, the gap could become even wider.

“Countries like Japan and South Korea, frankly, are in big trouble in a decarbonised future, especially if they make themselves dependent on importing energy in the form of hydrogen or hydrogen-derived molecules,” says Martin. He adds that “their economic competitors would be using energy which costs 1/10th as much per joule, and using that energy directly”.

BloombergNEF doesn’t expect favourable green hydrogen production policies to significantly change the situation. Due to economics, the demand in Asia will mostly be for blue hydrogen. However, according to the IEA, to achieve net zero by 2050, green hydrogen should hold a 77.8% share across the global hydrogen mix.

According to IRENA, green hydrogen costs in Southeast Asia can become competitive with fossil-based hydrogen before 2030, with the region producing up to 500 million tonnes at prices below 2 USD per kg. However, others aren’t as optimistic, referring to the lowest possible costs of USD 4 per kg by 2030 and USD 2.7 per kg by 2050. According to the Asian Development Bank Institute, even if production costs decrease, green hydrogen won’t be a viable option without a robust supply chain.

Lack of Commercial Availability and Production Challenges

Green hydrogen, for now, barely exists outside laboratories. Its real-world application is limited due to notable challenges to its commercialisation.

The IEA’s Global Hydrogen Review 2023 finds that clean hydrogen today accounts for less than 1% of global production and use. Furthermore, the agency notes that the demand remains concentrated in industry and refining. Less than 0.1% comes from new applications in heavy industry, transport or power generation. As a result, its suitability is yet to be tested en masse, leaving more question marks than answers. According to the IEA, clean hydrogen deployment needs to grow more than 100-fold by 2030 to align with its NZE Scenario.

However, this is easier said than done. Some analysis groups forecast that clean hydrogen technology might not be ready for application by 2035.

Bloomberg NEF estimates that globally, governments are likely to miss their aggregate clean hydrogen demand goals for 2030 by close to two-thirds. The main reasons include longer project completion times and insufficient policy support.

Furthermore, ensuring the proper infrastructure remains a challenge. Some market experts warn that while Asia has experience producing, transporting and storing grey hydrogen, it lacks the infrastructure and engineering capabilities to address the large scale needed to make green hydrogen a viable near-term solution. According to the IEA, hydrogen is mostly produced and consumed today in the same location. Scaling up transport and storage infrastructure for clean hydrogen is crucial for the fuel to play any role in the energy transition, but experts warn it won’t be easy.

“Only about 8% of world hydrogen production has moved any distance at all. Most hydrogen is consumed immediately without intermediate storage due to economic reasoning and basic thermodynamics,” explains Paul Martin. “Hydrogen is low in density and takes three times as much energy to move than natural gas, which takes about as much energy to move as electricity. It’s just too expensive to waste as fuel for heating or transport and is also difficult and expensive to move and store. As a result, major hydrogen users either build their own hydrogen plant or build their own facilities next door to a major hydrogen plant that already exists.” the expert adds.

Martin notes that while hydrogen is an appealing concept, its practical execution hides significant obstacles. The most notable are its production and application complexities since the process involves many steps, and energy loss is a part of every one of them during production, storage, transportation and use.

“The argument that we can use the natural gas infrastructure to move hydrogen is a sales pitch by the natural gas distribution industry – the people that own the pipes that carry gas and sell gas door to door,” explained Martin in an episode of Energy Tracker Asia’s Energy Insights podcast, dedicated to the role of hydrogen in the energy transition.

“If one looks at the job of replacing natural gas with hydrogen, first of all, not everywhere and every user all at once will be ready to use hydrogen. You will have to twin the pipeline network, and all the end-user devices will have to change, for example,” he continues.

“If this was all being funded by the industry, it would be a different matter, but it’s not. It’s being paid for out of the public purse,“ he explains further.

Inefficiency and Questionable Climate Credentials

“When you burn anything in the air, including hydrogen, there is a reaction between nitrogen and oxygen, and you make nitrogen oxides, which are toxic and have significant global warming potential. Nitrous oxide, for example, is an enormously powerful and persistent greenhouse gas with a global warming potential of 270 times that of CO2,” explains Martin.

The expert estimates that hydrogen production represents around 4% of world CO2 emissions. For comparison, aviation, one of the most carbon-intensive activities, contributes 2.5% to the world’s carbon emissions.

The IEA warns that in a net-zero scenario, low-emission hydrogen’s contribution to global CO2 emissions reduction efforts will be modest in comparison to critical mitigation efforts, like the deployment of renewables, direct electrification and behavioural change.

As a result, the agency envisions hydrogen’s primary role being in hard-to-abate sectors, like heavy industry, long-distance transport, shipping and aviation.

The majority of hydrogen development plans are currently related to fossil fuel produced hydrogen, which produces more emissions than conventional gas power generation. Yet, companies and governments are running away with the idea that hydrogen is a cleaner fuel and are actively channelling green capital in its development, including through transition bonds.

The UK government’s Department of Business, Energy and Industrial Strategy (BEIS) study concludes that hydrogen is twice “as powerful a greenhouse gas as previously thought”. It reacts with other greenhouse gases in the atmosphere and exacerbates their global warming potential (GWP). The study estimates the GWP for hydrogen to be between six and 16, compared to one for CO2. Furthermore, the study also finds an elevated risk of pipeline leaks during transportation.

Another Environmental Defense Fund report found that low-carbon hydrogen could be up to 50% worse for the climate than traditional fossil fuels.

Financing Green Hydrogen Aspirations Remains Challenging

The IEA estimates the global annual investment in low-emissions hydrogen and the respective transport and storage infrastructure required in an NZE scenario at USD 35 billion over the decade’s second half. This is around 40% of current annual spending on natural gas pipelines and shipping infrastructure. The agency estimates that an NZE by 2050 scenario requires 70% in yearly investment growth by 2030 to successfully meet the USD necessary 41 billion in financing for electrolyser installation by 2030. An analysis by the Energy Transitions Commission points out even higher figures of USD 80 billion in annual green hydrogen investment in the years up to 2050.

The scale of the needed green hydrogen investments presents a massive challenge. Yet, if the hydrogen transition is to succeed, it is imperative to make the fuel commercially available since few capital providers will invest in a technology with little to no commercial readiness, such as green hydrogen for energy production. Unless high production costs fall significantly, hydrogen won’t become an economically viable fuel, thus unable to lure project financiers. Other variables, including production efficiency improvements, the ability to rival the competitiveness of other clean energy sources such as solar and wind and demand risk, are also crucial to convince green capital providers that the future for green hydrogen is bright. Not all of these factors can be influenced by government policies, with some variables to be determined by market forces.

Increasing the commercial availability of clean hydrogen starts with de-risking project development. Succeeding in this mission requires joint collaboration between various stakeholders, including governments, which should ensure regulatory support and incentives, the private sector to drive development nurture demand, and accelerate innovation and, most importantly, public and private financiers and MDBs to provide adequate financing instruments.

The last point remains a significant barrier to accelerating the mass adoption of green hydrogen. According to a paper by the Asian Infrastructure Investment Bank, bringing prices down would require collaborative efforts in applying different financing mechanisms for the different types of projects and their stages of development, including venture capital, corporate finance, ordinary equity and project finance.

Hydrogen Risks Delaying the Energy Transition of Asia Pacific

“The focus on hydrogen looks more like an attempt to put off the energy transition until some future date when hydrogen becomes ‘economic’ as an option and burning fossil fuels or experimenting with inefficient projects like ammonia co-firing. If wind turbines were encircling the entirety of the Japanese islands, and they were thinking about hydrogen for just that extra bit that they couldn’t manage to do themselves, then I would give them the benefit of the doubt, but they’re not doing that. They’re talking about buying hydrogen from Australia, making it into ammonia and then shipping it to Japan and burning it in coal-fired power plants that are 30% efficient. It doesn’t make sense from an energy efficiency perspective, from a decarbonisation perspective, from an economic perspective. And yet, that’s what’s being proposed,” Paul Martin explains.

“Renewable electricity is more available, popular and cheaper than ever. But nothing about hydrogen has changed,” the expert adds.

Project complexity, regulatory and licensing barriers, high costs, slower innovation progress and uncertainty around mass commercial deployment make clean hydrogen a questionable solution for decarbonising Asia’s power sector. Achieving net zero in less than 30 years will not succeed if the primary focus is on conceptual ideas like hydrogen. All of the question marks prove too much to rectify the need for such a substantial focus on clean hydrogen, especially in light of the pace with which the climate crisis unfolds.

Paul Martin’s commentary for the article is made in a personal capacity and doesn’t necessarily reflect the views of the Hydrogen Science Coalition.

by Viktor Tachev

Viktor has years of experience in financial markets and energy finance, working as a marketing consultant and content creator for leading institutions, NGOs, and tech startups. He is a regular contributor to knowledge hubs and magazines, tackling the latest trends in sustainability and green energy.

Read moreOur Publications